PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1844302

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1844302

Cognitive Agent Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

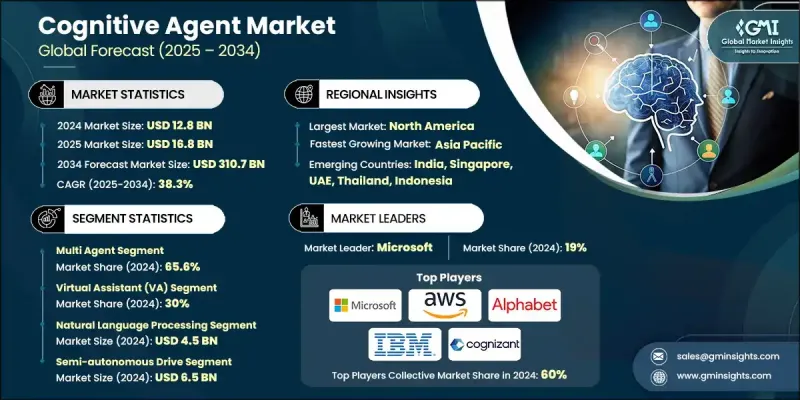

The Global Cognitive Agent Market was valued at USD 12.8 billion in 2024 and is estimated to grow at a CAGR of 38.3% to reach USD 310.7 billion by 2034.

The demand for cognitive agents is being driven by organizations looking to enhance decision-making, automate customer interactions, and increase operational efficiency. These advanced systems move beyond traditional virtual assistants, leveraging cutting-edge technologies to understand context, learn from past experiences, and perform tasks either independently or with minimal human input. Industries such as BFSI, healthcare, retail, manufacturing, government, and education are adopting cognitive agents to support functions like customer service, fraud detection, supply chain optimization, and workforce management. The global pandemic accelerated the adoption of AI solutions, including cognitive agents, as companies and governments adjusted to remote work and customer service demands. During 2019-2020, AI-related investments saw a significant 40% increase, signaling a shift towards AI-driven solutions to sustain operations and service customers amid disruptions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.8 Billion |

| Forecast Value | $310.7 Billion |

| CAGR | 38.3% |

The multi-agent segment held a 65.6% share in 2024 and is projected to grow at a CAGR of 37.1% from 2025 to 2034. This segment thrives due to its ability to coordinate with multiple AI systems to solve tasks in a collaborative manner. Multi-agent systems can interact, share data, and enhance decision-making to optimize performance, making them ideal for managing large-scale, dynamic operations in industries like technology, finance, and logistics.

The virtual assistant segment held a 30% share in 2024 and is expected to grow rapidly, at a CAGR of 35.5% from 2025 to 2034. These assistants are becoming increasingly popular for improving customer interactions and providing seamless user experiences, offering scalability that can handle millions of users while integrating into broader digital ecosystems.

U.S. Cognitive Agent Market generated USD 4.4 billion in 2024. With its advanced technological infrastructure and substantial enterprise adoption, the U.S. continues to dominate the global cognitive agent market. Government support, like the National AI Initiative, fosters the development of AI technologies, encouraging both established tech companies and startups to invest in cognitive agent solutions across various industries.

Major players in the Global Cognitive Agent Market include IBM, Microsoft, OpenAI, Salesforce, Cognizant, Oracle, NVIDIA, Google, Accenture, and Amazon Web Services. Companies in the cognitive agent market are adopting a variety of strategies to expand their market presence. These include strategic partnerships, mergers, and acquisitions to enhance technology offerings and improve market reach. Some companies are also heavily investing in R&D to improve the functionality of their cognitive agents, enabling them to offer more sophisticated decision-making, automated customer service, and process optimization capabilities. Additionally, companies are focusing on the integration of cognitive agents into existing business workflows to provide added value for customers across industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.6.1.1 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Agent

- 2.2.3 System

- 2.2.4 Autonomy Level

- 2.2.5 Technology

- 2.2.6 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Cloud service providers

- 3.1.1.2 AI platform providers

- 3.1.1.3 System integrators

- 3.1.1.4 Hardware & infrastructure providers

- 3.1.1.5 Security & governance solution providers

- 3.1.1.6 Industry-specific AI solution providers

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing enterprise adoption of AI-powered virtual assistants

- 3.2.1.2 Rising investments in generative AI, machine learning, and NLP technologies

- 3.2.1.3 Growing demand for automation across industries

- 3.2.1.4 Expansion of cloud infrastructure and AI-as-a-Service offerings

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Data privacy, cybersecurity, and regulatory concerns

- 3.2.2.2 High integration complexity with legacy IT systems

- 3.2.3 Market opportunities

- 3.2.3.1 Collaboration between AI tech providers and industry-specific players

- 3.2.3.2 Development of multi-agent systems and fully autonomous cognitive agents

