PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1844313

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1844313

U.S. Veterinary Orthopedic Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

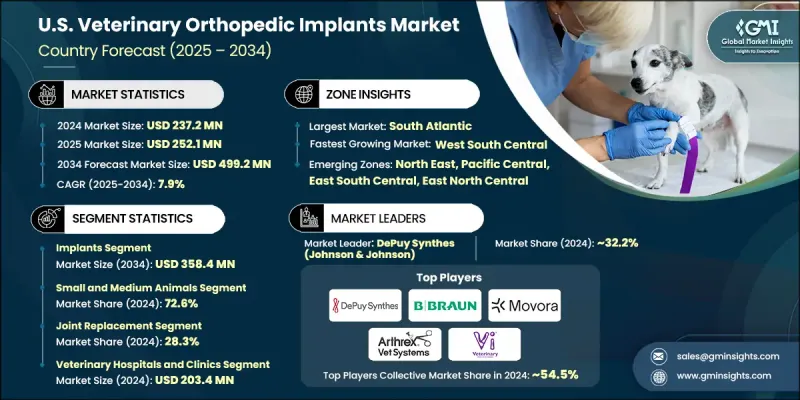

U.S. Veterinary Orthopedic Implants Market was valued at USD 237.2 million in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 499.2 million by 2034.

The market is witnessing substantial growth as pet owners increasingly prioritize advanced medical care for their animals, particularly surgical interventions that restore mobility and enhance quality of life. Veterinary orthopedic implants, including prosthetic joints, screws, plates, wires, and pins, are critical in treating fractures, joint disorders, and bone injuries across various animal species. These devices, commonly made from stainless steel or titanium, are engineered to endure high biomechanical stress while offering long-term durability and functionality. Market growth is further driven by continuous advancements in implant materials such as bioresorbable polymers and titanium-based alloys, which offer improved strength, biocompatibility, and faster healing. Additionally, veterinarians are increasingly opting for implants that align with minimally invasive procedures, enabling reduced recovery times, smaller incisions, and lower post-surgical complications. As veterinary medicine advances, the market continues to benefit from ongoing innovation, increasing surgical precision, and expanding access to orthopedic solutions that promote better outcomes for both companion animals and livestock.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $237.2 Million |

| Forecast Value | $499.2 Million |

| CAGR | 7.9% |

In 2024, the joint replacement segment held a share of 28.3%. This segment includes procedures involving the hip, knee, ankle, and elbow, and is gaining traction due to the growing occurrence of joint-related conditions in animals. The segment is seeing rapid innovation, with a notable shift toward the use of custom-designed, 3D-printed implants that offer better fit, reduce surgical errors, and improve compatibility. These technological advancements are contributing significantly to the broader adoption of joint replacement surgeries across veterinary care practices.

The veterinary hospitals and clinics segment generated USD 203.4 million in 2024 and is expected to witness a CAGR of 8.1% through 2034. These facilities remain the primary centers for diagnosing and managing orthopedic issues such as fractures, ligament damage, and degenerative joint conditions in animals. The growing number of veterinary professionals and advanced surgical infrastructure is enabling better access to high-quality implant procedures. The continuous expansion of clinics and hospitals equipped with specialized orthopedic tools and skilled surgeons is accelerating growth in this segment, making it a vital contributor to the overall market.

Florida Veterinary Orthopedic Implants Market generated USD 10.4 million in 2024. The increase in orthopedic issues, injuries, and age-related bone disorders in pets is fueling demand for innovative surgical implants. The state's growing population of aging animals, combined with rising pet ownership and access to veterinary care, continues to support regional market development and adoption of orthopedic implant solutions.

Leading companies active in the U.S. Veterinary Orthopedic Implants Market include Orthomed, B. Braun, Movora (Vimian Group), AmerisourceBergen Corporation (Cencora), Veterinary Instrumentation, Arthrex Vet Systems, Rita Leibinger, GPC Medical, Integra LifeSciences, Fusion Implants, BlueSAO, Narang Medical Limited, DePuy Synthes (Johnson & Johnson), Ortho Max, and GerVetUSA. To strengthen their position in the market, companies are heavily investing in R&D to develop implants that offer greater biocompatibility and support faster healing. Brands like Veterinary Instrumentation, Arthrex Vet Systems, and GerVetUSA are focusing on expanding their product portfolios with minimally invasive and custom-fit implant systems. Collaborations with veterinary hospitals and academic institutions are enabling deeper market penetration and end-user engagement. Businesses are also enhancing their manufacturing capabilities by introducing precision-engineered implants and improving distribution channels to reach a broader customer base.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Zone trends

