PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1871163

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1871163

Cryogenic Valve for Aerospace Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

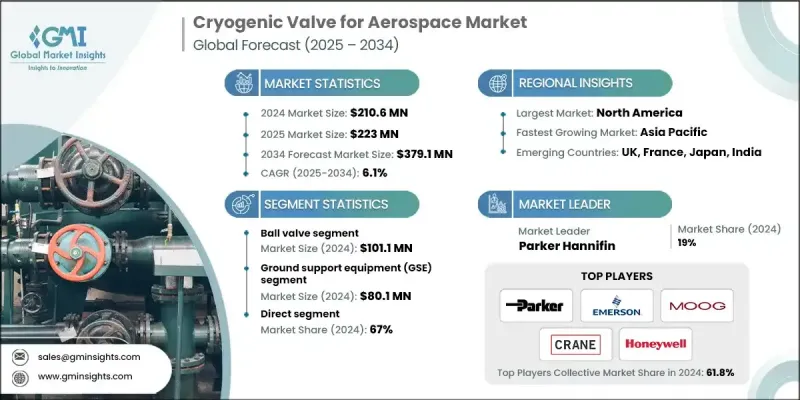

The Global Cryogenic Valve for Aerospace Market was valued at USD 210.6 million in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 379.1 million by 2034.

The continuous rise in space exploration missions and the increasing use of cryogenic fuels such as liquid oxygen and hydrogen are key drivers boosting the need for specialized cryogenic valves. These valves play a vital role in handling extremely low-temperature fluids safely and efficiently, ensuring precision and reliability during space launches and propulsion processes. As aerospace technology evolves, cryogenic valve systems are being refined to deliver enhanced control, operational safety, and durability under high-stress conditions. Advancements in materials, design, and automation have improved their performance, enabling precise flow control and leak-free operation across both orbital and terrestrial aerospace applications. Growing demand from commercial space programs, satellite deployments, and deep-space exploration projects continues to fuel product development. Furthermore, the integration of smart sensors and monitoring systems into cryogenic valves is transforming operational efficiency by enabling real-time tracking and predictive maintenance, which are essential for mission-critical aerospace operations worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $210.6 Million |

| Forecast Value | $379.1 Million |

| CAGR | 6.1% |

The ball valve segment generated USD 101.1 million in 2024. The segment's leadership can be attributed to its robust sealing capabilities and adaptability to the demanding conditions of aerospace environments. Ball valves are particularly valued for their ability to maintain stable performance under extreme temperature shifts, vibration, and pressure variations. Their reliability makes them indispensable in propulsion systems, fuel lines, and cryogenic storage tanks where consistent flow regulation is crucial. Additionally, the industry's ongoing efforts to develop specialized alloys and materials that prevent freezing or cracking under cryogenic temperatures further enhance the adoption of ball valves in aerospace systems.

The ground support equipment (GSE) segment generated USD 80.1 million in 2024. This segment is integral to supporting launch and maintenance operations through refueling, venting, and cooling procedures. The efficiency of GSE systems directly impacts launch frequency and turnaround times for aerospace missions. Continuous upgrades in GSE design and performance have significantly improved operational readiness and safety in space programs. Their contribution to reducing pre-launch cycles has strengthened their role as an essential component of modern aerospace infrastructure, enhancing reliability and mission consistency.

United States Cryogenic Valve for Aerospace Market held an 87.5% share in 2024. This leadership is driven by the country's advanced aerospace capabilities, ongoing investment in cryogenic systems, and the presence of major manufacturing players. The U.S. maintains a competitive advantage due to its strong focus on research, technological innovation, and the continuous expansion of both commercial and government space programs. The robust domestic supply chain, combined with an established regulatory framework and infrastructure for cryogenic fuel handling, reinforces the country's leading role in regional and global market growth.

Prominent companies operating in the Cryogenic Valve for Aerospace Market include Woodward, Flowserve, Moog, Parker Hannifin, Baker Hughes, Precision Fluid Controls, Herose, SAMSON, Cryofab, Inc., Bray International, Kitz, Crane Company, BAC Valves, Honeywell, and Emerson. Key strategies adopted by major companies in the Cryogenic Valve for Aerospace Market focus on innovation, strategic partnerships, and technological advancement. Industry leaders are investing in advanced materials and smart valve technologies to enhance reliability and real-time performance monitoring under extreme conditions. Collaborations with aerospace agencies and private space enterprises are helping tailor solutions for high-precision applications like propulsion and fuel management. Companies are also expanding global manufacturing capabilities to meet the increasing demand for cryogenic systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Valve type

- 2.2.3 Valve size

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in space exploration & launch programs

- 3.2.1.2 Rise of commercial aerospace & satellite deployment

- 3.2.1.3 Advancements in cryogenic technologies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Extreme operating conditions

- 3.2.2.2 High cost & long development cycles

- 3.2.3 Opportunities

- 3.2.3.1 Hydrogen-powered aircraft development

- 3.2.3.2 High cost & long development cycles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Valve type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Valve type, 2021-2034 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Ball valves

- 5.3 Globe valves

- 5.4 Gate valves

- 5.5 Check valves

- 5.6 Butterfly valves

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Valve size, 2021-2034 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Small Valves (≤2 inches)

- 6.3 Medium Valves (2-6 inches)

- 6.4 Large Valves (6-12 inches)

- 6.5 Extra-Large Valves (>12 inches)

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Aircraft systems

- 7.3 Ground support equipment (GSE)

- 7.4 Aerospace manufacturing and testing

- 7.5 Defense and military applications

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Baker Hughes

- 10.2 Bray International

- 10.3 BAC Valves

- 10.4 Crane Company

- 10.5 Cryofab, Inc.

- 10.6 Emerson

- 10.7 Flowserve

- 10.8 Honeywell

- 10.9 Herose

- 10.10 Kitz

- 10.11 SAMSON

- 10.12 Moog

- 10.13 Parker Hannifin

- 10.14 Precision Fluid Controls

- 10.15 Woodward