PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833414

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833414

Personal 3D Printers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

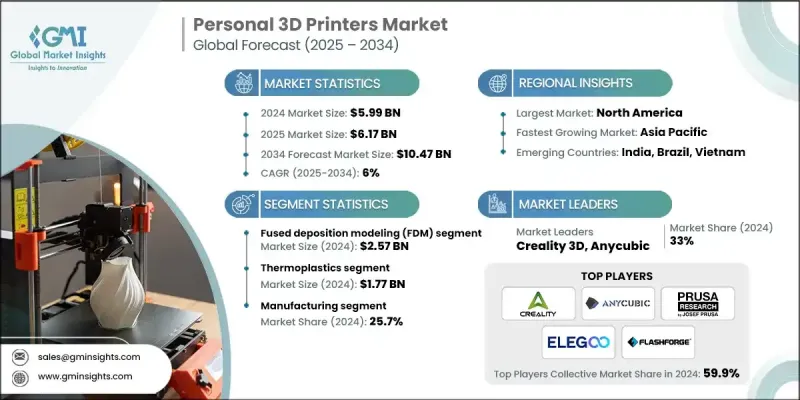

The Global Personal 3D Printers Market was valued at USD 5.99 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 10.47 billion by 2034.

The steady decline in pricing for desktop 3D printers has been one of the strongest growth drivers, as affordability has removed barriers for hobbyists, educators, and small-scale businesses. Continuous improvements in design and performance, including better resolution, multi-material printing, and intuitive interfaces, have further encouraged adoption. Affordable machines now deliver professional-quality output, making them attractive to individuals and institutions alike. Alongside this, the rise of maker culture and DIY communities has reinforced the adoption of single-user printers. Growing use in schools, community workshops, and small enterprises is spreading awareness, while online platforms and forums expand technical knowledge. These cultural changes emphasize creativity, innovation, and practical learning, creating an environment where personal 3D printers are seen as essential tools for experimentation, education, and independent product development. As accessibility improves, adoption continues to grow rapidly among students, hobbyists, and independent professionals seeking efficient, low-cost prototyping and customization solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.99 Billion |

| Forecast Value | $10.47 Billion |

| CAGR | 6% |

The fused deposition modeling (FDM) segment generated USD 2.57 billion in 2024, expanding at a CAGR of 7.1%. Its strength lies in its versatility, low material costs, and ease of access, making it a dominant choice for both consumer and education markets. Recent advances have introduced models with automated leveling, silent stepper drivers, and smart filament detection, enhancing user experience. To remain competitive, manufacturers are prioritizing modular systems, multi-material support, and simplified user interfaces that reduce setup complexity.

The thermoplastics material segment was valued at USD 1.77 billion in 2024 and is projected to grow at a CAGR of 5.3%. Their affordability, adaptability, and compatibility with FDM printers ensure they remain the preferred choice for prototyping and educational uses. Companies such as Creality and Prusa Research are broadening their filament lines with improved PLA, PETG, and ABS options, addressing user needs for durability, flexibility, and eco-friendliness. The focus is also shifting toward recyclable polymers and specialized blends for improved impact resistance or biocompatibility for applications like medical modeling.

U.S. Personal 3D Printers Market generated USD 1.61 billion in 2024. Market growth is supported by its established consumer electronics ecosystem and integration of 3D printing into both K-12 and higher education systems. Key manufacturers, including Creality (through distributors), Bambu Lab, and Prusa, dominate online and offline channels, supported by robust networks for filaments, spare parts, and repair services. A strong community of makers and educators fosters broader usage, while reliable supply chains make adoption smoother for end users.

