PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876572

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876572

Automotive Ethernet PHY Chip Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

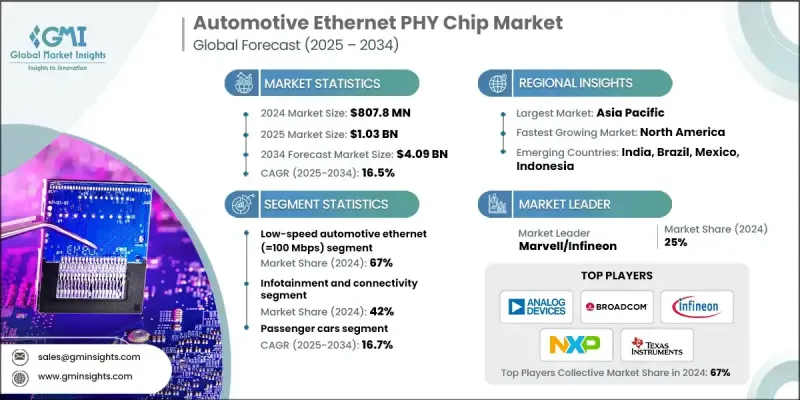

The Global Automotive Ethernet PHY Chip Market was valued at USD 807.8 million in 2024 and is estimated to grow at a CAGR of 16.5% to reach USD 4.09 billion by 2034.

Market growth is driven by the rapid evolution of in-vehicle electronic architectures that demand faster and more reliable data transmission. These PHY chips enable dependable communication over single, unshielded twisted pair cables across intricate automotive networks. Built to endure rigorous automotive conditions such as extreme temperatures, vibration, and electromagnetic interference, these chips are designed to meet stringent standards like AEC-Q100 Grade 1 and IEC 61508 for functional safety and long-term reliability. As vehicle networks increasingly adopt standardized IEEE Ethernet protocols, such as IEEE 802.3bw and IEEE 802.3bp, automakers are achieving greater interoperability and consistency across platforms. With advanced driver-assistance and autonomous driving technologies expanding, the need for high-speed, low-latency connectivity continues to grow. PHY chips support seamless data flow between sensors, radar, cameras, and infotainment systems, contributing to enhanced safety and connected mobility experiences across modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $807.8 Million |

| Forecast Value | $4.09 Billion |

| CAGR | 16.5% |

In 2024, the low-speed automotive Ethernet (up to 100 Mbps) segment held a 67% share. This segment remains the market leader due to its extensive installed base and compatibility with widely adopted Ethernet standards. Offering efficient full-duplex 100 Mbps data transfer over a single twisted pair cable, these PHY chips are widely utilized for gateway connections, infotainment systems, and basic networking applications within vehicles.

The passenger car segment is anticipated to grow at a CAGR of 16.7% from 2025 to 2034. Passenger cars, including sedans, hatchbacks, SUVs, and luxury models, continue to drive the highest demand for Ethernet PHY chips. Their dominance stems from the growing integration of electronic systems, increasing consumer interest in connectivity features, and early adoption of ADAS technologies compared with commercial vehicles.

China Automotive Ethernet PHY Chip Market generated USD 246.6 million in 2024. As the leading global producer of automobiles, China manufactured over 26.1 million passenger vehicles and 4 million commercial vehicles in 2023. This production scale has created a favorable environment for implementing Ethernet-based connectivity systems. Government initiatives promoting intelligent and connected vehicles have accelerated the use of PHY chip solutions across domestic vehicle models. Regulatory encouragement for autonomous driving, telematics, and digital cockpit technologies has further motivated local automakers to integrate advanced networking architectures into new platforms.