- 2.2.3 Product trends

- 2.2.4 Animal type trends

- 2.2.5 Application trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising penetration of pet insurance

- 3.2.1.2 Growing incidence of musculoskeletal disorders in animals

- 3.2.1.3 Rising pet ownership and humanization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of orthopedic procedures and implants

- 3.2.2.2 Post-surgical complications and recovery time

- 3.2.3 Market opportunities

- 3.2.3.1 Emergence of biodegradable and resorbable implants

- 3.2.3.2 Expansion of veterinary specialty hospitals and referral centers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Number of pet owning households, by species (2024)

- 3.7 Pet ownership rates, by leading states (2025)

- 3.8 Pet industry expenditures, 2018 - 2025

- 3.9 Future market trends

- 3.10 Consumer behavior analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Implants

- 5.2.1 Plates

- 5.2.1.1 TPLO plates

- 5.2.1.2 TTA plates

- 5.2.1.3 Trauma plates

- 5.2.1.4 Specialty plates

- 5.2.1.5 Other plates

- 5.2.2 Joint implants

- 5.2.3 Bone screws and anchors

- 5.2.4 Pins and wires

- 5.2.5 Other implants

- 5.2.1 Plates

- 5.3 Instruments

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Small and medium animals

- 6.2.1 Dogs

- 6.2.2 Cats

- 6.2.3 Other small and medium animals

- 6.3 Large animals

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Tibial Plateau Leveling Osteotomy (TPLO)

- 7.3 Tibial Tuberosity Advancement (TTA)

- 7.4 Joint replacement

- 7.4.1 Hip replacement

- 7.4.2 Knee replacement

- 7.4.3 Elbow replacement

- 7.4.4 Ankle replacement

- 7.5 Trauma

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospitals and clinics

- 8.3 Other End use

Chapter 9 Market Estimates and Forecast, By Zone, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North East

- 9.2.1 Connecticut

- 9.2.2 Maine

- 9.2.3 Massachusetts

- 9.2.4 New Hampshire

- 9.2.5 Rhode Island

- 9.2.6 Vermont

- 9.2.7 New Jersey

- 9.2.8 New York

- 9.2.9 Pennsylvania

- 9.3 East North Central

- 9.3.1 Wisconsin

- 9.3.2 Michigan

- 9.3.3 Illinois

- 9.3.4 Indiana

- 9.3.5 Ohio

- 9.4 West North Central

- 9.4.1 North Dakota

- 9.4.2 South Dakota

- 9.4.3 Nebraska

- 9.4.4 Kansas

- 9.4.5 Minnesota

- 9.4.6 Iowa

- 9.4.7 Missouri

- 9.5 South Atlantic

- 9.5.1 Delaware

- 9.5.2 Maryland

- 9.5.3 District of Columbia

- 9.5.4 Virginia

- 9.5.5 West Virginia

- 9.5.6 North Carolina

- 9.5.7 South Carolina

- 9.5.8 Georgia

- 9.5.9 Florida

- 9.6 East South Central

- 9.6.1 Kentucky

- 9.6.2 Tennessee

- 9.6.3 Mississippi

- 9.6.4 Alabama

- 9.7 West South Central

- 9.7.1 Oklahoma

- 9.7.2 Texas

- 9.7.3 Arkansas

- 9.7.4 Louisiana

- 9.8 Mountain States

- 9.8.1 Idaho

- 9.8.2 Montana

- 9.8.3 Wyoming

- 9.8.4 Nevada

- 9.8.5 Utah

- 9.8.6 Colorado

- 9.8.7 Arizona

- 9.8.8 New Mexico

- 9.9 Pacific Central

- 9.9.1 California

- 9.9.2 Alaska

- 9.9.3 Hawaii

- 9.9.4 Oregon

- 9.9.5 Washington

Chapter 10 Company Profiles

- 10.1 AmerisourceBergen Corporation (Cencora)

- 10.2 Arthrex Vet Systems

- 10.3 B. Braun

- 10.4 BlueSAO

- 10.5 DePuy Synthes (Johnson & Johnson)

- 10.6 Fusion Implants

- 10.7 GerVetUSA

- 10.8 GPC Medical

- 10.9 Integra LifeSciences

- 10.10 Movora (Vimian Group)

- 10.11 Narang Medical Limited

- 10.12 Ortho Max

- 10.13 Orthomed

- 10.14 Rita Leibinger

- 10.15 Veterinary Instrumentation