PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833422

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833422

Anti-Static Foam Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

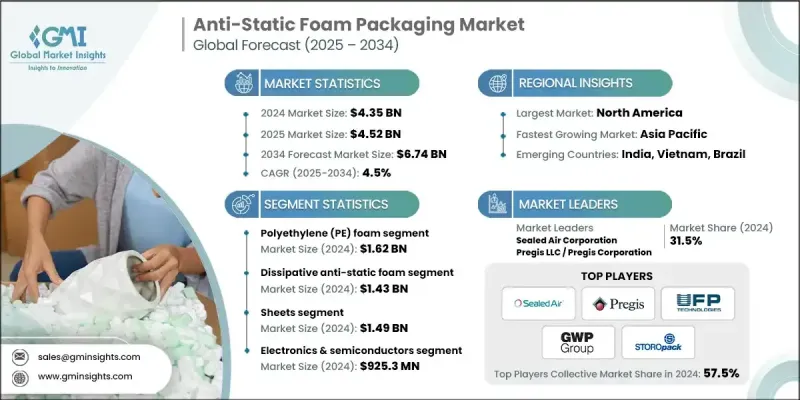

The Global Anti-Static Foam Packaging Market was valued at USD 4.35 billion in 2024 and is estimated to grow at a CAGR of 4.5% to reach USD 6.74 billion by 2034.

The growth of sensitive electronic devices such as semiconductors, circuit boards, and consumer electronics drives the need for anti-static foam packaging to prevent damage from electrostatic discharge during storage and transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.35 Billion |

| Forecast Value | $6.74 Billion |

| CAGR | 4.5% |

Rising Adoption of Polyethylene (PE) Foam

The polyethylene (PE) foam segment held a notable share in 2024, owing to its lightweight nature, cushioning ability, and excellent resistance to static discharge. Widely used for protecting delicate electronic components, PE foam provides flexibility in both design and application, making it suitable for custom inserts, trays, and wraps. With a growing demand for cost-effective protective materials, this segment continues to gain momentum among manufacturers and suppliers.

Increasing Demand for Sheets

The sheets segment generated a sustainable share in 2024, backed by its versatility and ease of customization. These sheets are ideal for cutting into inserts, dividers, and protective layers used in various industrial and consumer applications. The segment benefits from rising demand across warehousing, shipping, and assembly operations where component protection against static buildup is critical.

Electronics & Semiconductors to Gain Traction

The electronics and semiconductors segment will grow at a significant rate through 2034, driven by the need to prevent electrostatic discharge damage to highly sensitive devices like microchips, processors, and PCBs. As technology becomes more compact and performance-intensive, packaging precision and protection have become more critical than ever. Companies serving this segment are developing foam solutions with tighter static control specifications and integrating value-added services such as cleanroom packaging, kitting, and compliance testing to support quality assurance in semiconductor manufacturing and logistics.

North America to Emerge as a Propelling Region

North America anti-static foam packaging market held sustained growth in 2024, owing to its robust electronics manufacturing ecosystem and well-established logistics infrastructure. The region is home to several key players and serves as a hub for innovation in packaging technology. Regulatory focus on product safety, coupled with high-value exports of sensitive electronics, continues to fuel market growth.

Major players in the anti-static foam packaging market are Kaneka Corporation, Foam Fabricators, Inc., GWP Group Limited, Antistat, Pregis Corporation, UFP Technologies, Inc., Conductive Containers, Inc. (CCI), Flexipol Foams Pvt. Ltd., Storopack Hans Reichenecker GmbH, Recticel NV, DS Smith Plc, Dow Chemical Company, Sealed Air Corporation, Nefab AB, BASF SE, Polymer Packaging Inc., Tekni-Plex, Inc., Protective Packaging Corporation, Sonoco Products Company, and ACH Foam Technologies.

