PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1892775

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1892775

Urology Supplements Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

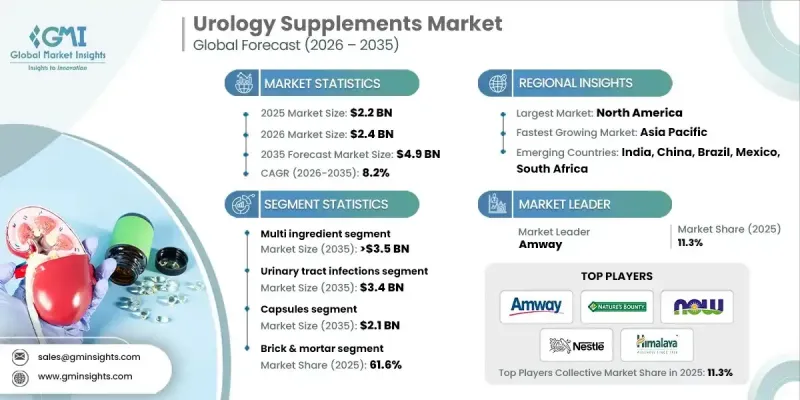

The Global Urology Supplements Market was valued at USD 2.2 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 4.9 billion by 2035.

Market growth is supported by the rising burden of urinary health disorders, growing concern around prostate wellness, and increasing consumer focus on proactive self-care routines. Wider access to digital retail platforms and a strong preference for naturally derived formulations further reinforce demand. Consumers are increasingly seeking science-backed, non-pharmaceutical solutions that support urinary tract function, prostate health, kidney performance, and overall urological balance. Rising infection rates, a growing aging population, and the shift toward preventive and self-managed healthcare continue to expand the addressable consumer base. Leading industry participants compete through advanced formulation expertise, validated botanical science, and diversified distribution strategies spanning physical retail, online platforms, and practitioner-focused channels. Continuous innovation and growing consumer education initiatives are strengthening confidence in urology-focused dietary supplementation and supporting sustained market development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.2 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 8.2% |

Key manufacturers emphasize high-grade ingredient sourcing, sustained research investment, and transparent consumer communication to reinforce credibility and product effectiveness. Strategic advancements centered on optimized nutrient combinations, clinically aligned formulations, and evidence-supported performance benchmarks are raising quality standards across the market and improving long-term urinary wellness outcomes.

The multi-ingredient formulations segment accounted for a 70.4% share in 2025. This leadership position reflects increasing consumer preference for all-in-one products designed to address multiple urological health needs in a single regimen. These formulations integrate diverse functional components to deliver enhanced convenience, broader health coverage, and improved perceived effectiveness, which continues to support segment growth.

The urinary tract health segment held a 67.8% share in 2025 and is projected to reach USD 3.4 billion during 2026-2035, attributed to widespread prevalence across age groups and heightened awareness of preventive nutritional approaches that support long-term urinary function and reduce recurrence risks.

North America Urology Supplements Market held a 40.2% share in 2025. Strong consumer awareness, well-established healthcare infrastructure, and rising incidence of urological conditions have fueled demand for supportive supplementation. Ongoing advances in formulation technologies and increased availability of clinically positioned products continue to accelerate regional adoption.

Prominent companies operating in the Global Urology Supplements Market include NOW Foods, Himalaya Wellness, Nestle, Natrol, Amway, Better Being, dsm-firmenich, Theralogix, Puritan's Pride, Himalayan Organics, Nature's Bounty, Solgaray, Biotexlife, ZAHLER, and Szio+. Companies in the Global Urology Supplements Market adopt targeted strategies to strengthen their competitive positioning and expand market share. Product differentiation through clinically aligned formulations and premium ingredient sourcing remains a central focus. Manufacturers invest heavily in research to support efficacy claims and meet evolving regulatory expectations. Expansion across omnichannel distribution models enables brands to reach both direct consumers and healthcare-influenced buyers. Strategic acquisitions and partnerships support portfolio diversification and geographic reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 Formulation trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of urological disorders

- 3.2.1.2 Advancements in product formulations and delivery systems

- 3.2.1.3 Increasing emphasis on preventive healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Potential interactions and side effects

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding demand for personalized nutrition solutions

- 3.2.3.2 Rising penetration across emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.1.1 Advanced absorption and bioavailability technologies

- 3.5.1.2 Novel herbal and functional ingredients for urinary health

- 3.5.1.3 AI-assisted personalized dosing and supplement guidance

- 3.5.2 Emerging technologies

- 3.5.2.1 Machine learning for multi-ingredient formulation optimization

- 3.5.2.2 Integration with wearable and remote health monitoring devices

- 3.5.2.3 Smart encapsulation and controlled-release delivery systems

- 3.5.1 Current technological trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.9.1 Tailored nutrition solutions based on genetic and lifestyle data

- 3.9.2 Evidence-backed, clinically tested urology supplement combinations

- 3.9.3 Digital-first platforms combining AI recommendations with global e-commerce reach

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Multi ingredient

- 5.3 Single ingredient

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Urinary tract infections

- 6.3 Prostate health

- 6.4 Kidney health

- 6.5 Bladder health

Chapter 7 Market Estimates and Forecast, By Formulation, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Capsules

- 7.3 Softgels

- 7.4 Tablets

- 7.5 Powder

- 7.6 Other formulations

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Brick & mortar

- 8.3 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amway

- 10.2 Better Being

- 10.3 Biotexlife

- 10.4 dsm-firmenich

- 10.5 Himalaya Wellness

- 10.6 Himalayan Organics

- 10.7 Natrol

- 10.8 Nature's Bounty

- 10.9 Nestle

- 10.10 NOW Foods

- 10.11 Puritan's Pride

- 10.12 Solaray

- 10.13 Szio+

- 10.14 Theralogix

- 10.15 ZAHLER