PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913285

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913285

Packaging Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

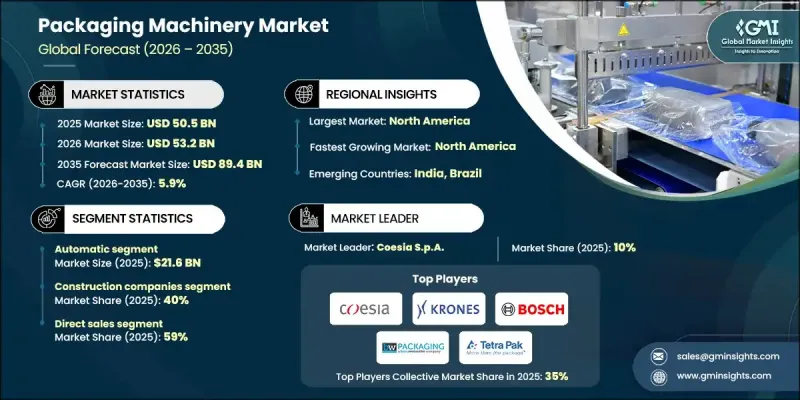

The Global Packaging Machinery Market is valued at USD 50.5 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 89.4 billion by 2035.

Packaging machinery now plays a critical role in supporting faster output, improved product integrity, regulatory adherence, and lower environmental impact. Manufacturers face increasing pressure to deliver consistent quality at scale while meeting sustainability targets and operational efficiency goals. Automated packaging solutions remain central to these efforts, as they deliver high precision, improved sanitation, and reliable compliance with global standards. As manufacturing volumes rise and supply chains become more complex, companies increasingly rely on advanced packaging systems to ensure secure sealing and efficient processing. The industry continues to transform through innovation that aligns productivity with environmental responsibility. Investments in automation, digitalization, and material optimization reinforce the importance of packaging machinery across multiple industrial workflows. The market's growth trajectory reflects rising demand for dependable, scalable, and future-ready packaging solutions that support modern manufacturing needs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $50.5 Billion |

| Forecast Value | $89.4 Billion |

| CAGR | 5.9% |

Packaging machinery producers are actively redesigning equipment to integrate intelligent functionality through digital controls and sensor-based monitoring, improving uptime and operational speed. Sustainability has become a foundational value rather than an optional feature, with machines engineered to handle eco-conscious materials while reducing waste generation. These advancements respond directly to rising demand for environmentally responsible production methods.

In 2025, the automatic systems segment generated USD 21.6 billion. Automation enhances consistency, limits human intervention, and significantly lowers error rates. These systems enable large-scale production while allowing flexible packaging formats, supporting faster turnaround times and improved operational reliability. The adoption of connected technologies further accelerates demand by enabling predictive servicing, real-time visibility, and data-driven efficiency improvements that lower long-term costs.

The direct sales segment accounted for a 59% share in 2025, reflecting a strong preference for manufacturer-to-client engagement. This approach supports tailored system configurations, faster implementation, and stronger service oversight, particularly for high-volume operations. Direct channels also enable greater pricing control and enhanced post-sale support.

United States Packaging Machinery Market held a 71% share in 2025, generating USD 12.6 billion. The region benefits from advanced infrastructure, widespread automation adoption, and strong investment in smart manufacturing. Expanding online retail activity and steady demand from consumer goods and beverage producers continue to drive high-speed system adoption.

Leading companies active in the Global Packaging Machinery Market include Tetra Pak International S.A., Krones AG, Coesia S.p.A., MULTIVAC Sepp Haggenmuller SE & Co. KG, Barry-Wehmiller, Ishida Co., Ltd., Yamato Scale Co., Ltd., Robert Bosch Packaging Technology, Ilapak International SA, Rovema GmbH, Fres-co System USA, Inc., ENGEL Holding GmbH, KraussMaffei Group GmbH, ARBURG GmbH + Co KG, Sumitomo Heavy Industries Ltd., and JSW Plastics Machinery Co., Ltd. Companies operating in the Global Packaging Machinery Market reinforce their competitive position through continuous innovation, automation expansion, and sustainability-driven design. Strategic investments in digital technologies improve machine intelligence, predictive maintenance, and system efficiency. Manufacturers focus on modular designs to enable customization while reducing deployment time. Global players strengthen distribution networks and after-sales services to enhance customer retention. Sustainability initiatives, including waste reduction and material compatibility, support compliance with environmental regulations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Automation

- 2.2.4 End-user industry

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for automation and efficiency

- 3.2.1.2 Growth of e-commerce and consumer packaged goods (CPG)

