PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876554

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876554

Health-Monitoring Car Seat Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

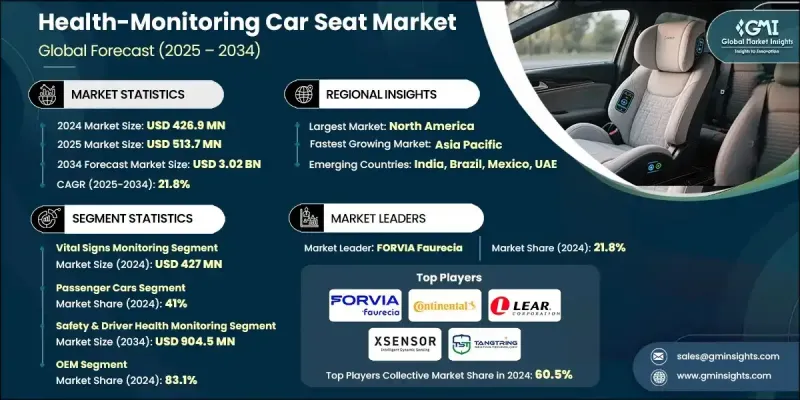

The Global Health-Monitoring Car Seat Market was valued at USD 426.9 million in 2024 and is estimated to grow at a CAGR of 21.8% to reach USD 3.02 billion by 2034.

The rising focus on personal health and wellness is driving the demand for smart automotive seats equipped with health-monitoring technologies. Consumers are increasingly prioritizing safety features that track vital signs, fatigue, and stress, encouraging automakers to integrate biometric sensors and AI-enabled wellness systems. Advances in wearable electrodes, sensors, and artificial intelligence now enable real-time monitoring of occupants' heart rate, respiration, and posture, allowing predictive health alerts, personalized comfort, and enhanced driving safety. In terms of units, the market is expected to expand from over 322K in 2024 to 856K by 2030. As vehicles become more connected and autonomous, in-cabin health monitoring is emerging as a key differentiator, enabling continuous tracking of occupant wellbeing and supporting proactive safety measures.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $426.9 Million |

| Forecast Value | $3.02 Billion |

| CAGR | 21.8% |

The vital signs monitoring segment generated USD 427 million in 2024 and will grow at a CAGR of 21.3% through 2034. This segment captures heart rate, blood pressure, and respiration via capacitive ECG sensors embedded in the seat, delivering reliable and consistent signals. It is particularly popular among commercial fleets and high-end vehicle manufacturers, driven by regulatory requirements and growing consumer awareness of driver health.

The passenger cars segment held a share of 41% in 2024, as SUVs and sedans increasingly incorporate AI-enabled seat systems that monitor vital signs, posture, and fatigue, providing real-time alerts and customizable comfort.

U.S. Health-Monitoring Car Seat Market held 85.4% share in 2024, valued at USD 72.8 million. US automakers are spearheading the integration of health-monitoring technologies, particularly in premium vehicle segments. Regulatory frameworks focusing on commercial driver health further encourage the adoption of such systems in fleet operations, promoting occupant safety and well-being.

Key players in the Global Health-Monitoring Car Seat Market include Tangtring Seating Technology, ZF Friedrichshafen AG, Visteon Corporation, Continental AG, NOVELDA, Robert Bosch GmbH, FORVIA Faurecia, Lear, Yanfeng, and XSENSOR Technology. Companies in the health-monitoring car seat market are adopting several strategies to strengthen their market presence and expand their foothold. They are investing in research and development to enhance sensor accuracy, AI-driven analytics, and seat comfort features. Collaborations with automakers and health technology providers accelerate innovation and integration of advanced monitoring systems. Firms are focusing on product differentiation through customizable and predictive wellness features that enhance safety and user experience.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Feature

