PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1858860

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1858860

Data Lakehouse Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

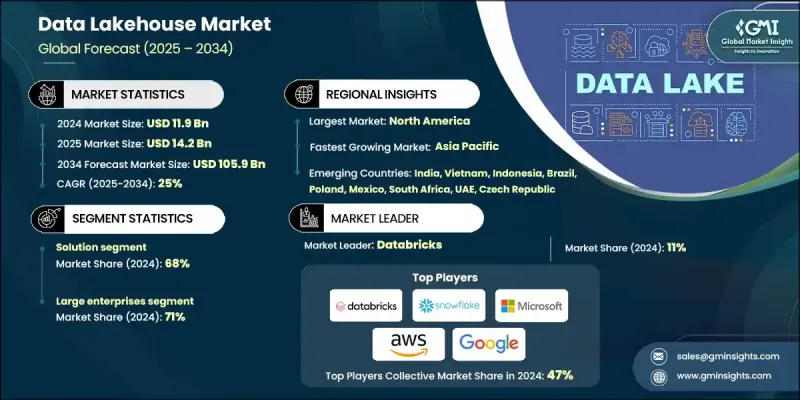

The Global Data Lakehouse Market was valued at USD 11.9 billion in 2024 and is estimated to grow at a CAGR of 25% to reach USD 105.9 billion by 2034.

This remarkable growth stems from organizations increasingly seeking to merge the affordability of data lakes with the analytical capabilities of traditional data warehouses. Lakehouse architecture delivers unified access, enabling scalable analytics, real-time insights, and enhanced AI and machine learning performance. Businesses are prioritizing platforms that reduce silos, improve governance, and support hybrid cloud and on-premises environments, especially in regulated sectors like healthcare and BFSI. With the rising adoption of no-code tools and self-service BI platforms, business users and data professionals beyond IT can now leverage these systems independently. Training ecosystems have also expanded, with more providers emphasizing education and upskilling to ensure organizations feel confident deploying and scaling lakehouse platforms. As hybrid and multi-cloud deployments become the norm, lakehouses are offering enterprises increased agility, centralized data access, and long-term cost efficiency, driving widespread adoption across North America, Europe, and APAC.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.9 Billion |

| Forecast Value | $105.9 Billion |

| CAGR | 25% |

In 2024, the solutions segment held a 68% share and will grow at a CAGR of 23.6% through 2034. Organizations are adopting modern lakehouse technologies that integrate data storage, governance, and analytics into a single platform. This transition is largely driven by the demand for improved operational performance, simplified infrastructure, and support for high-demand workloads like AI and ML. Businesses are favoring cloud-native systems that feature elastic compute, serverless architecture, and separation of storage and compute to increase efficiency while lowering costs.

The large enterprises segment held a 71% share in 2024 and is projected to grow at a CAGR of 24.5% during 2025-2034. These companies are consolidating multiple legacy platforms into unified lakehouse environments to centralize governance, improve collaboration, and reduce redundant workstreams. The lakehouse model allows large organizations to scale AI/ML initiatives, improve analytics capabilities, and ensure better data compliance. Enterprise-wide adoption is accelerating due to the flexibility of hybrid and multi-cloud environments, which also enhance resiliency and cost control.

US Data Lakehouse Market was valued at USD 3.5 billion in 2024. North America remains at the forefront of lakehouse adoption, with the US accounting for the highest regional share. Rapid digital transformation, widespread cloud adoption, and the presence of leading technology vendors have fueled demand for real-time data processing, integrated analytics, and enterprise-scale AI solutions. Sectors like IT, financial services, healthcare, and retail continue to lead demand, supported by robust cloud infrastructure and a highly skilled workforce.

