PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876548

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876548

Automotive Digital Factory Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

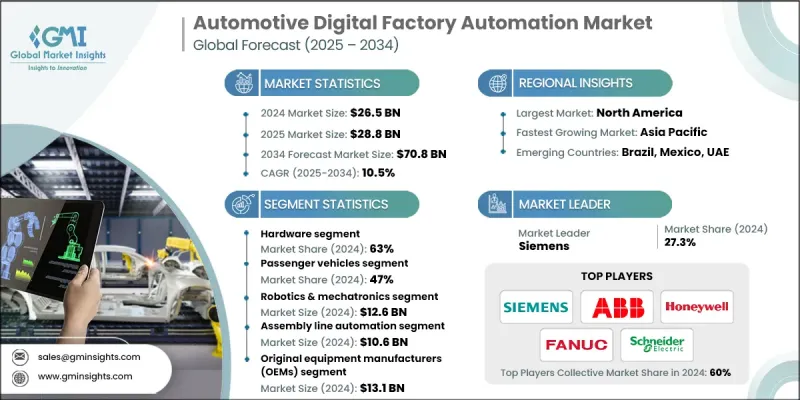

The Global Automotive Digital Factory Automation Market was valued at USD 26.5 billion in 2024 and is estimated to grow at a CAGR of 10.5% to reach USD 70.8 billion by 2034.

The market is experiencing strong momentum as the automotive industry increasingly embraces smart manufacturing and digital transformation. Manufacturers are prioritizing operational efficiency, real-time data insights, and flexible production systems to stay competitive in a rapidly evolving landscape. The integration of Industry 4.0 technologies, artificial intelligence, and IoT-enabled monitoring platforms is transforming traditional automotive facilities into intelligent, data-driven production environments. These digital factory systems optimize productivity, reduce equipment downtime, and enhance quality assurance through predictive maintenance and automated process control. By combining digital twin simulations, robotics, AI-based analytics, and IoT connectivity, companies are achieving seamless coordination across the entire production cycle. This convergence not only supports sustainability goals and energy efficiency but also enables full lifecycle visibility, improved compliance, and greater manufacturing resilience. The growing need for interconnected, adaptive, and transparent manufacturing networks is driving continued investment in digital factory automation across both OEMs and suppliers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $26.5 Billion |

| Forecast Value | $70.8 Billion |

| CAGR | 10.5% |

The hardware segment accounted for about 63% of the market in 2024 and is anticipated to expand at a CAGR of 10.8% from 2025 to 2034. Hardware remains the foundation of automotive digital factory automation, playing a critical role in enabling real-time tracking, data collection, and machine control throughout production lines. Key hardware elements include IoT sensors, PLCs, RFID systems, embedded controllers, and machine vision devices that ensure seamless operation, predictive maintenance, and high productivity. Automakers and suppliers depend on these systems to maintain precision, reduce errors, and optimize production performance while enabling scalable digital transformation across facilities.

The passenger vehicle segment held 47% share in 2024 and is expected to grow at a CAGR of 11.3% between 2025 and 2034. Rising demand for electric and hybrid vehicles, coupled with stricter environmental regulations, is accelerating automation investments in passenger vehicle production. Automotive manufacturers are leveraging digital factory solutions such as robotics, cloud-integrated platforms, and AI-powered analytics to improve process accuracy, ensure compliance, and increase output efficiency. These technologies provide real-time visibility into production metrics and enhance the ability to manage complex, high-volume assembly operations with minimal downtime.

U.S. Automotive Digital Factory Automation Market held 88% share and generated USD 8.5 billion in 2024. The nation's strong manufacturing base, combined with rapid adoption of digital and AI technologies, is fueling large-scale modernization of automotive plants. Advanced robotics, IoT-enabled monitoring, and digital twin technologies are being increasingly integrated into production and supply chain systems. This expansion supports better resource utilization, reduced waste, and improved product quality while reinforcing the industry's sustainability and innovation goals.

