PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876542

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876542

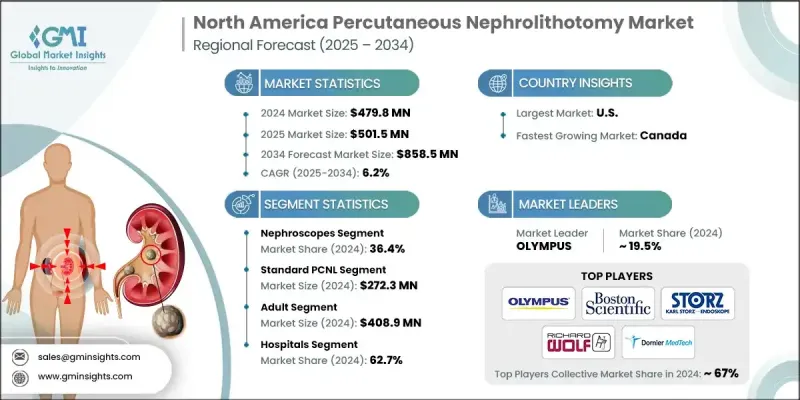

North America Percutaneous Nephrolithotomy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

North America Percutaneous Nephrolithotomy Market was valued at USD 479.8 million in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 858.5 million by 2034.

The growth is driven by advancements in minimally invasive urology, a well-established healthcare infrastructure, an increasing incidence of kidney stones, and favorable reimbursement frameworks. Percutaneous nephrolithotomy (PCNL) is a minimally invasive surgical approach used for removing large or complex kidney stones that cannot be effectively treated with extracorporeal shockwave lithotripsy or ureteroscopy. The technique involves a small incision in the patient's back to access the kidney using a nephroscope, allowing stone fragmentation and removal with minimal tissue trauma and shorter recovery times. Ongoing innovations such as mini-PCNL, ultra-mini PCNL, and micro-PCNL have significantly improved procedural precision and safety. Enhanced visualization equipment, image-guided systems, and technologically advanced nephroscopes are further optimizing outcomes by reducing complication risks, shortening hospital stays, and improving surgical efficiency across hospitals and ambulatory care centers in the region.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $479.8 Million |

| Forecast Value | $858.5 Million |

| CAGR | 6.2% |

The nephroscopes segment held a share of 36.4% in 2024, maintaining dominance due to increasing use of high-definition and digital flexible nephroscopes. These instruments enhance procedural visualization, minimize operation time, and contribute to improved patient outcomes during complex kidney stone surgeries. The growing number of renal calculi cases in the U.S. and Canada continues to fuel demand for nephroscopes, which are indispensable in PCNL procedures. As hospitals perform higher volumes of kidney stone surgeries, the adoption of advanced nephroscopic systems grows accordingly to support precision and consistency in treatment.

The standard PCNL segment generated USD 272.3 million in 2024 and is projected to grow at a CAGR of 6.1% through 2034. Standard PCNL remains the preferred method for patients presenting with complex anatomical variations such as horseshoe kidneys, calyceal diverticula, or ureteropelvic junction obstructions, where other approaches prove less effective. Supported by well-equipped operating facilities and experienced surgical teams, standard PCNL procedures benefit from established clinical workflows and reliable supply chains for surgical tools like sheaths, dilators, nephroscopes, and access kits. These factors ensure procedural continuity and widespread adoption across both large hospitals and regional medical centers.

U.S. Percutaneous Nephrolithotomy Market was valued at USD 450.8 million in 2024. With recurrence rates of kidney stones reaching up to 50% within five years, the U.S. continues to see a steady influx of patients requiring PCNL for complete stone removal. This recurring patient base ensures consistent demand for urology procedures nationwide. The integration of AI-driven surgical planning tools and navigation technologies is further advancing precision and efficiency in PCNL surgeries, supporting high-quality outcomes and expanding procedural adoption.

Prominent players active in the North America Percutaneous Nephrolithotomy Market include Teleflex, KARL STORZ, Olympus, Becton, Dickinson and Company, EMS Electro Medical Systems, Boston Scientific, COOK Medical, ADVIN, Richard Wolf, ELMED, B. Braun, Coloplast, and Dornier MedTech. Leading companies in the North America Percutaneous Nephrolithotomy Market are focusing on product innovation, partnerships, and portfolio diversification to strengthen their regional presence. Firms are developing next-generation nephroscopes and surgical instruments with enhanced imaging, flexibility, and miniaturized designs to reduce invasiveness and improve precision. Collaborations with hospitals and urology centers are helping manufacturers refine device functionality through clinical feedback. Many players are expanding their regional distribution networks to ensure better accessibility across the U.S. and Canada. Additionally, investments in R&D and integration of AI-assisted visualization and navigation systems are helping companies stay competitive.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional

- 1.3.2 Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Procedure type trends

- 2.2.4 Patient trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements in PCNL instruments

- 3.2.1.2 Rising healthcare expenditure and hospital investments

- 3.2.1.3 Increasing prevalence of kidney stone disease

- 3.2.1.4 Growing number of trained endourologists and centers of excellence

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Shortage of skilled surgeons in some regions

- 3.2.2.2 Stringent regulatory and quality compliance requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Market penetration in underserved U.S. and Canadian regions

- 3.2.3.2 Expansion into ambulatory surgical centers and outpatient settings

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Canada

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Value chain analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Gap analysis

- 3.12 Start-up scenario

- 3.13 Consumer behaviour insights

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Nephroscopes

- 5.2.1 Rigid

- 5.2.2 Flexible

- 5.3 Lithotripsy systems

- 5.4 Access systems

- 5.5 Other product types

Chapter 6 Market Estimates and Forecast, By Procedure Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Standard PCNL

- 6.3 Mini-PCNL

- 6.4 Micro-PCNL

Chapter 7 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Adult

- 7.3 Pediatric

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other End use

Chapter 9 Market Estimates and Forecast, By Country, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 U.S.

- 9.3 Canada

Chapter 10 Company Profiles

- 10.1 ADVIN

- 10.2 B. BRAUN

- 10.3 Becton, Dickinson and Company

- 10.4 Boston Scientific

- 10.5 Coloplast

- 10.6 COOK MEDICAL

- 10.7 Dornier MedTech

- 10.8 ELMED

- 10.9 EMS ELECTRO MEDICAL SYSTEMS

- 10.10 KARL STORZ

- 10.11 OLYMPUS

- 10.12 Richard Wolf

- 10.13 Teleflex