- 2.2.2 Vehicle

- 2.2.3 Sales channel

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising health awareness

- 3.2.1.2 Technological advancements in sensors and ai

- 3.2.1.3 Regulatory and safety standards

- 3.2.1.4 Connected and autonomous vehicle growth

- 3.2.1.5 Increasing consumer demand for personalized in-cabin experience

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation cost

- 3.2.2.2 Data privacy and security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with wearables and health apps

- 3.2.3.2 Expansion in electric and premium vehicles

- 3.2.3.3 Ai-driven predictive health analytics

- 3.2.3.4 Emerging markets and urbanization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle east and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technology

- 3.7.2 Emerging technology

- 3.8 Patent analysis

- 3.9 Price Trends Analysis

- 3.9.1 By component

- 3.9.2 By region

- 3.10 Cost Breakdown Analysis

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon Footprint Considerations

- 3.13 Future trends

- 3.14 Major market trends and disruptions

- 3.15 Cost-benefit analysis & roi models

- 3.15.1 Total cost of ownership analysis

- 3.15.2 Return on investment calculations

- 3.15.3 Cost reduction roadmap(15-20% decline by 2030)

- 3.15.4 Value proposition by market segment

- 3.16 User experience & human factors

- 3.16.1 Ergonomic design considerations

- 3.16.2 User acceptance & adoption barriers

- 3.16.3 Cultural & regional preferences

- 3.16.4 Accessibility & universal design

- 3.17 Future outlook & technology roadmap

- 3.17.1 Technology evolution roadmap (2025-2035)

- 3.17.2 Emerging applications & use cases

- 3.17.3 Integration with autonomous vehicles

- 3.17.4. 5 G & edge computing impact

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key news and initiatives

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Feature, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Vital signs monitoring

- 5.3 Posture/seat-pressure monitoring

- 5.4 Fatigue/drowsiness detection

- 5.5 Biometric sensing

- 5.6 Thermal / occupant comfort sensing

- 5.7 Multi-parameter / integrated sensing

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 LCV

- 6.3.2 MCV

- 6.3.3 HCV

- 6.4 Electric vehicle

- 6.4.1 BEV

- 6.4.2 PHEV

- 6.4.3 FCEV

Chapter 7 Market Estimates & Forecast, By Sales channel 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.1.1 Safety & driver health monitoring

- 8.1.2 Comfort & ergonomics enhancement

- 8.1.3 Wellness / preventive health

- 8.1.4 Fleet driver monitoring

- 8.1.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Netherlands

- 9.3.8 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 ANZ

- 9.4.5 Singapore

- 9.4.6 Thailand

- 9.4.7 Vietnam

- 9.4.8 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Continental AG

- 10.1.2 Denso Corporation

- 10.1.3 FORVIA (Faurecia)

- 10.1.4 Lear

- 10.1.5 Magna International Inc.

- 10.1.6 Robert Bosch GmbH

- 10.1.7 Valeo SA

- 10.1.8 ZF Friedrichshafen AG

- 10.2 Regional players

- 10.2.1 Aptiv PLC

- 10.2.2 Autoliv AB

- 10.2.3 Gentex Corporation

- 10.2.4 HARMAN International (Samsung)

- 10.2.5 Hyundai Mobis

- 10.2.6 Infineon Technologies AG

- 10.2.7 Joyson Safety Systems

- 10.2.8 NOVELDA

- 10.2.9 Tangtring Seating Technology Inc.

- 10.2.10 Visteon Corporation

- 10.2.11 XSENSOR Technology

- 10.2.12 Yanfeng

- 10.3 Technology Specialists (Components / Sensors)

- 10.3.1 NXP Semiconductors

- 10.3.2 Sensirion AG

- 10.3.3 STMicroelectronics

- 10.3.4 TDK Corporation

- 10.3.5 TE Connectivity

- 10.3.6 Texas Instruments

- 10.4 Emerging Players / Startups

- 10.4.1 Comfort Motion Global

- 10.4.2 ContinUse Biometrics

- 10.4.3 Neteera Technologies