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Large language model evolution

- 3.3.1.2 Multi-modal AI integration

- 3.3.1.3 Reinforcement learning advances

- 3.3.1.4 Neural architecture search

- 3.3.2 Emerging technologies

- 3.3.2.1 Federated learning for agents

- 3.3.2.2 Edge AI & distributed computing

- 3.3.2.3 Quantum computing integration

- 3.3.2.4 Brain-computer interface development

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 NIST AI risk management framework

- 3.5.2 EU AI compliance requirements

- 3.5.3 GDPR data protection impact

- 3.5.4 Sector-specific AI regulations

- 3.5.5 International AI governance standards

- 3.5.6 Ethical AI development guidelines

- 3.6 Cost breakdown analysis

- 3.6.1 Development & training costs

- 3.6.2 Infrastructure & computing expenses

- 3.6.3 Integration & customization costs

- 3.6.4 Ongoing maintenance & updates

- 3.6.5 Compliance & governance costs

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Environmental impact assessment & lifecycle analysis

- 3.10.2 Social impact & community relations

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable technological development

- 3.11 Use cases

- 3.12 AI model & algorithm analysis

- 3.12.1 Foundation model landscape

- 3.12.2 Fine-tuning & customization approaches

- 3.12.3 Model performance benchmarking

- 3.12.4 Training data requirements

- 3.12.5 Computer resource optimization

- 3.13 Investment landscape analysis

- 3.13.1 Venture capital investment in cognitive AI

- 3.13.2 Corporate investment & acquisition activity

- 3.13.3 Government AI research funding

- 3.13.4 Academic research investment

- 3.14 Customer behavior analysis

- 3.14.1 Enterprise adoption decision factors

- 3.14.2 Use case prioritization patterns

- 3.14.3 Vendor evaluation criteria

- 3.14.4 Implementation approach preferences

- 3.15 Performance & quality standards

- 3.15.1 Agent response accuracy metrics

- 3.15.2 Processing speed & latency requirements

- 3.15.3 Scalability & throughput benchmarks

- 3.15.4 Reliability & availability standards

- 3.16 Risk assessment framework

- 3.16.1 AI model bias & fairness risks

- 3.16.2 Data privacy & security risks

- 3.16.3 Regulatory compliance risks

- 3.16.4 Technology obsolescence risks

- 3.17 Ethical AI & responsible development

- 3.17.1 AI ethics framework implementation

- 3.17.2 Bias detection & mitigation strategies

- 3.17.3 Fairness & inclusive considerations

- 3.17.4 Transparency & explainability requirements

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Agent, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Virtual Assistants (VA)

- 5.3 Conversational Customer Agents

- 5.4 Digital Workers

- 5.5 Decision-Support

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By System, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Single agent

- 6.3 Multi agent

Chapter 7 Market Estimates & Forecast, By Autonomy Level, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Semi-autonomous

- 7.3 Fully autonomous

- 7.4 Assistive (Human-in-the-loop)

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Machine Learning (ML)

- 8.3 Natural Language Processing

- 8.4 Computer Vision

- 8.5 Robotics Process Automation (RPA)

- 8.6 Cognitive Computing

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Banking, Financial Services & Insurance (BFSI)

- 9.3 Healthcare & Life Sciences

- 9.4 Retail & e-commerce

- 9.5 Media & Entertainment

- 9.6 Manufacturing

- 9.7 Government & Public Sector

- 9.8 Education

- 9.9 Transportation & Logistics

- 9.10 Energy & Utilities

- 9.11 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 OpenAI

- 11.1.2 Microsoft

- 11.1.3 Google

- 11.1.4 Amazon Web Services

- 11.1.5 IBM

- 11.1.6 Anthropic

- 11.1.7 Salesforce

- 11.1.8 Meta Platforms

- 11.1.9 NVIDIA

- 11.1.10 Oracle

- 11.2 Regional players

- 11.2.1 UiPath

- 11.2.2 Automation Anywhere

- 11.2.3 ServiceNow

- 11.2.4 Baidu

- 11.2.5 Alibaba Cloud

- 11.2.6 Tencent

- 11.2.7 SAP

- 11.2.8 Palantir Technologies

- 11.2.9 DataRobot

- 11.2.10 H2O.ai

- 11.3 Emerging players

- 11.3.1 Cohere

- 11.3.2 Stability AI

- 11.3.3 Hugging Face

- 11.3.4 Adept AI

- 11.3.5 Character.AI

- 11.3.6 Jasper AI

- 11.3.7 Copy.ai

- 11.3.8 Rasa

- 11.3.9 Moveworks

- 11.3.10 Avanade