PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1892898

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1892898

Analytical Instrumentation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

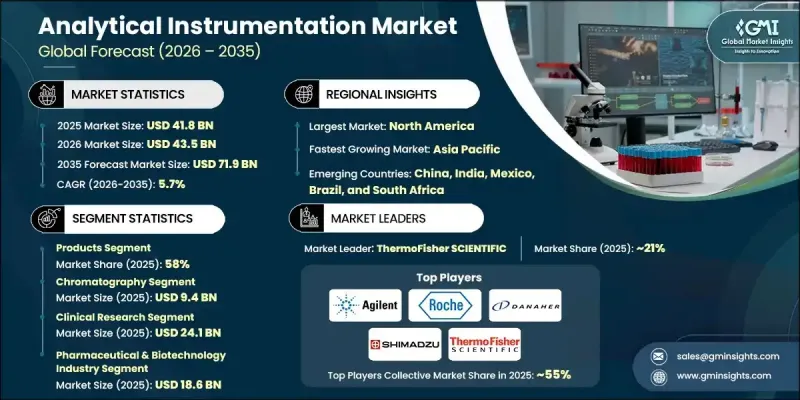

The Global Analytical Instrumentation Market was valued at USD 41.8 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 71.9 billion by 2035.

The growth is fueled by increased R&D investments in the pharmaceutical and biotech sectors, rising adoption of analytical systems for precision medicine, the growing prevalence of chronic and infectious diseases, and regulatory mandates driving compliance with validated analytical protocols. Analytical instrumentation enables laboratories to deliver highly accurate measurements, real-time monitoring, and advanced data analytics, supporting evidence-based clinical decision-making and optimized treatment strategies. The rising demand for high-throughput, sensitive testing in clinical, reference, and research laboratories is further accelerating the adoption of these systems, which are essential for impurity profiling, biologics characterization, batch release, and stability testing. These instruments allow scientists and clinicians to analyze chemical, physical, and molecular properties of samples with unmatched precision, making them critical across healthcare, pharmaceutical, and industrial applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $41.8 Billion |

| Forecast Value | $71.9 Billion |

| CAGR | 5.7% |

The products segment held 58% share in 2025, driven by strong demand for advanced instruments in pharmaceutical R&D, diagnostics, and industrial testing. This dominance is reinforced by continuous technological innovation and the growing need for precise, high-throughput analytical tools.

The chromatography segment generated USD 9.4 billion in 2025, due to its ability to separate, identify, and quantify complex chemical mixtures accurately. Laboratories heavily rely on chromatography for quality control, formulation development, stability testing, and impurity profiling, solidifying its central role in research-intensive workflows.

U.S. Analytical Instrumentation Market reached USD 14.6 billion in 2025 and is expected to grow at a CAGR of 5.8% through 2035. This leadership stems from a mature pharmaceutical, biotechnology, and clinical diagnostics ecosystem, advanced laboratory infrastructure, and stringent regulatory requirements. Agencies such as the FDA, USP, CDC, and CMS/CLIA enforce rigorous analytical validation for drug development, biologics manufacturing, and clinical diagnostics, driving sustained demand for high-precision instruments, including chromatography, spectroscopy, mass spectrometry, molecular analysis platforms, and particle characterization tools across research, quality control, and clinical laboratories.

Key players in the Global Analytical Instrumentation Market include Bruker, Waters, Eppendorf, Agilent, Illumina, Avantor, Revvity, Shimadzu, METTLER TOLEDO, Bio-Rad, Malvern Panalytical (Spectris), Roche, Sartorius, Hitachi, ThermoFisher Scientific, Metrohm AG, Zeiss, and Danaher. To strengthen their Analytical Instrumentation Market position, companies are focusing on product innovation, expanding instrument portfolios, and integrating advanced technologies such as AI, IoT, and automation into their analytical platforms. Strategic collaborations with pharmaceutical, biotech, and research institutions help accelerate the adoption of cutting-edge systems. Firms are investing in digital services, predictive maintenance, and cloud-enabled analytics to improve workflow efficiency and uptime. Global expansion into emerging markets, targeted marketing campaigns, and customized solutions for clinical, industrial, and research applications further reinforce brand presence and foster long-term client relationships.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product & services trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising R&D spending by the pharmaceutical industry and government research organizations

- 3.2.1.2 Technological advancements in analytical instruments

- 3.2.1.3 Increasing adoption of analytical instrumentation for precision medicine applications

- 3.2.1.4 Growing prevalence of chronic and infectious diseases requiring accurate testing

- 3.2.1.5 Regulatory compliance driving adoption of validated analytical systems

- 3.2.1.6 Expansion of molecular diagnostics and PCR-based platforms for early detection

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of instruments

- 3.2.2.2 Lack of skilled professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in point-of-care testing

- 3.2.3.2 Surge in drug discovery and development activities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Value chain analysis

- 3.5 Pipeline analysis

- 3.6 Pricing analysis, by region, 2025

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Volume analysis, 2022 - 2035

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 MEA

- 3.8 Future market trends

- 3.9 Regulatory landscape

- 3.10 Technology landscape

- 3.10.1 Current technologies

- 3.10.2 Emerging technologies

- 3.11 Gap analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 North America

- 4.3.2 Europe

- 4.3.3 Asia Pacific

- 4.3.4 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product & Services, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Products

- 5.2.1 Chromatography instruments

- 5.2.2 Spectroscopy instruments

- 5.2.3 Molecular analysis instruments

- 5.2.4 Particle counters and analyzers

- 5.2.5 Electrochemical analysis instruments

- 5.2.6 Other products

- 5.3 Services & consumables

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Chromatography

- 6.2.1 Liquid chromatography

- 6.2.2 Gas chromatography

- 6.2.3 Ion chromatography

- 6.3 Spectroscopy

- 6.4 Polymerase chain reaction

- 6.5 Particle analysis

- 6.6 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Clinical research

- 7.3 Clinical diagnostics

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical & biotechnology industry

- 8.3 Research and academic institutes

- 8.4 Diagnostic centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Poland

- 9.3.7 Sweden

- 9.3.8 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Thailand

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.5.5 Chile

- 9.5.6 Peru

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Israel

- 9.6.5 Turkey

- 9.6.6 Iran

Chapter 10 Company Profiles

- 10.1 Agilent

- 10.2 Avantor

- 10.3 BIO RAD

- 10.4 BRUKER

- 10.5 Danaher

- 10.6 Eppendorf

- 10.7 HITACHI

- 10.8 Illumina

- 10.9 Malvern Panalytical (Spectris)

- 10.10 METTLER TOLEDO

- 10.11 Metrohm AG

- 10.12 Revvity

- 10.13 Roche

- 10.14 SARTORIUS

- 10.15 SHIMADZU

- 10.16 ThermoFisher SCIENTIFIC

- 10.17 Waters

- 10.18 ZEISS