PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885821

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885821

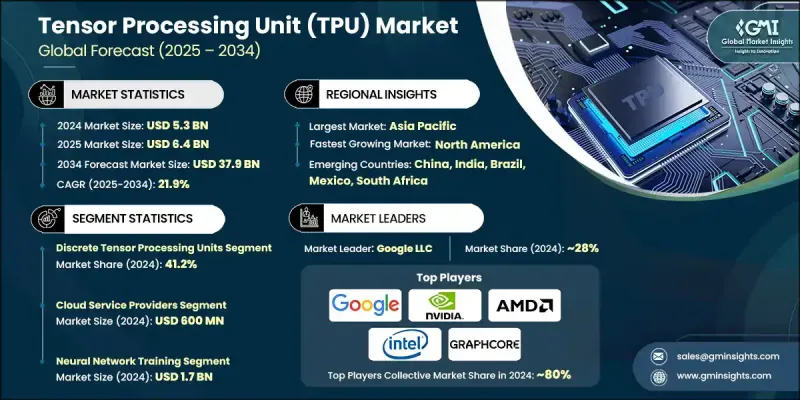

Tensor Processing Unit (TPU) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global Tensor Processing Unit (TPU) Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 21.9% to reach USD 37.9 billion by 2034.

The growth is fueled by the widespread adoption of artificial intelligence (AI) and machine learning (ML) across sectors such as healthcare, finance, automotive, and robotics. TPUs provide high-speed processing and energy-efficient performance, making them highly suited for deep learning applications. The rapid expansion of cloud computing infrastructure and the rising demand for real-time analytics are further accelerating TPU adoption. Industries increasingly require scalable, high-performance AI solutions, and TPUs are becoming integral to modern data centers and edge computing frameworks. Optimized for deep learning workloads, TPUs deliver faster training and inference times, essential for real-time decision-making and intelligent automation. Leading cloud service providers are embedding TPUs into their platforms, enabling enterprises to leverage AI efficiently. As businesses transition to cloud-based systems, high-performance and energy-efficient processors like TPUs are critical for reducing operational costs and accelerating data processing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $37.9 Billion |

| CAGR | 21.9% |

The discrete tensor processing units segment accounted for a 41.2% share in 2024. Discrete TPUs dominate due to their exceptional performance and flexibility in managing complex AI tasks. These standalone units are engineered for deep learning workloads, offering high computational throughput and scalability for enterprise and data center applications. Their compatibility with diverse hardware setups without relying on CPUs or GPUs enhances their suitability for large-scale AI training and inference, driving widespread adoption across cloud and high-performance computing environments.

The cloud service providers segment generated USD 600 million in 2024. These providers hold a dominant position as they offer scalable, high-performance AI infrastructure for businesses and developers. By integrating TPUs into cloud platforms, they provide cost-effective access to advanced machine learning capabilities without requiring significant upfront investment. With robust global data centers and support for multiple AI frameworks, cloud service providers are accelerating AI adoption across industries. Continuous innovation in TPU-based cloud services strengthens their leadership in the market.

North America Tensor Processing Unit (TPU) Market held a 40.2% share in 2024. Growth in this region is driven by increasing demand for high-performance computing to support AI and machine learning applications. The expansion of cloud-based services, data centers, and advancements in deep learning technologies are major growth factors. Investments by leading tech companies in TPU infrastructure are boosting AI workloads. Furthermore, the growing need for energy-efficient processing and real-time data handling in sectors such as healthcare, finance, and automotive is enhancing market expansion in North America.

Key players in the Global Tensor Processing Unit (TPU) Market include SambaNova Systems, Inc., Arm Holdings plc, Graphcore Ltd., Huawei Technologies Co., Ltd., Tenstorrent Inc., Fujitsu Limited, Amazon Web Services, Inc., Intel Corporation, Cambricon Technologies Corporation Limited, Microsoft Corporation, Qualcomm Technologies, Inc., Baidu, Inc., Google LLC, Advanced Micro Devices, Inc. (AMD), IBM Corporation, Alibaba Group Holding Limited, Cadence Design Systems, Inc., Hewlett Packard Enterprise Company, Synopsys, Inc., and NVIDIA Corporation. Companies in the Global Tensor Processing Unit (TPU) Market are leveraging multiple strategies to strengthen their foothold. They are heavily investing in research and development to enhance TPU performance and energy efficiency. Strategic partnerships, mergers, and acquisitions expand their market reach and enable integration with cloud and enterprise platforms. Companies are also focusing on broadening their product portfolios to meet diverse AI and machine learning requirements. Prioritizing sustainability and energy-efficient solutions improves competitiveness.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Trends

- 2.2.2 End use Industry Trends

- 2.2.3 Application Trends

- 2.2.4 Regional Trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for artificial intelligence and machine learning applications

- 3.2.1.2 Growing adoption of cloud computing services

- 3.2.1.3 Rising investments in deep learning technologies

- 3.2.1.4 Advancements in semiconductor technology

- 3.2.1.5 Need for high computational power for handling large-scale data processing tasks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment cost for TPU hardware

- 3.2.2.2 Limited availability of skilled professionals in TPU programming

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of TPU market in emerging economies

- 3.2.3.2 Development of customized TPU solutions for specific industries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Bn)

- 5.1 Key trends

- 5.2 Discrete Tensor Processing Units

- 5.3 Wafer-Scale AI Processors

- 5.4 Intelligence Processing Units

- 5.5 Integrated Neural Processing Units

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 ($ Bn)

- 6.1 Key trends

- 6.2 Government & Defense

- 6.3 Research Institutions

- 6.4 Cloud Service Providers

- 6.5 Enterprise Technology

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Bn)

- 7.1 Key trends

- 7.2 Neural Network Training

- 7.3 AI Inference Processing

- 7.4 Scientific Computing

- 7.5 Edge AI

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Google LLC (USA)

- 9.2 NVIDIA Corporation (USA)

- 9.3 Advanced Micro Devices, Inc. (AMD) (USA)

- 9.4 Intel Corporation (USA)

- 9.5 Microsoft Corporation (USA)

- 9.6 Amazon Web Services, Inc. (USA)

- 9.7 Huawei Technologies Co., Ltd. (China)

- 9.8 Alibaba Group Holding Limited (China)

- 9.9 Baidu, Inc. (China)

- 9.10 Graphcore Ltd. (UK)

- 9.11 SambaNova Systems, Inc. (USA)

- 9.12 Tenstorrent Inc. (Canada)

- 9.13 Cambricon Technologies Corporation Limited (China)

- 9.14 Qualcomm Technologies, Inc. (USA)

- 9.15 IBM Corporation (USA)

- 9.16 Arm Holdings plc (UK)

- 9.17 Cadence Design Systems, Inc. (USA)

- 9.18 Synopsys, Inc. (USA)

- 9.19 Fujitsu Limited (Japan)

- 9.20 Hewlett Packard Enterprise Company (USA)