PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1871132

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1871132

Electric Vehicle Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

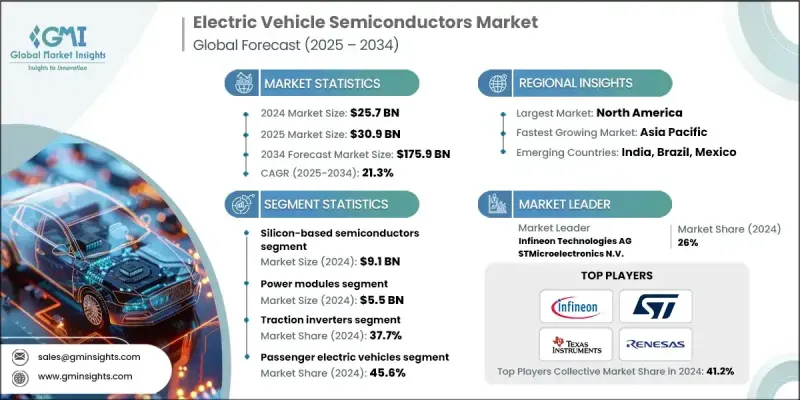

The Global Electric Vehicle Semiconductors Market was valued at USD 25.7 Billion in 2024 and is estimated to grow at a CAGR of 21.3% to reach USD 175.9 Billion by 2034.

The market is expanding as the global shift toward carbon neutrality and lower greenhouse gas emissions drives widespread adoption of electric vehicles (EVs). Governments and regulatory authorities worldwide are enforcing strict emission regulations while introducing incentives, rebates, and subsidies to promote EV usage. Consumers increasingly prefer sustainable mobility alternatives over traditional combustion vehicles, further boosting demand. This surge in EV adoption has led to an accelerated requirement for advanced semiconductors, which serve as the technological backbone of electric vehicles. They enable efficient powertrain control, energy optimization, infotainment, and safety systems. Sustainability mandates have become a primary force shaping semiconductor innovation within the EV ecosystem. The industry is undergoing a major transition from conventional silicon-based semiconductors to next-generation materials such as silicon carbide (SiC) and gallium nitride (GaN). These wide-bandgap semiconductors provide superior energy efficiency, faster switching, and improved thermal management, essential for handling high-power operations in EVs. Their ability to make vehicle power systems more compact, lightweight, and efficient enhances range, charging speed, and overall performance. Automakers and semiconductor companies are rapidly integrating SiC and GaN technologies to replace legacy materials, increasing their competitive advantage and addressing the evolving global EV demand.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25.7 Billion |

| Forecast Value | $175.9 Billion |

| CAGR | 21.3% |

The silicon-based semiconductors segment generated USD 9.1 Billion in 2024. The strong position of this segment is attributed to the maturity and cost-efficiency of silicon technology, supported by established global manufacturing capabilities. These semiconductors deliver reliable performance, scalability, and compatibility with current automotive systems, making them the preferred option for mass-produced EV models. Their extensive use in power management systems and vehicle control units continues to strengthen their market relevance as the EV industry scales.

The power modules segment generated USD 5.5 Billion in 2024. The demand for power modules stems from their ability to consolidate multiple power devices into compact, high-efficiency packages that enhance energy conversion and thermal regulation. This functionality is vital for powering electric drivetrains, charging systems, and inverters in both hybrid and fully electric vehicles. The continuous focus on achieving higher system reliability and reducing thermal losses keeps power modules at the forefront of EV semiconductor innovation.

U.S. Electric Vehicle Semiconductors Market will grow at a CAGR of 21.8% by 2034. Growth is strongly supported by federal and state-level incentives, EV mandates, and growing consumer adoption. Domestic automakers increasingly incorporate SiC-based power chips to enhance drivetrain efficiency, performance computing, and autonomous driving integration. The U.S. also benefits from local semiconductor production supported by the CHIPS Act, fostering innovation and supply chain resilience. Collaboration among automakers, semiconductor firms, and technology providers is driving next-generation developments in battery management systems, autonomous processors, and high-performance charging modules, ensuring sustained competitiveness within the EV ecosystem.

