PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876556

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876556

Polyimide Films for Electronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

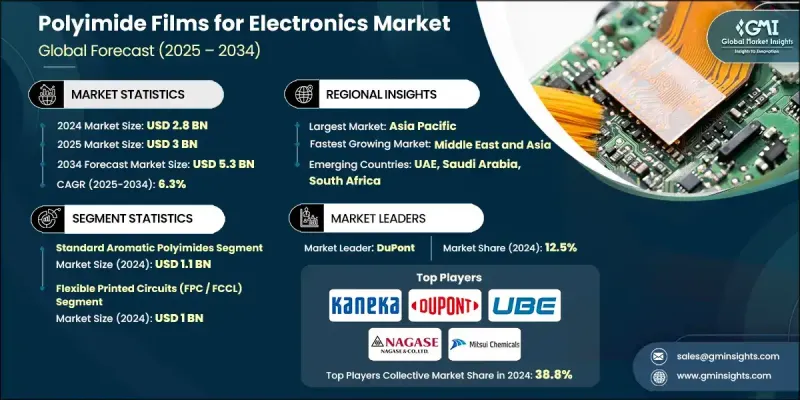

The Global Polyimide Films for Electronics Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 5.3 billion by 2034.

Polyimide films are advanced polymer materials widely recognized for their exceptional thermal stability, chemical resistance, and mechanical strength. These films are used extensively in the electronics industry due to their ability to maintain insulation properties under extreme temperatures. Produced through the polymerization of diamines and dianhydrides, polyimide films offer superior flexibility and dimensional stability, making them ideal for use in flexible printed circuits, insulation tapes, and various display components. Continuous progress in electronics manufacturing, driven by miniaturization trends, flexible and wearable devices, and 5G integration, is accelerating demand for these films. Manufacturers are also developing next-generation polyimide films to meet the needs of flexible hybrid electronics, which require high reliability and performance. As industries shift toward lightweight, high-performance, and energy-efficient materials, the demand for polyimide films continues to expand across consumer electronics, communication equipment, and advanced circuitry applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 6.3% |

The standard aromatic polyimides segment generated USD 1.1 billion in 2024. Their dominance stems from extensive usage across various electronic applications such as flexible circuits, wire insulation, and display substrates. The reliability and cost-effectiveness of these materials make them the preferred choice in mass production. Meanwhile, thermally conductive polyimides are witnessing growing demand due to their ability to efficiently dissipate heat in high-power electronics, electric vehicle components, and compact semiconductor devices. Electrically conductive and corona-resistant polyimides are gaining traction in specialized applications that require enhanced voltage resistance and electrical properties, particularly in automotive, industrial, and aerospace electronics.

The flexible printed circuits (FPC/FCCL) segment was valued at USD 1 billion in 2024. This segment continues to expand with the increasing adoption of compact and high-density electronic components. The unique attributes of polyimide films, such as flexibility, heat endurance, and electrical insulation, make them essential in advanced circuit designs and modern electronic assemblies. Other key applications, including wire and cable insulation and motor and magnet wire insulation, also show strong potential, driven by the transition toward high-temperature materials in electric vehicles, automation technologies, and industrial systems.

U.S. Polyimide Films for Electronics Market was valued at USD 401.8 million in 2024. In North America, demand continues to grow due to advances in flexible electronics, aerospace systems, semiconductors, and automotive technologies. The U.S. market benefits from innovation in high-performance, low-dielectric, and colorless polyimide films. Strong R&D investment, the presence of major electronics manufacturers, and the increasing shift toward sustainable material production further enhance the region's position as a hub for polyimide film development and application.