Leading companies in the Automotive Ethernet PHY Chip Market include Analog Devices, Broadcom, Cadence Design Systems, Intel, Marvell / Infineon, Microchip Technology, MaxLinear, NXP Semiconductors, Qualcomm Technologies, and Texas Instruments. Major players in the Automotive Ethernet PHY Chip Market are focusing on several strategic initiatives to strengthen their competitive position. Many companies are investing heavily in R&D to develop high-speed, energy-efficient, and compact PHY solutions that support evolving vehicle architectures. Strategic collaborations with automotive OEMs and Tier 1 suppliers are being pursued to accelerate product integration and testing. Firms are also expanding production capabilities and securing long-term supply chains to meet the growing demand for connected vehicles.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of EVs and ADAS

- 3.2.1.2 Shift to software-defined vehicles (SDV)

- 3.2.1.3 Rising vehicle production in emerging markets

- 3.2.1.4 Demand for low-latency, secure data transmission

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development costs for automotive-grade chips

- 3.2.2.2 Cybersecurity vulnerabilities in connected systems

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in autonomous driving and V2X ecosystems

- 3.2.3.2 Expansion of EV battery management and telematics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability & environmental aspects

- 3.11.1 Carbon Footprint Assessment

- 3.11.2 Circular Economy Integration

- 3.11.3 E-Waste Management Requirements

- 3.11.4 Green Manufacturing Initiatives

- 3.12 Use cases and applications

- 3.13 Best-case scenario

- 3.14 Total cost of ownership analysis

- 3.15 Automotive qualification processes & timelines

- 3.16 Supply chain resilience & risk management

- 3.17 Manufacturing process analysis & yield optimization

- 3.18 Quality & reliability metrics

- 3.19 Thermal management solutions & power Consumption Analysis

- 3.20 Interoperability Testing & Certification Requirements

- 3.21 Obsolescence Management & Long-Term Support Strategies

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, units)

- 5.1 Key trends

- 5.2 Low-Speed Automotive Ethernet (=100 Mbps)

- 5.2.1 10BASE-T1S

- 5.2.2 100BASE-T1

- 5.3 Gigabit Automotive Ethernet (1000BASE-T1)

- 5.4 Multi-Gigabit Automotive Ethernet (>1 Gbps)

- 5.4.1 2.5/5/10GBASE-T1

- 5.4.2 Future Standards (25G+)

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger Cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial Vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 ADAS and Autonomous Driving

- 7.2.1 Radar Systems

- 7.2.2 LiDAR Sensors

- 7.2.3 Cameras

- 7.2.4 Sensor Fusion

- 7.2.5 Domain Controllers

- 7.3 Infotainment and Connectivity

- 7.3.1 Display Systems

- 7.3.2 Audio Systems

- 7.3.3 Telematics

- 7.3.4 Over-the-Air Updates

- 7.3.5 Connectivity Gateways

- 7.4 Powertrain and Vehicle Dynamics

- 7.4.1 Engine Control

- 7.4.2 Transmission Control

- 7.4.3 Battery Management

- 7.4.4 Chassis Control

- 7.4.5 Thermal Management

- 7.5 Body Electronics and Comfort

- 7.5.1 Door Modules

- 7.5.2 Lighting Systems

- 7.5.3 Climate Control

- 7.5.4 Seat Control

- 7.5.5 Access Control

- 7.6 Gateway and Backbone

- 7.6.1 Central Gateways

- 7.6.2 Zone Controllers

- 7.6.3 Ethernet Switches

- 7.6.4 Diagnostic Systems

- 7.6.5 Security Gateways

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Nordics

- 8.3.7 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Players

- 9.1.1 Analog Devices

- 9.1.2 Broadcom

- 9.1.3 Marvell / Infineon

- 9.1.4 Intel

- 9.1.5 Marvell Technology

- 9.1.6 NXP Semiconductors

- 9.1.7 Qualcomm Technologies

- 9.1.8 Texas Instruments

- 9.2 Regional Players

- 9.2.1 Cadence Design Systems (PHY IP)

- 9.2.2 MaxLinear

- 9.2.3 MediaTek

- 9.2.4 Onsemi

- 9.2.5 Realtek Semiconductor

- 9.2.6 Renesas Electronics

- 9.2.7 Rohm Semiconductor

- 9.2.8 STMicroelectronics

- 9.3 Emerging Players/Disruptors

- 9.3.1 Alphawave IP

- 9.3.2 Aquantia

- 9.3.3 Canova Tech

- 9.3.4 Ethernovia

- 9.3.5 Kandou Bus

- 9.3.6 Valens Semiconductor