Key players active in the Electric Vehicle Semiconductors Market include Wolfspeed, Inc., NXP Semiconductors N.V., STMicroelectronics N.V., Texas Instruments Inc., Infineon Technologies AG, Microchip Technology Inc., Analog Devices, Inc., Renesas Electronics Corporation, ON Semiconductor Corporation, Power Integrations, Inc., Melexis N.V., Monolithic Power Systems, Inc., ROHM Co., Ltd., Toshiba Electronic Devices & Storage, Allegro MicroSystems, Inc., ams OSRAM AG, StarPower Semiconductor Ltd., Samsung Semiconductor, Inc., Sanken Electric Co., Ltd., and BYD Semiconductor Co., Ltd. Leading companies in the Electric Vehicle Semiconductors Market are implementing strategic initiatives to reinforce their competitive edge and expand their technological footprint. They are increasing R&D investment to accelerate advancements in wide-bandgap materials like SiC and GaN, targeting higher performance and energy efficiency. Firms are entering long-term supply partnerships with automotive OEMs to secure semiconductor integration across new EV platforms. Localization of manufacturing, supported by government policies, is enhancing supply stability and cost competitiveness.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Packaging type trends

- 2.2.2 Material trends

- 2.2.3 Application trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid EV adoption driven by global sustainability goals

- 3.2.1.2 Advancements in power electronics (SiC & GaN technologies)

- 3.2.1.3 Government incentives and regulatory mandates for electrification

- 3.2.1.4 Growing demand for autonomous and connected EVs

- 3.2.1.5 Expansion of EV charging infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing and R&D costs of advanced semiconductors

- 3.2.2.2 Global supply chain constraints & chip shortages

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2021-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2025-2034)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability ROI analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Silicon-based semiconductors

- 5.3 Silicon Carbide (SiC) semiconductors

- 5.4 Gallium Nitride (GaN) semiconductors

- 5.5 Ultra-wide bandgap semiconductors

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Power modules

- 6.3 Discrete power devices

- 6.4 Power management ICs

- 6.5 Microcontrollers & processors

- 6.6 Sensor ICs

- 6.7 Gate driver ICs

- 6.8 Communication & interface ICs

- 6.9 Memory & storage ICs

- 6.10 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Traction inverters

- 7.3 Onboard Chargers (OBC)

- 7.4 DC-DC converters

- 7.5 Wireless power transfer

- 7.6 Ultra-fast charging systems

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Passenger electric vehicles

- 8.3 Commercial electric vehicles

- 8.4 Specialized electric vehicles

- 8.5 EV charging infrastructure

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Allegro MicroSystems, Inc.

- 10.2 Alpha and Omega Semiconductor Ltd.

- 10.3 ams OSRAM AG

- 10.4 Analog Devices, Inc.

- 10.5 BYD Semiconductor Co., Ltd.

- 10.6 Diodes Incorporated

- 10.7 Infineon Technologies AG

- 10.8 IXYS Corporation

- 10.9 Melexis N.V.

- 10.10 Microchip Technology Inc.

- 10.11 Monolithic Power Systems, Inc.

- 10.12 NXP Semiconductors N.V.

- 10.13 ON Semiconductor Corporation

- 10.14 Power Integrations, Inc.

- 10.15 Powerex, Inc.

- 10.16 Qorvo, Inc.

- 10.17 Renesas Electronics Corporation

- 10.18 ROHM Co., Ltd.

- 10.19 Samsung Semiconductor, Inc.

- 10.20 Sanken Electric Co., Ltd.

- 10.21 StarPower Semiconductor Ltd.

- 10.22 STMicroelectronics N.V.

- 10.23 Texas Instruments Inc.

- 10.24 Toshiba Electronic Devices & Storage

- 10.25 Wolfspeed, Inc.