PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833441

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833441

Non-Small Cell Lung Cancer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

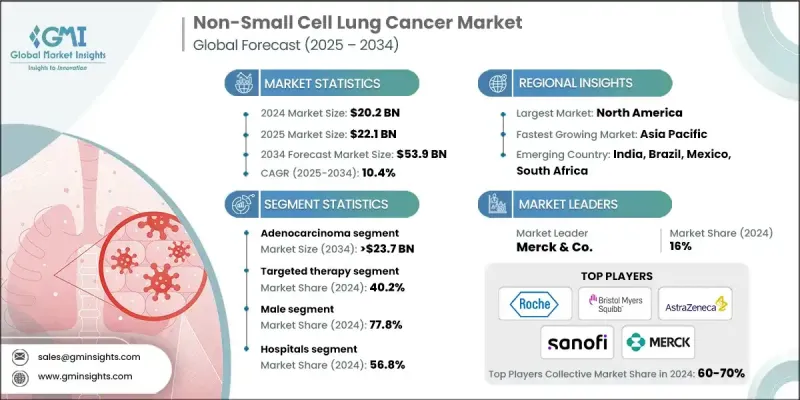

The Global Non-Small Cell Lung Cancer Market was valued at USD 20.2 billion in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 53.9 billion by 2034.

The development of therapies targeting specific genetic mutations (like EGFR, ALK, ROS1, and KRAS) has transformed treatment pathways, expanded personalized medicine and significantly improved outcomes in select patient groups.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.2 Billion |

| Forecast Value | $53.9 Billion |

| CAGR | 10.4% |

Rising Prevalence of Adenocarcinoma

The adenocarcinoma segment held a significant share in 2024, driven by its high prevalence, particularly among non-smokers and younger patients. As the most common histological subtype of NSCLC, adenocarcinoma is often associated with actionable genetic mutations, making it a prime focus for molecularly targeted therapies.

Increasing Adoption of Targeted Therapy

The targeted therapy segment held a sizeable share in 2024, backed by offering a personalized approach that improves survival while minimizing systemic toxicity. This segment has gained strong momentum due to the approval of multiple agents addressing specific oncogenic drivers like EGFR, ALK, BRAF, MET, and KRAS mutations. Targeted drugs are often preferred as first-line treatments for eligible patients, resulting in longer progression-free survival compared to traditional chemotherapy.

Male Sector to Gain Traction

The male segment generated a substantial share in 2024, owing to historically higher rates of smoking and occupational exposure to lung carcinogens among men. Although gender-based treatment protocols do not significantly differ, the higher incidence among male patients drives disproportionate demand in terms of diagnostics, therapy initiation, and follow-up care.

North America to Emerge as a Propelling Region

North America non-small cell lung cancer market will grow at a decent CAGR during 2025-2034, fueled by robust healthcare infrastructure, widespread biomarker testing, and early adoption of next-generation therapies. The region also benefits from active participation in global clinical trials and fast-track regulatory pathways that bring novel treatments to market faster. With rising investment in precision oncology and supportive government initiatives, North America is expected to maintain its dominant position in the NSCLC landscape.

Some prominent players operating in the non-small cell lung cancer industry include Xcovery, Merck & Co., Janssen Biotech, Sanofi, AbbVie, Novartis, Astellas Pharma, Pfizer, Eli Lilly, Takeda, F. Hoffmann La Roche, Bristol-Myers Squibb Company, AstraZeneca, Sun Pharmaceutical, and Merus.

To strengthen their presence in the non-small cell lung cancer market, companies are implementing a range of strategies, including expanding their precision oncology portfolios and accelerating time-to-market through regulatory fast-tracks. A major focus lies in developing next-generation inhibitors to overcome resistance to existing therapies, particularly in the targeted therapy segment. Collaborations with diagnostic firms are also key, as they enable streamlined patient identification through companion diagnostics.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Treatment

- 2.2.4 Gender

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of non-small cell lung cancer

- 3.2.1.2 Breakthroughs in immunotherapy and targeted treatments

- 3.2.1.3 Advancements in diagnostic technologies

- 3.2.1.4 Growing adoption of personalized medicine

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced therapies

- 3.2.2.2 Regulatory and diagnostic infrastructure gaps

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand in emerging markets

- 3.2.3.2 Shift toward personalized and combination therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Pipeline analysis

- 3.7 Technology and innovation landscape

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Adenocarcinoma

- 5.3 Squamous cell carcinoma

- 5.4 Large cell carcinoma

- 5.5 Other types

Chapter 6 Market Estimates and Forecast, By Treatment, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chemotherapy

- 6.3 Immunotherapy

- 6.4 Targeted therapy

- 6.5 Other treatment types

Chapter 7 Market Estimates and Forecast, By Gender, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Male

- 7.3 Female

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinics

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Astellas Pharma

- 10.3 AstraZeneca

- 10.4 Bristol-Myers Squibb Company

- 10.5 Eli Lilly

- 10.6 F. Hoffmann La Roche

- 10.7 Janssen Biotech

- 10.8 Merck & Co.

- 10.9 Merus

- 10.10 Novartis

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Sun Pharmaceutical

- 10.14 Takeda

- 10.15 Xcovery