- 3.2.1.3 Technological advancements and smart packaging integration

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Complexity in maintenance and skilled workforce shortage

- 3.2.3 Opportunities

- 3.2.3.1 Sustainability and eco-friendly packaging solutions

- 3.2.3.2 Expansion in developing economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By Region

- 3.6.2 By Equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2022 - 2025 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Filling & dosing equipment

- 5.2.1 Volumetric fillers

- 5.2.2 Gravimetric fillers

- 5.2.3 Liquid fillers

- 5.2.4 Powder fillers

- 5.3 Bagging & flexible packaging equipment

- 5.3.1 Vertical form-fill-seal (vffs)

- 5.3.2 Horizontal form-fill-seal (hffs)

- 5.3.3 Pre-made bag filling & sealing

- 5.3.4 Pouch making & filling

- 5.3.5 Product wrapping equipment

- 5.4 Cartoning, case packing & multipacking equipment

- 5.4.1 Horizontal cartoners

- 5.4.2 Vertical cartoners

- 5.4.3 Wraparound case packers

- 5.4.4 Tray formers

- 5.4.5 Shrink bundlers and multipack wrappers

- 5.5 Labeling, coding & marking equipment

- 5.5.1 Pressure-sensitive labelers

- 5.5.2 Hot-melt and cold-glue labelers

- 5.5.3 Sleeve labelers

- 5.5.4 Inkjet and laser coders

- 5.5.5 Thermal transfer printers

- 5.6 Palletizing & end-of-line equipment

- 5.6.1 Robotic palletizers

- 5.6.2 Conventional palletizers

- 5.6.3 Pallet stretch wrappers

- 5.6.4 Pallet shrink wrappers

- 5.6.5 Strapping machines

- 5.6.6 Case sealers

- 5.7 Conveying, feeding & handling equipment

- 5.7.1 Belt and roller conveyors

- 5.7.2 Accumulation tables

- 5.7.3 Product feeders and sorters

- 5.7.4 Robotic pick-and-place

- 5.8 Inspection & quality control equipment

- 5.8.1 Checkweighers

- 5.8.2 Metal detectors and x-ray inspection

- 5.8.3 Vision inspection systems

- 5.8.4 Leak testers

- 5.9 Capping & closing equipment

- 5.9.1 Screw cappers

- 5.9.2 Snap cappers and crimpers

- 5.9.3 Seamers and induction sealers

- 5.10 Bulk bag & fibc handling equipment

- 5.10.1 Bulk bag fillers

- 5.10.2 Fibc dischargers

- 5.11 Other equipment types

- 5.11.1 Blister packaging machines

- 5.11.2 Bottle blowing and molding

- 5.11.3 Aseptic packaging systems

Chapter 6 Market Estimates and Forecast, By Automation, 2022 - 2025 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Fully automatic

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2025 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.2.1 Fresh & frozen foods

- 7.2.2 Dry foods & snacks

- 7.2.3 Beverages

- 7.2.4 Dairy

- 7.3 Pharmaceuticals & medical devices

- 7.3.1 Tablets and capsules

- 7.3.2 Injectables and biologics

- 7.3.3 Medical devices and diagnostics

- 7.3.4 Nutraceuticals

- 7.3.5 Personal care & cosmetics

- 7.3.6 Skincare and haircare

- 7.3.7 Cosmetics and color

- 7.3.8 Toiletries and hygiene products

- 7.4 Household, industrial & agricultural chemicals

- 7.4.1 Detergents and cleaners

- 7.4.2 Fertilizers and pesticides

- 7.4.3 Industrial chemicals

- 7.5 Pet food & animal nutrition

- 7.5.1 Dry pet food

- 7.5.2 Wet pet food

- 7.5.3 Treats and supplements

- 7.5.4 Animal feed

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2025 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2025 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ARBURG GmbH + Co KG

- 10.2 Barry-Wehmiller (BW Packaging)

- 10.3 Coesia S.p.A.

- 10.4 ENGEL Holding GmbH

- 10.5 Fres-co System USA, Inc.

- 10.6 Ilapak International SA

- 10.7 Ishida Co., Ltd.

- 10.8 KraussMaffei Group GmbH

- 10.9 Krones AG

- 10.10 MULTIVAC Sepp Haggenmuller SE & Co. KG

- 10.11 Robert Bosch Packaging Technology

- 10.12 Rovema GmbH

- 10.13 Sumitomo Heavy Industries, Ltd.

- 10.14 Tetra Pak International S.A.

- 10.15 Yamato Scale Co., Ltd