Prominent companies in the Global Personal 3D Printers Industry include Bambu Lab, FlashForge, Creality 3D, Phrozen, Tronxy, Anycubic, Artillery 3D, QIDI Tech, Elegoo, Raise3D, Monoprice, MakerBot, Ultimaker (merged with MakerBot as UltiMaker), Prusa Research, Peopoly, Formlabs, Snapmaker, Wanhao, Dremel DigiLab, Tenlog 3D, LulzBot (by Aleph Objects), Anycubic Photon, XYZprinting, Sindoh, and Voxelab. Companies in the personal 3D printers market are focusing on strategies that enhance accessibility, user experience, and sustainability to secure a stronger competitive edge. Many are investing in modular, multi-material printers with intuitive user interfaces, making them suitable for beginners and experienced users alike. Expansion of filament portfolios is also a core strategy, with manufacturers offering eco-friendly, recyclable, and performance-driven materials to meet diverse application needs. Strong community engagement remains central, with firms building online knowledge bases, offering open-source designs, and cultivating maker networks. Partnerships with schools and universities are being strengthened to capture the education sector. Sustainability initiatives such as filament recycling and low-energy printers help companies build trust with eco-conscious users while enhancing brand value in a growing global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Printer technology trends

- 2.2.3 Material type trends

- 2.2.4 Price range trends

- 2.2.5 Distribution channel trends

- 2.2.6 End user trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Affordability of Desktop models

- 3.2.1.2 Expanding DIY & maker culture

- 3.2.1.3 Educational integration

- 3.2.1.4 User-friendly software & ecosystems

- 3.2.1.5 Growth of customization trends

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited material versatility

- 3.2.2.2 Maintenance & reliability issues

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Consumer sentiment analysis

- 3.13 Patent and IP analysis

- 3.14 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market estimates and forecast, by Printing Technology, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Fused Deposition Modeling (FDM)

- 5.3 Stereolithography (SLA)

- 5.4 Digital Light Processing (DLP)

- 5.5 Selective Laser Sintering (SLS)

- 5.6 Binder jetting

- 5.7 Inkjet printing / material jetting

- 5.8 Others

Chapter 6 Market estimates and forecast, by Material Type, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Thermoplastics

- 6.2.1 PLA

- 6.2.2 ABS

- 6.2.3 PETG

- 6.2.4 Nylon

- 6.2.5 Others

- 6.3 Photopolymers/resin

- 6.3.1 Standard resin

- 6.3.2 Tough resin

- 6.3.3 Flexible resin

- 6.3.4 Castable resin

- 6.4 Composites

- 6.4.1 Carbon-fiber infused

- 6.4.2 Wood-filled

- 6.4.3 Metal-filled

- 6.5 Others

Chapter 7 Market estimates and forecast, by Price Range, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Low-end (Below USD 300)

- 7.3 Mid-range (USD 300-1,000)

- 7.4 High-end (Above USD 1,000)

Chapter 8 Market estimates and forecast, by Distribution Channel, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Online retail

- 8.2.1 Brand-owned websites

- 8.2.2 E-commerce platforms

- 8.3 Offline retail

- 8.3.1 Technology & electronics stores

- 8.3.2 Educational suppliers & EdTech distributors

- 8.3.3 Authorized dealers

Chapter 9 Market estimates and forecast, by End Use, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 Education

- 9.3 Healthcare

- 9.4 Aerospace and Defense

- 9.5 Automotive

- 9.6 Consumer Goods

- 9.7 Manufacturing

- 9.8 Jewellery

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players:

- 11.1.1 Anycubic

- 11.1.2 Bambu Lab

- 11.1.3. Creality 3D

- 11.1.4 Elegoo

- 11.1.5 FlashForge

- 11.1.6 Formlabs

- 11.1.7 MakerBot

- 11.1.8 Prusa Research

- 11.1.9 QIDI Tech

- 11.1.10 Raise3D

- 11.1.11 Ultimaker

- 11.1.12 XYZprinting

- 11.2 Regional Players:

- 11.2.1 Dremel DigiLab

- 11.2.2 LulzBot

- 11.2.3 Monoprice

- 11.2.4 Sindoh

- 11.2.5 Snapmaker

- 11.2.6 Voxelab

- 11.2.7 Wanhao

- 11.3 Emerging Players:

- 11.3.1. Artillery 3D

- 11.3.2 Peopoly

- 11.3.3 Phrozen

- 11.3.4. Tenlog 3D

- 11.3.5 Tronxy