PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833428

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833428

U.S. Pet Therapeutic Diet Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

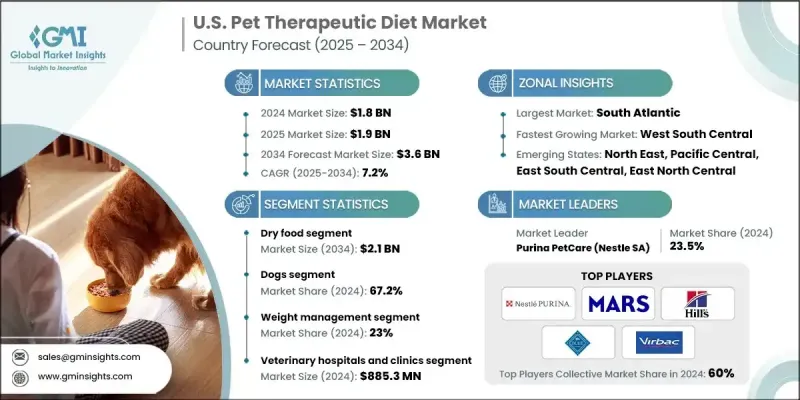

The U.S. Pet Therapeutic Diet Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 3.6 billion by 2034.

The growing prevalence of obesity and chronic conditions among pets in the U.S. is significantly influencing the demand for therapeutic diets. Just like humans, sedentary lifestyles, overfeeding, and poor-quality nutrition have led to an alarming rise in pet health issues such as diabetes, kidney disease, gastrointestinal disorders, and food allergies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 7.2% |

Rising Adoption of Dry Food

The dry food segment held a notable share in 2024, driven by its convenience, longer shelf life, and cost-effectiveness. Consumers find dry therapeutic food easier to store and measure, making it a preferred choice for daily feeding routines. Veterinary-recommended formulations for conditions like renal support, gastrointestinal health, and weight management are widely available in dry formats, allowing brands to reach a broader customer base.

Growing Prevalence of Dogs

The dogs segment in the U.S. pet therapeutic diet market generated a significant share in 2024, driven by their increasing popularity as companion animals. Dog owners are more likely to seek specialized nutrition plans for their pets, particularly chronic issues such as joint disorders, obesity, and skin allergies.

Weight Management to Gain Traction

The weight management segment held sizeable growth in 2024 as obesity among pets becomes a widespread concern. Rising calorie intake and reduced physical activity, especially among indoor pets, have triggered health risks that necessitate dietary intervention. Therapeutic diets focused on weight control offer low-fat, high-fiber formulations to support metabolic health without compromising on taste or nutrition.

South Atlantic to Emerge as a Propelling Region

South Atlantic pet therapeutic diet market will witness robust growth through 2034, driven by increasing pet ownership and rising awareness of chronic health conditions like obesity, diabetes, and allergies among pets in this region. The market benefits from a strong presence of veterinary clinics and specialty pet stores in urban hubs like Atlanta, Charlotte, and Miami. Pet owners here are more inclined to invest in premium, clinically formulated diets to manage their pets' health, reflecting broader national trends of humanization and preventive care.

Major players in the U.S. pet therapeutic diet market are Husse, Purina PetCare (Nestle SA), Drools Pet Food, Diamond Pet Foods (Schell & Kampeter, Inc.), Stella and Chewy's, Blue Buffalo Company (General Mills), Open Farm, Hill's Pet Nutrition (Colgate Palmolive), JustFoodForDogs, Mars, Incorporated, Virbac, EmerAid, Ziwi Pet.

To strengthen their position in the competitive U.S. pet therapeutic diet market, companies are leveraging a combination of innovation, education, and distribution enhancements. They are developing specialized formulas targeting specific health issues such as renal care, weight management, and digestive support, ensuring products meet diverse pet needs. Partnerships with veterinary professionals are critical, as companies provide training and educational materials to increase vets' recommendations of therapeutic diets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Zone trends

- 2.2.3 Product type trends

- 2.2.4 Animal type trends

- 2.2.5 Health condition trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased pet population and animal healthcare spending

- 3.2.1.2 Rising prevalence of chronic disease in pets

- 3.2.1.3 Strong veterinarian endorsement for therapeutic diet

- 3.2.1.4 Growing availability of products through e-commerce and subscription models

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory requirements

- 3.2.2.2 Increased competition from functional premium pet foods

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for natural and clean-label products

- 3.2.3.2 Expansion of microbiome-targeted formulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Technological advancements

- 3.6.1 Current technological platforms

- 3.6.2 Emerging technologies

- 3.7 Pricing analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dry food

- 5.3 Wet/canned food

- 5.4 Other product types

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Other animal types

Chapter 7 Market Estimates and Forecast, By Health Condition, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Renal health

- 7.3 Gastrointestinal health

- 7.4 Skin and coat health

- 7.5 Cardiovascular health

- 7.6 Weight management

- 7.7 Joint care

- 7.8 Other health conditions

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospitals and clinics

- 8.3 E-commerce

- 8.4 Retail pharmacies

- 8.5 Other distribution channels

Chapter 9 Market Estimates and Forecast, By Zone, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North East

- 9.2.1 Connecticut

- 9.2.2 Maine

- 9.2.3 Massachusetts

- 9.2.4 New Hampshire

- 9.2.5 Rhode Island

- 9.2.6 Vermont

- 9.2.7 New Jersey

- 9.2.8 New York

- 9.2.9 Pennsylvania

- 9.3 East North Central

- 9.3.1 Wisconsin

- 9.3.2 Michigan

- 9.3.3 Illinois

- 9.3.4 Indiana

- 9.3.5 Ohio

- 9.4 West North Central

- 9.4.1 North Dakota

- 9.4.2 South Dakota

- 9.4.3 Nebraska

- 9.4.4 Kansas

- 9.4.5 Minnesota

- 9.4.6 Iowa

- 9.4.7 Missouri

- 9.5 South Atlantic

- 9.5.1 Delaware

- 9.5.2 Maryland

- 9.5.3 District of Columbia

- 9.5.4 Virginia

- 9.5.5 West Virginia

- 9.5.6 North Carolina

- 9.5.7 South Carolina

- 9.5.8 Georgia

- 9.5.9 Florida

- 9.6 East South Central

- 9.6.1 Kentucky

- 9.6.2 Tennessee

- 9.6.3 Mississippi

- 9.6.4 Alabama

- 9.7 West South Central

- 9.7.1 Oklahoma

- 9.7.2 Texas

- 9.7.3 Arkansas

- 9.7.4 Louisiana

- 9.8 Mountain States

- 9.8.1 Idaho

- 9.8.2 Montana

- 9.8.3 Wyoming

- 9.8.4 Nevada

- 9.8.5 Utah

- 9.8.6 Colorado

- 9.8.7 Arizona

- 9.8.8 New Mexico

- 9.9 Pacific Central

- 9.9.1 California

- 9.9.2 Alaska

- 9.9.3 Hawaii

- 9.9.4 Oregon

- 9.9.5 Washington

Chapter 10 Company Profiles

- 10.1 Blue Buffalo Company (General Mills)

- 10.2 Diamond Pet Foods (Schell & Kampeter, Inc.)

- 10.3 Drools Pet Food

- 10.4 EmerAid

- 10.5 Hill's Pet Nutrition (Colgate Palmolive)

- 10.6 Husse

- 10.7 JustFoodForDogs

- 10.8 Mars, Incorporated

- 10.9 Open Farm

- 10.10 Purina PetCare (Nestle SA)

- 10.11 Stella and Chewy’s

- 10.12 Virbac

- 10.13 Ziwi Pet