Key players in the Global Polyimide Films for Electronics Market include Apical Film Solutions, Arakawa Chemical Industries Ltd., CAPLINQ Corporation, CS Hyde Company, DuPont, Dunmore Corporation, Hony Engineering Plastics Limited, Kaneka Corporation, Mitsui Chemicals Inc., NAGASE & Co. Ltd., Polyonics Inc., Qnity Electronics, Rogers Corporation, Saint-Gobain Performance Plastics, Sheldahl Flexible Technologies Inc., SKC Kolon PI Inc., Taimide Tech Inc., UBE Industries Ltd., Wuhan China Star Optoelectronics, Yousan Technology Co. Ltd., and 3M Company. Leading companies in the Polyimide Films for Electronics Market are emphasizing innovation, product differentiation, and sustainability to strengthen their market foothold. Many firms are heavily investing in research and development to produce high-performance polyimide films with enhanced electrical, thermal, and mechanical properties. Companies are also expanding production capacity and forming partnerships with electronic component manufacturers to develop customized film solutions. A key strategic focus is on eco-friendly and recyclable materials, aligning with global sustainability goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Application

- 2.2.3 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for flexible and wearable electronics

- 3.2.1.2 Expansion of 5G and high-frequency electronics

- 3.2.1.3 Technological advancements in material science

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing and processing complexity

- 3.2.2.2 Challenges in recyclability and sustainability

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of electric vehicles (EVs) and advanced automotive electronics

- 3.2.3.2 Emergence of advanced display technologies

- 3.2.3.3 Integration into emerging semiconductor packaging technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Million Meters)

- 5.1 Key trends

- 5.2 Standard aromatic polyimides

- 5.2.1 PMDA/ODA-based systems

- 5.3 Thermally conductive polyimides

- 5.3.1 Enhanced thermal conductivity variants

- 5.4 Electrically conductive & resistive films

- 5.4.1 Controlled surface resistivity

- 5.4.2 Anti-static & EMI shielding

- 5.5 Corona-resistant polyimides

- 5.5.1 High-voltage ac

- 5.5.2 Power electronics

- 5.6 Fluorinated polyimides

- 5.6.1 Low dielectric constant

- 5.6.2 5G & high-frequency communication systems

- 5.7 Composite & reinforced polyimides

- 5.7.1 Nanoparticle-enhanced variants

- 5.7.2 Mechanical property enhancement

- 5.8 Coated & metallized variants

- 5.8.1 FEP-coated films

- 5.8.2 Aluminum & ITO metallized films

- 5.8.3 Specialty coatings & surface treatments

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Million Meters)

- 6.1 Flexible printed circuits (FPC / FCCL)

- 6.2 Wire & cable insulation

- 6.2.1 Temperature electrical insulation

- 6.2.2 Aerospace & defense

- 6.2.3 Industrial motor

- 6.3 Electric vehicle battery systems

- 6.3.1 Battery pack insulation & thermal management

- 6.4 Display & touch panel substrates

- 6.4.1 OLED & flexible display

- 6.4.2 Touch sensor panel

- 6.5 Motor & magnet wire insulation

- 6.5.1 High-temperature motor

- 6.5.2 Industrial & automotive motor

- 6.6 Aerospace & space

- 6.6.1 Multilayer insulation systems

- 6.6.2 Satellite & spacecraft electronics

- 6.6.3 Thermal control & protection systems

- 6.7 Semiconductor packaging

- 6.7.1 Die attach & encapsulation

- 6.7.2 Advanced packaging technologies

- 6.7.3 Moisture sensitivity & reliability

Chapter 7 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Million Meters)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Apical Film Solutions

- 8.2 Arakawa Chemical Industries Ltd.

- 8.3 CAPLINQ Corporation

- 8.4 CS Hyde Company

- 8.5 DuPont

- 8.6 Dunmore Corporation

- 8.7 Hony Engineering Plastics Limited

- 8.8 Kaneka Corporation

- 8.9 Mitsui Chemicals Inc.

- 8.10 NAGASE & Co. Ltd.

- 8.11 Polyonics Inc.

- 8.12 Qnity Electronics

- 8.13 Rogers Corporation

- 8.14 Saint-Gobain Performance Plastics

- 8.15 Sheldahl Flexible Technologies Inc.

- 8.16 SKC Kolon PI Inc.

- 8.17 Taimide Tech Inc.

- 8.18 Toyobo Co. Ltd.

- 8.19 UBE Industries Ltd.

- 8.20 Wuhan China Star Optoelectronics

- 8.21 Yousan Technology Co. Ltd.

- 8.22 3M Company