Key players shaping the competitive landscape in the Global Data Lakehouse Market include Google, Databricks, Microsoft, Starburst Data, Dremio, IBM, Amazon Web Services, Snowflake, Cloudera, and Teradata. To strengthen their position in the data lakehouse sector, companies are focusing on expanding their platform capabilities through AI integration, serverless architecture, and enhanced support for multi-cloud deployments. Major vendors are investing heavily in training academies, certifications, and community-building initiatives to upskill enterprise users and deepen customer loyalty. Strategic alliances with cloud providers, technology partners, and industry-specific service integrators are being pursued to expand reach and improve interoperability.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment mode

- 2.2.4 Enterprise size

- 2.2.5 Industry vertical

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Convergence of data lakes & warehouses

- 3.2.1.2 AI/ML and real-time analytics demand

- 3.2.1.3 Cloud vendor ecosystem expansion

- 3.2.1.4 Data democratization & self-service BI

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation & migration costs

- 3.2.2.2 Interoperability & compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Hybrid & multi-cloud deployments

- 3.2.3.2 Industry-specific lakehouse solutions

- 3.2.3.3 Government-led digital transformation & skilling initiatives

- 3.2.3.4 Integration with generative AI & advanced analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Enterprise data architecture modernization trends

- 3.11.1 Legacy system migration patterns

- 3.11.2 Cloud-first vs hybrid adoption strategies

- 3.11.3 Data consolidation & unification initiatives

- 3.11.4 Multi-cloud data strategy evolution

- 3.12 Organizational capability & skills development

- 3.12.1 Data engineering talent market analysis

- 3.12.2 Training & certification program adoption

- 3.12.3 Outsourcing vs in-house development trends

- 3.12.4 Change management & user adoption strategies

- 3.13 Performance & scalability requirements

- 3.13.1 Total cost of ownership analysis framework

- 3.13.2 Cloud cost management & FinOps adoption

- 3.13.3 Resource utilization optimization patterns

- 3.13.4 Value realization & business case development

- 3.14 Vendor selection & partnership strategies

- 3.14.1 Multi-vendor vs single-vendor approach analysis

- 3.14.2 Open source vs proprietary solution evaluation

- 3.14.3 Vendor lock-in mitigation strategies

- 3.14.4 Strategic partnership & alliance patterns

- 3.15 Security & risk management framework

- 3.15.1 Zero trust architecture implementation

- 3.15.2 Data encryption & access control strategies

- 3.15.3 Threat detection & response capabilities

- 3.15.4 Compliance audit & reporting requirements

- 3.16 Investment & funding analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Market concentration analysis

- 4.8 Service delivery model comparison

- 4.9 Professional services ecosystem analysis

- 4.10 Managed services provider landscape

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Data storage

- 5.2.2 Data integration

- 5.2.3 Analytics & BI

- 5.2.4 Governance & security

- 5.2.5 ML/AI tools

- 5.3 Services

- 5.3.1 Professional services

- 5.3.1.1 System integration

- 5.3.1.2 Training & consulting

- 5.3.1.3 Support & maintenance

- 5.3.2 Managed services

- 5.3.1 Professional services

Chapter 6 Market Estimates & Forecast, By Deployment mode, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud-based

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Enterprise size, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 Small & medium enterprises (SMEs)

Chapter 8 Market Estimates & Forecast, By Industry vertical, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 IT & Telecom

- 8.4 Retail & E-commerce

- 8.5 Healthcare

- 8.6 Manufacturing

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Czech Republic

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Amazon Web Services (AWS)

- 10.1.2 Databricks

- 10.1.3 Google

- 10.1.4 IBM

- 10.1.5 Microsoft

- 10.1.6 Oracle

- 10.1.7 Palantir Technologies

- 10.1.8 Snowflake

- 10.2 Regional companies

- 10.2.1 Alteryx

- 10.2.2 Cloudera

- 10.2.3 HPE (Hewlett Packard Enterprise)

- 10.2.4 Informatica

- 10.2.5 Qlik Technologies

- 10.2.6 SAP

- 10.2.7 SAS Institute

- 10.2.8 Teradata

- 10.3 Emerging companies

- 10.3.1 CelerData

- 10.3.2 Dremio

- 10.3.3 Firebolt Analytics

- 10.3.4 Kyvos Insights

- 10.3.5 Onehouse

- 10.3.6 Starburst Data

- 10.3.7 StarTree

- 10.3.8 Tabular Technologies