PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833661

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833661

Sleep Tech Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

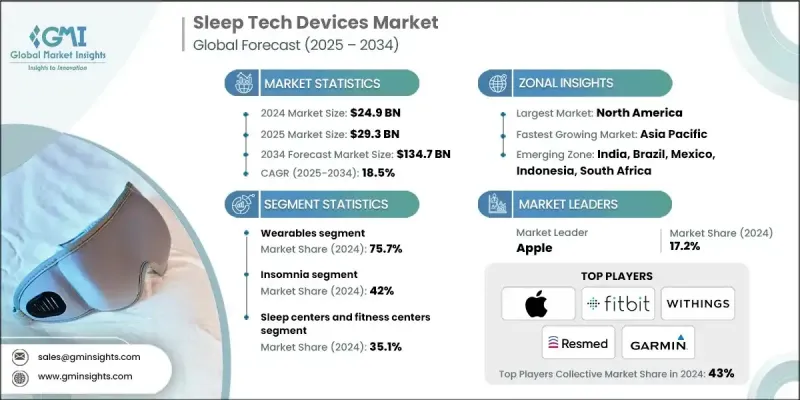

The global sleep tech devices market was estimated at USD 24.9 billion in 2024 and is expected to grow from USD 29.3 billion in 2025 to USD 134.7 billion in 2034, at a CAGR of 18.5%, according to the latest report published by Global Market Insights Inc.

According to various health studies, a significant portion of the adult population now experiences poor sleep quality or insufficient sleep duration, often without being formally diagnosed. This underdiagnosis further drives demand for consumer-facing, non-invasive devices that allow individuals to self-monitor and take early action.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $24.9 Billion |

| Forecast Value | $134.7 Billion |

| CAGR | 18.5% |

Increasing Adoption of Wearables

The wearables segment held a notable share in 2024. Consumers are increasingly turning to smartwatches, fitness bands, and other sensor-equipped wearables to monitor sleep patterns, heart rate variability, and oxygen saturation throughout the night. The demand is largely driven by the desire for continuous, non-invasive health tracking that fits seamlessly into daily life. With improvements in sensor accuracy and AI-powered analytics, wearables are evolving from basic sleep trackers to holistic wellness companions.

Increasing Prevalence of Insomnia

The insomnia segment will grow at a decent CAGR through 2034, as millions of individuals struggle with chronic sleep initiation and maintenance problems. Sleep tech devices tailored for this market-such as smart pillows, cognitive behavioral therapy (CBT)-based apps, and noise-masking devices-are gaining traction among both consumers and clinicians. The focus is on providing drug-free, personalized solutions that enhance sleep quality without adverse side effects. Key players are investing in evidence-based features and digital therapeutics to address the root causes of insomnia while delivering actionable insights that promote better sleep hygiene and long-term behavioral changes.

Sleep Centers and Fitness Centers to Gain Traction

The sleep centers and fitness centers held a sizeable share in 2024. Sleep labs are increasingly adopting advanced monitoring systems, AI-powered diagnostics, and connected devices to streamline sleep studies and improve clinical outcomes. At the same time, fitness centers are integrating sleep tracking services as part of broader wellness programs, recognizing the direct link between sleep quality, physical performance, and recovery. These partnerships are opening new B2B revenue streams for manufacturers and creating a hybrid ecosystem where medical and lifestyle applications of sleep technology can coexist and thrive.

North America to Emerge as a Propelling Region

North America sleep tech devices market is expected to generate significant revenues by 2034, fueled by high consumer awareness, advanced healthcare infrastructure, and strong demand for personalized wellness solutions. The United States, in particular, accounts for the lion's share of the region's revenue, with rising rates of sleep disorders and chronic health conditions creating ongoing demand for both consumer-grade and clinical-grade devices. The market in North America is expected to continue growing steadily, supported by favorable reimbursement policies for medical devices, innovation in wearable technologies, and the expansion of digital health platforms.

Major players in the sleep tech devices market are Smart Nora, Fitbit, BedJet, Withings, ResMed, Emfit, Oura Health, SleepScore Labs, Somnofy, Balluga, ChiliSleep, Apple, ReST, Itamar Medical, Huawei, Somnox, Pulsetto, Philips, Garmin, Eight Sleep, Xiaomi, Fisher & Paykel Healthcare.

To strengthen their foothold in the sleep tech devices market, leading companies are employing a mix of strategic partnerships, product innovation, and targeted acquisitions. Many are focusing on integrating AI and machine learning to deliver deeper insights and predictive analytics, enhancing user engagement and clinical relevance. Others are expanding their ecosystems through interoperability with health apps and smart home platforms. Brand differentiation is also being achieved through direct-to-consumer models, influencer marketing, and subscription-based service models. Additionally, collaborations with healthcare providers and sleep clinics help companies validate their offerings while tapping into new patient segments and reimbursement channels.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements in sleep tech devices

- 3.2.1.2 Increasing awareness regarding availability of sleep tech devices

- 3.2.1.3 Rising geriatric population

- 3.2.1.4 Surging demand for portable, efficient and superior sleep tech devices

- 3.2.1.5 Product innovation and adoption of different strategies by key market participants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of sleep tech devices

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with telehealth and remote patient monitoring

- 3.2.3.2 Expansion into mental health and wellness segments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Consumer behaviour trend

- 3.8 Go-to-market strategy analysis

- 3.9 Porter's analysis

- 3.10 Brand analysis

- 3.11 Business model of top companies

- 3.11.1 Apple

- 3.11.2 ResMed

- 3.12 PESTEL analysis

- 3.13 Future market trends

- 3.14 Gap analysis

- 3.15 Pricing analysis, 2024

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Wearables

- 5.2.1 Smart watches and bands

- 5.2.2 Other wearables

- 5.3 Non-wearables

- 5.3.1 Sleep monitors

- 5.3.2 Smart beds

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Obstructive sleep apnea

- 6.3 Insomnia

- 6.4 Narcolepsy

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Sleep centers and fitness centers

- 7.3 Hypermarkets and supermarkets

- 7.4 E-commerce

- 7.5 Pharmacy and retail stores

- 7.6 Other distribution channels

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Apple

- 9.2 Balluga

- 9.3 BedJet

- 9.4 ChiliSleep

- 9.5 Eight Sleep

- 9.6 Emfit

- 9.7 Fisher & Paykel Healthcare

- 9.8 Fitbit

- 9.9 Garmin

- 9.10 Huawei

- 9.11 Itamar Medical

- 9.12 Oura Health

- 9.13 Philips

- 9.14 Pulsetto

- 9.15 ResMed

- 9.16 ReST

- 9.17 SleepScore Labs

- 9.18 Smart Nora

- 9.19 Somnofy

- 9.20 Somnox

- 9.21 Withings

- 9.22 Xiaomi