PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1871096

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1871096

Oil and Gas Heat Exchanger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

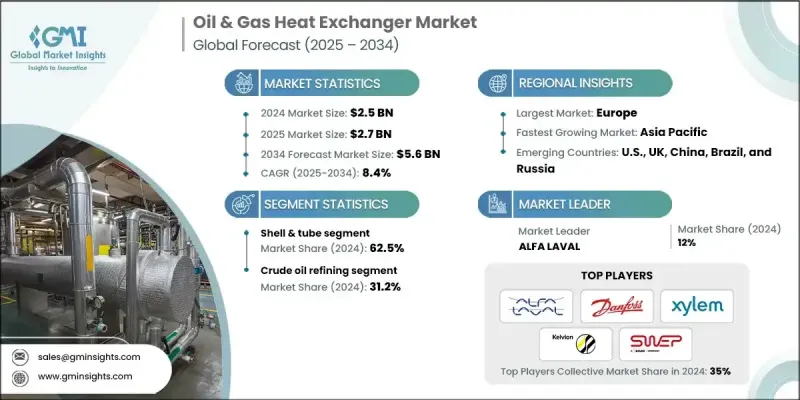

The Global Oil & Gas Heat Exchanger Market was valued at USD 2.5 Billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 5.6 Billion by 2034.

The industry's outlook remains strong as continuous investments in oil and gas infrastructure and rising demand for efficient heating and cooling systems continue to drive growth. Heat exchangers play a vital role in maintaining thermal balance across oil and gas operations by ensuring effective energy transfer between fluid streams, which enhances productivity and reduces operational costs. The growing focus on energy-efficient thermal management across refining, processing, and exploration activities, coupled with technological advancements, is further stimulating market expansion. Increasing adoption of project-specific, customized heat exchangers that ensure precise temperature control and operational reliability is also enhancing market penetration. Moreover, the growing preference for compact and adaptable designs suitable for complex or space-constrained facilities is accelerating product adoption. The shift toward sustainable and cost-effective thermal technologies aimed at improving energy performance and reducing emissions is redefining industry trends and competitiveness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $5.6 Billion |

| CAGR | 8.4% |

The shell and tube segment held a 62.5% share in 2024 and is forecasted to grow at a CAGR of 8% through 2034. This segment continues to gain traction due to its robust use in both crude oil refining and gas processing applications, primarily driven by its high durability and ability to operate under extreme pressure and temperature conditions. Expanding investments in upstream and downstream infrastructure and the continuous need for reliable and efficient thermal performance are supporting this growth trajectory. The introduction of corrosion-resistant materials, improved tube configurations for enhanced heat transfer, and the integration of advanced monitoring systems designed for predictive maintenance and operational optimization are boosting product demand and efficiency across operations.

The crude oil refining application segment held a 31.2% share in 2024 and is expected to grow at a CAGR of 7.5% through 2034. Rising refining capacities worldwide, coupled with an increasing emphasis on optimizing plant performance, are contributing significantly to the segment's growth. Stricter environmental norms encouraging better energy utilization and reduced emissions are further shaping the market landscape. The growing integration of digital technologies, predictive maintenance tools, and high-efficiency heat exchangers designed to improve reliability and extend equipment life is fueling this expansion.

United States Oil & Gas Heat Exchanger Market held a 78% share in 2024, generating USD 452.8 million. The U.S. market is expanding due to the country's strong oil and gas infrastructure, advancements in shale extraction, and rising investments in refining and processing capacities. Increasing focus on modernizing energy infrastructure and the transition toward energy-efficient solutions in alignment with sustainability goals are major drivers behind this growth. Evolving environmental standards and the push toward net-zero objectives are further supporting widespread adoption of advanced heat exchanger systems across the region.

Leading companies operating in the Global Oil & Gas Heat Exchanger Market include ALFA LAVAL, API Heat Transfer, BARRIQUAND Heat Exchanger, Bronswerk, Danfoss, Funke Warmeaustauscher Apparatebau GmbH, HFM, HISAKA WORKS LTD., HRS Heat Exchangers, KAM Thermal Equipment LTD, Kelvion Holding GmbH, Mersen, Metalforms LLC, Nexson Group, SPX Flow, SWEP International, Thermofin, TITAN Metal Fabricators, Tranter, Turnbull & Scott Group, and Xylem. Key players in the Oil & Gas Heat Exchanger Market are actively adopting several strategies to enhance their market presence and competitiveness. Companies are focusing on expanding their global production capabilities and strengthening their supply chains to meet increasing demand. Strategic collaborations and mergers are enabling technology sharing and portfolio diversification. Firms are heavily investing in R&D to develop high-performance, corrosion-resistant, and energy-efficient heat exchangers tailored to evolving industry requirements. Integration of digital monitoring systems and predictive maintenance technologies is being prioritized to enhance operational reliability and reduce downtime.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 Cost structure analysis of oil & gas heat exchangers

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Shell & tube

- 5.3 Plate

- 5.4 Air cooled

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Onshore production facilities

- 6.3 Crude oil refining

- 6.4 Petrochemical processing

- 6.5 LNG facilities

- 6.6 Pipeline systems

- 6.7 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Russia

- 7.3.5 Italy

- 7.3.6 Spain

- 7.3.7 Poland

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 India

- 7.4.5 Indonesia

- 7.4.6 Malaysia

- 7.4.7 Thailand

- 7.4.8 Vietnam

- 7.4.9 Philippines

- 7.4.10 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Egypt

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Colombia

- 7.6.4 Chile

Chapter 8 Company Profiles

- 8.1 ALFA LAVAL

- 8.2 API Heat Transfer

- 8.3 BARRIQUAND Heat Exchanger

- 8.4 Bronswerk

- 8.5 Danfoss

- 8.6 Funke Warmeaustauscher Apparatebau GmbH

- 8.7 HFM

- 8.8 HISAKA WORKS LTD.

- 8.9 HRS Heat Exchangers

- 8.10 KAM Thermal Equipment, LTD

- 8.11 Kelvion Holding GmbH

- 8.12 Mersen

- 8.13 Metalforms, LLC

- 8.14 Nexson Group

- 8.15 SPX Flow

- 8.16 SWEP International

- 8.17 Thermofin

- 8.18 TITAN Metal Fabricators

- 8.19 Tranter

- 8.20 Turnbull & Scott Group

- 8.21 Xylem