PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982333

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982333

Reciprocating Plunger Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

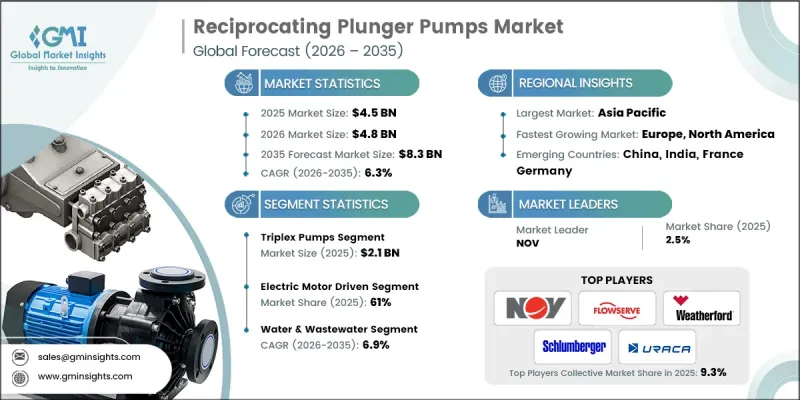

The Global Reciprocating Plunger Pumps Market was valued at USD 4.5 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 8.3 billion by 2035.

Growth in the reciprocating plunger pumps industry is being driven by increasing upstream oil and gas activities, rising demand for hydraulic fracturing operations, expanding industrialization, and greater use of high-pressure water jetting systems. Renewed investment in energy exploration, particularly in unconventional resource development, is accelerating the need for robust high-pressure pumping solutions. Reciprocating plunger pumps are widely utilized in applications that require reliable fluid transfer under extreme pressure conditions. As global energy consumption continues to climb, the demand for efficient pumping systems across extraction, refining, and transportation processes is strengthening. At the same time, rapid technological advancements in ultra-high-pressure plunger pump systems are transforming industrial operations. These advanced systems deliver superior pressure control, operational durability, and dependable performance across demanding environments. Their ability to maintain precision and stability under high loads positions reciprocating plunger pumps as essential components in modern industrial and energy infrastructure worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.5 Billion |

| Forecast Value | $8.3 Billion |

| CAGR | 6.3% |

The triplex pumps segment generated USD 2.1 billion in 2025 and is expected to grow at a CAGR of 6.2% through 2035. Their dominance is attributed to a balanced combination of strong pressure output, steady flow performance, and simplified mechanical configuration. The multi-plunger arrangement enables phased operation that minimizes pulsation and enhances operational consistency. Reduced vibration and smoother discharge flow contribute to improved system stability and lower maintenance requirements, making triplex pumps highly suitable for intensive industrial applications.

The electric motor-driven segment accounted for 61% share in 2025 and is anticipated to grow at a CAGR of 6.7% from 2026 to 2035. Electric motor-powered reciprocating plunger pumps provide precise speed modulation, instant torque response, and smoother operation compared to conventional engine-driven systems. These features allow operators to achieve accurate flow management, consistent pressure delivery, and reduced pulsation. The segment's growth is supported by increasing demand for energy-efficient systems capable of continuous-duty performance in high-pressure industrial processes.

United States Reciprocating Plunger Pumps Market held 83% share, generating USD 1.2 billion in 2025. Market expansion in the country is driven by sustained demand from the oil and gas sector, growing emphasis on water and wastewater management, and ongoing technological innovation. Advancements in pump engineering are improving durability, operational efficiency, and automation capabilities. Infrastructure modernization and industrial digitalization initiatives are further supporting equipment adoption. Additionally, the country's extensive mining activities contribute to demand for high-performance pumping systems capable of handling rigorous extraction and processing requirements.

Key companies operating in the Global Reciprocating Plunger Pumps Market include Flowserve Corporation, National Oilwell Varco (NOV), Schlumberger, Weatherford, Cat Pumps, URACA GmbH & Co. KG, KAMAT GmbH & Co. KG, MAXIMATOR GmbH, Ruhrpumpen, Peroni Pompe, Mouvex, UDOR, Bakker & Co., Dencil Pumps, and Nanjing Yalong Petrochemical Equipment Technology. Companies in the reciprocating plunger pumps market are strengthening their competitive position through continuous product innovation and strategic partnerships. Leading manufacturers are investing in research and development to enhance pressure capabilities, improve material durability, and increase energy efficiency. Integration of digital monitoring systems and predictive maintenance technologies is enabling smarter pump performance and reduced downtime. Firms are expanding their global distribution networks and reinforcing after-sales service capabilities to improve customer retention. Customization of pump configurations for industry-specific requirements is also becoming a key differentiator.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By Pump Configuration

- 2.2.3 By Pressure Range

- 2.2.4 By Flow Rate Capacity

- 2.2.5 By Drive Type

- 2.2.6 By Application

- 2.2.7 By Distribution Channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By pump configuration

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Pump Configuration, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Triplex pumps

- 5.3 Quintuplex pumps

- 5.4 Septuplex pumps

- 5.5 Other configurations

Chapter 6 Market Estimates & Forecast, By Pressure Range, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Low pressure (<500 bar)

- 6.3 Medium pressure (500-800 bar)

- 6.4 High pressure (>800 bar)

Chapter 7 Market Estimates & Forecast, By Flow Rate Capacity, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Low flow (<100 gpm / <380 lpm)

- 7.3 Medium flow (100-500 gpm / 380-1,900 lpm)

- 7.4 High flow (>500 gpm / >1,900 lpm)

Chapter 8 Market Estimates & Forecast, By Drive Type, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Electric motor driven

- 8.3 Diesel engine driven

- 8.4 Gas engine driven

- 8.5 Hydraulic driven

- 8.6 Other drive systems

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Oil & gas

- 9.3 Chemical processing

- 9.4 Water & wastewater

- 9.5 Power generation

- 9.6 Mining & minerals

- 9.7 Industrial manufacturing

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Bakker & Co.

- 12.2 Cat Pumps

- 12.3 Dencil Pumps

- 12.4 Flowserve Corporation

- 12.5 KAMAT GmbH & Co. KG

- 12.6 MAXIMATOR GmbH

- 12.7 Mouvex

- 12.8 Nanjing Yalong Petrochemical Equipment Technology

- 12.9 National Oilwell Varco (NOV)

- 12.10 Peroni Pompe

- 12.11 Ruhrpumpen

- 12.12 Schlumberger

- 12.13 UDOR

- 12.14 URACA GmbH & Co. KG

- 12.15 Weatherford