PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876644

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876644

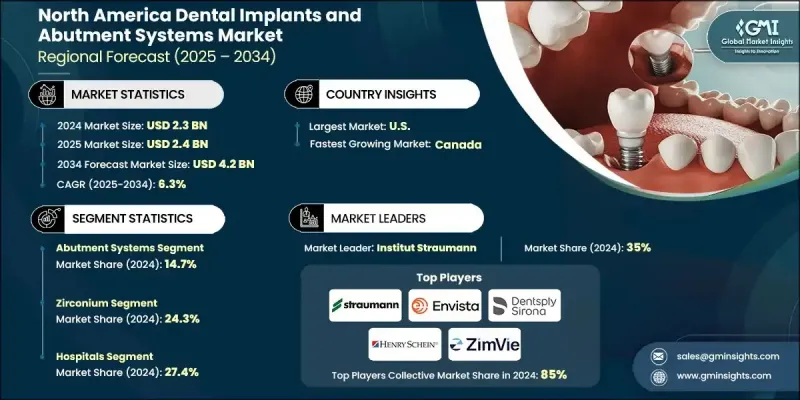

North America Dental Implants and Abutment Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

North America Dental Implants and Abutment Systems Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 4.2 billion by 2034.

Market expansion is influenced by widespread dental insurance coverage, an increasing burden of oral health issues, the rising appeal of cosmetic dentistry, and steady improvements in implant design and materials. Growing interest in procedures that enhance smile aesthetics continues to support demand, as more individuals seek corrective and restorative options that contribute to overall facial appearance. Dental implants and abutment systems serve as core components of restorative dentistry, functioning as replacements for missing teeth and helping reestablish oral performance and visual harmony. Implants, commonly crafted from titanium or zirconia, act as artificial roots placed within the jaw to secure crowns, dentures, or bridges. Abutments act as connectors that attach these restorations to the implant structure. Together, these systems offer durable and natural-looking outcomes for both functional rehabilitation and aesthetic enhancement, making them a preferred option for patients requiring long-term solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $4.2 Billion |

| CAGR | 6.3% |

The abutment systems segment was valued at USD 338 million in 2024 and held a 14.7% share. These systems form a vital interface in implant procedures by connecting the implant fixture to the final prosthetic restoration. They help preserve alignment, ensure stability, and maintain the overall visual quality of the dental prosthesis. Options vary by material, with titanium, zirconia, and hybrid designs selected according to clinical indications and cosmetic goals.

The zirconium segment accounted for a 24.3% share in 2024. Zirconium, most often used as zirconia, offers a ceramic, metal-free choice known for its biocompatibility and natural translucency. Its strength, thermal resistance, and ability to withstand significant force make it well-suited for patients sensitive to metal components or those requiring highly aesthetic restorations. These properties support its growing use in both implants and abutment systems, particularly in visible areas of the mouth.

U.S. Dental Implants and Abutment Systems Market generated USD 2.1 billion in 2024 and is projected to reach USD 3.8 billion by 2034. Rising oral health challenges and strong availability of trained dental specialists continue to shape demand. The country benefits from a large pool of implantology experts and continuous advancements in dental technology, along with enhanced training programs that strengthen the adoption of advanced restorative solutions. These factors contribute to ongoing growth and elevated demand for implants across various clinical settings.

Key players participating in the North America Dental Implants and Abutment Systems Market include A.B. Dental Devices, Bicon, Dentium USA, Henry Schein, Envista Holdings Corporation, Keystone Dental Group, BioHorizons, Adin Dental Implant Systems, Institut Straumann, ZimVie, Cortex, BioThread Dental Implant Systems, Osstem Implant, Dentsply Sirona, National Dentex Labs, Dynamic Abutment Solutions, and Glidewell. Companies active in the North America Dental Implants and Abutment Systems Market are emphasizing several strategies to reinforce their competitive presence. Many are investing in next-generation materials such as advanced ceramics and hybrid alloys to boost durability, biocompatibility, and aesthetics. Firms are expanding their digital dentistry capabilities by integrating CAD/CAM workflows, 3D imaging, and guided surgery platforms to improve treatment accuracy and clinician efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Country trends

- 2.2.2 Product trends

- 2.2.3 Material trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Robust dental insurance adoption rates

- 3.2.1.2 Growing prevalence of dental disorders

- 3.2.1.3 Rising demand for cosmetic dentistry

- 3.2.1.4 Advancements in implant technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory compliance challenges

- 3.2.2.2 High cost of dental implant treatment

- 3.2.3 Market opportunities

- 3.2.3.1 Shift towards minimally invasive procedures

- 3.2.3.2 Expansion of dental tourism

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dental implants

- 5.2.1 Tapered implants

- 5.2.2 Parallel-walled implants

- 5.3 Abutment systems

- 5.3.1 Stock abutments

- 5.3.2 Custom abutments

- 5.3.3 Abutments fixation screws

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Titanium

- 6.3 Zirconium

- 6.4 Other materials

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Dental Clinics

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Country, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 U.S.

- 8.3 Canada

Chapter 9 Company Profiles

- 9.1 A.B. Dental Devices

- 9.2 Adin Dental Implant Systems

- 9.3 Bicon

- 9.4 BioHorizons

- 9.5 BioThread Dental Implant Systems

- 9.6 Cortex

- 9.7 Dentium USA

- 9.8 Dentsply Sirona

- 9.9 Dynamic Abutment Solutions

- 9.10 Envista Holdings Corporation

- 9.11 Glidewell

- 9.12 Henry Schein

- 9.13 Institut Straumann

- 9.14 Keystone Dental Group

- 9.15 National Dentex Labs

- 9.16 Osstem Implant

- 9.17 ZimVie