To strengthen their position in the anti-static foam packaging market, companies are adopting strategies centered around innovation, sustainability, and customer-centric service. Many are investing in eco-friendly materials and recyclable foams to meet growing environmental expectations. Others are enhancing product customization through precision cutting technologies and modular packaging systems. Strategic collaborations with electronics manufacturers and logistics providers help streamline supply chains and secure recurring contracts.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1. Material Type

- 2.2.2 Product Type

- 2.2.3 Form

- 2.2.4 End use Industry

- 2.2.5 North America

- 2.2.6 Europe

- 2.2.7 Asia Pacific

- 2.2.8 Latin America

- 2.2.9 Middle East & Africa

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspective: Strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical Success Factors

- 2.7 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Boom in electronics and semiconductor manufacturing

- 3.2.1.2 Rise in global e-commerce for electronics

- 3.2.1.3 Expansion of automotive electronics and ev adoption

- 3.2.1.4 Proliferation of miniaturized, ESD-sensitive components

- 3.2.1.5 Adoption in aerospace, defense, and medical device packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Production and Material Costs

- 3.2.2.2 Environmental Concerns and Recycling Limitations

- 3.2.3 Market Opportunities

- 3.2.3.1 Expansion of semiconductor fabs in emerging regions

- 3.2.3.2 Integration of AI and machine learning in lithography process control

- 3.2.3.3 Development of High-NA EUV technology

- 3.2.3.4 Growing demand for advanced packaging and 3D ICs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technological and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price Trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.13 Consumer sentiment analysis

- 3.14 Patent and IP analysis

- 3.15 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction Company market share analysis

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1. North America

- 4.2.2. Europe

- 4.2.3. Asia Pacific

- 4.2.2 Market concentration analysis

- 4.3 Competitive Benchmarking of key Players

- 4.3.1 Financial Performance Comparison

- 4.3.1.1. Revenue

- 4.3.1.2. Profit Margin

- 4.3.1.3. R&D

- 4.3.2 Product Portfolio Comparison

- 4.3.2.1. Product Range Breadth

- 4.3.2.2. Technology

- 4.3.2.3. Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1. Global Footprint Analysis

- 4.3.3.2. Service Network Coverage

- 4.3.3.3. Market Penetration by Region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1. Leaders

- 4.3.4.2. Challengers

- 4.3.4.3. Followers

- 4.3.4.4. Niche Players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial Performance Comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and Acquisitions

- 4.4.2 Partnerships and Collaborations

- 4.4.3 Technological Advancements

- 4.4.4 Expansion and Investment Strategies

- 4.4.5 Sustainability Initiatives

- 4.4.6 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates & Forecast, By Material Type, 2021 - 2034 (USD Million)

- 5.1 Polyethylene (PE) Foam

- 5.2 Polyurethane (PU) Foam

- 5.3 Polypropylene (PP) Foam

- 5.4 Other Materials (e.g., PVC, ESD corrugated foam)

Chapter 6 Market estimates & forecast, By Product Type, 2021 - 2034 (USD Million)

- 6.1 Conductive Anti-Static Foam

- 6.2 Dissipative Anti-Static Foam

- 6.3 Shielding Anti-Static Foam

- 6.4 Static-Neutral Foam

Chapter 7 Market estimates & forecast, By Form, 2021 - 2034 (USD Million)

- 7.1 Sheets

- 7.2 Rolls

- 7.3 Bags & Pouches

- 7.4 Inserts & Trays

- 7.5 Custom Shapes (Die-cut, Molded)

Chapter 8 Market estimates & forecast, By End use Industry, 2021-2034 (USD Million)

- 8.1 Electronics & Semiconductors

- 8.2 Automotive

- 8.3 Consumer Appliances

- 8.4 Aerospace & Defense

- 8.5 Healthcare & Medical Devices

- 8.6 Industrial Equipment

- 8.7 Others (e.g., telecom, renewable energy)

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 U.K.

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.3.7 ROE

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 RoAPAC

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 RoLATAM

- 9.6 Middle East & Africa

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

- 9.6.4 RoMEA

Chapter 10 Company Profile

- 10.1 Sealed Air Corporation

- 10.2 Pregis Corporation

- 10.3 Sonoco Products Company

- 10.4 Storopack Hans Reichenecker GmbH

- 10.5 Conductive Containers, Inc. (CCI)

- 10.6 Antistat

- 10.7 Nefab AB

- 10.8 Polymer Packaging Inc.

- 10.9 ACH Foam Technologies

- 10.10 Foam Fabricators, Inc.

- 10.11 BASF SE

- 10.12 Dow Chemical Company

- 10.13 Kaneka Corporation

- 10.14 Recticel NV

- 10.15 Tekni-Plex, Inc.

- 10.16 DS Smith Plc

- 10.17 UFP Technologies, Inc.

- 10.18 GWP Group Limited

- 10.19 Protective Packaging Corporation

- 10.20 Flexipol Foams Pvt. Ltd.