Key players operating in the Global Automotive Digital Factory Automation Market include Mitsubishi Electric, Schneider Electric, FANUC, Siemens, ABB, Emerson Electric, Honeywell International, JR Automation Technologies, Rockwell Automation, and Yokogawa Electric. Leading companies in the Global Automotive Digital Factory Automation Market are focusing on technological innovation, strategic partnerships, and global expansion to strengthen their market presence. They are investing heavily in advanced robotics, digital twin technologies, and AI-driven analytics to enhance precision and streamline manufacturing processes. Collaborations between automation providers and automotive OEMs are enabling the creation of customized, end-to-end automation ecosystems. Companies are also emphasizing sustainability by integrating energy-efficient hardware and optimizing resource utilization through smart monitoring systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Labor shortage mitigation requirements

- 3.2.1.2 Quality & consistency improvement demands

- 3.2.1.3 Production flexibility & customization needs

- 3.2.1.4 Cost reduction & operational efficiency pressures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment requirements

- 3.2.2.2 Legacy system integration challenges

- 3.2.3 Market opportunities

- 3.2.3.1 5G network implementation in factories

- 3.2.3.2 Edge computing & real-time analytics

- 3.2.3.3 Blockchain for supply chain traceability

- 3.2.3.4 AI-driven predictive maintenance expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Safety and Quality Standards

- 3.4.2 Environmental and Sustainability Regulations

- 3.4.3 Data Privacy and Cybersecurity

- 3.4.4 Industry-specific Standards

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 5G Network Integration in Manufacturing

- 3.7.2 Edge Computing & Real-time Analytics

- 3.7.3 Blockchain for Supply Chain Transparency

- 3.7.4 Augmented Reality & Virtual Reality Applications

- 3.7.5 Cybersecurity Evolution in Industrial Systems

- 3.7.6 Human-Machine Interface Advancements

- 3.7.7 Digital Twin Evolution & Metaverse Integration

- 3.7.8 Autonomous Factory Concepts

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

- 3.14 Risk assessment framework

- 3.14.1 Cybersecurity risk management

- 3.14.2 Operational risk assessment

- 3.14.3 Financial risk analysis

- 3.14.4 Supply chain risk mitigation

- 3.15 Best case scenarios

- 3.16 Future Outlook & Strategic Recommendations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Industrial robots

- 5.2.2 Control systems

- 5.2.3 Sensors & vision systems

- 5.2.4 Human-machine interface (HMI)

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Manufacturing execution systems (MES)

- 5.3.2 Digital twin & simulation software

- 5.3.3 Predictive maintenance & analytics platforms

- 5.3.4 AI & machine learning platforms

- 5.3.5 ERP / cloud integration

- 5.4 Services

- 5.4.1 Installation & commissioning

- 5.4.2 Maintenance & support

- 5.4.3 Consulting & system integration

- 5.4.4 Retrofit & modernization services

- 5.4.5 Training & workforce development

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

- 6.4 Two-Wheelers

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Robotics & mechatronics

- 7.3 Industrial IoT & sensors

- 7.4 AI & machine learning

- 7.5 Digital twin & simulation

- 7.6 Cloud & edge computing

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($ Bn, Units)

- 8.1 Key trends

- 8.2 Assembly line automation

- 8.3 Welding & joining operations

- 8.4 Painting & coating processes

- 8.5 Quality control & inspection

- 8.6 Material handling & logistics

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($ Bn, Units)

- 9.1 Key trends

- 9.2 Original equipment manufacturers (OEMs)

- 9.3 Tier 1 Suppliers

- 9.4 Tier 2 Suppliers

- 9.5 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 ABB

- 11.1.2 Bosch Rexroth

- 11.1.3 Emerson Electric

- 11.1.4 FANUC

- 11.1.5 General Electric

- 11.1.6 Honeywell International

- 11.1.7 Rockwell Automation

- 11.1.8 Schneider Electric

- 11.1.9 Siemens

- 11.2 Regional Player

- 11.2.1 Festo

- 11.2.2 JR Automation Technologies

- 11.2.3 Keyence

- 11.2.4 KUKA

- 11.2.5 Mitsubishi Electric

- 11.2.6 Omron

- 11.2.7 UL Solutions

- 11.2.8 Vention

- 11.2.9 Yokogawa Electric

- 11.3 Emerging Players

- 11.3.1 Augury Systems

- 11.3.2 Bright Machines

- 11.3.3 MachineMetrics

- 11.3.4 Path Robotics

- 11.3.5 Sight Machine

- 11.3.6 Standard Bots

- 11.3.7 Tulip Interfaces