PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913309

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913309

Processed Fruits and Vegetables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

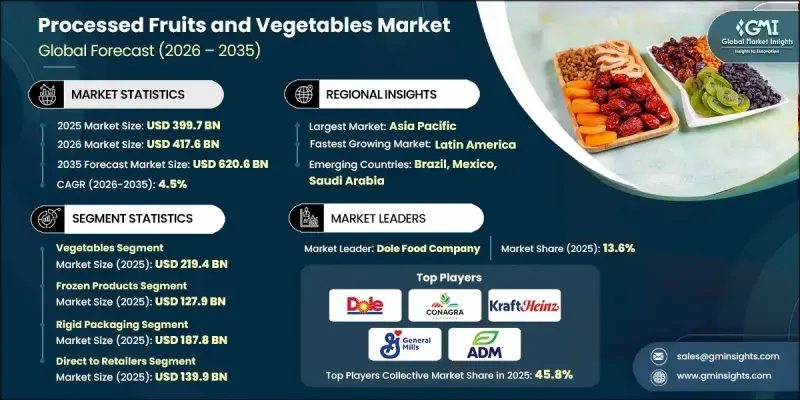

The Global Processed Fruits and Vegetables Market was valued at USD 399.7 billion in 2025 and is estimated to grow at a CAGR of 4.5% to reach USD 620.6 billion by 2035.

Growth is supported by changing consumption patterns that favor convenience and time efficiency in daily meals. Urbanization, longer working schedules, and evolving household structures continue to reduce time available for food preparation, strengthening demand for ready-to-use and ready-to-eat food options. Processed fruits and vegetables address these needs by offering extended shelf life, consistent quality, and ease of use across multiple consumption settings. At the same time, rising awareness of nutrition and balanced diets is supporting positive consumer perception of processed produce. Many consumers now view these products as practical alternatives to fresh options when nutritional value is preserved. Growing acceptance of minimally processed formats, frozen offerings, and plant-forward eating habits is widening the consumer base and reinforcing long-term market expansion across retail and foodservice channels.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $399.7 Billion |

| Forecast Value | $620.6 Billion |

| CAGR | 4.5% |

The vegetables category generated USD 219.4 billion in 2025. Vegetables represent the dominant product group within the processed fruits and vegetables market due to broad utilization across households, foodservice operations, and industrial food production. Their longer storage potential, lower natural sugar content compared to fruits, and adaptability across global cuisines contribute to strong and consistent demand.

The frozen formats segment accounted for USD 127.9 billion in 2025, holding a leading share within processing types. These products are favored for their ability to preserve nutritional content, texture, and taste while offering extended storage life, supporting both commercial and consumer use.

North America Processed Fruits and Vegetables Market held 23% share in 2025, supported by advanced processing capabilities, robust cold-chain infrastructure, and strong food safety standards. The United States leads regional production due to a large manufacturing base, high per-capita consumption of convenience foods, and well-developed retail and foodservice networks.

Key companies active in the Global Processed Fruits and Vegetables Market include Nestle S.A., Dole Food Company, The Kraft Heinz Company, General Mills, Inc., Del Monte Foods, Inc., Conagra Brands, Inc., B&G Foods, Inc., ADM, Grofresh Agrofoods Pvt Ltd, Vebzy Nature and ABC Fruits. Companies operating in the Global Processed Fruits and Vegetables Market strengthen their position through product innovation, supply chain efficiency, and geographic expansion. Leading players invest in processing technologies that maintain nutritional integrity while improving shelf stability. Portfolio diversification across formats and price points helps address varied consumer preferences. Firms also focus on sourcing optimization and long-term partnerships with growers to ensure consistent raw material supply. Expansion into emerging markets, along with enhanced distribution networks, supports volume growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Processing Form

- 2.2.4 Packaging Type

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for convenience foods

- 3.2.1.2 Growing health & wellness consciousness

- 3.2.1.3 Expansion of organized retail & e-commerce

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Dependency on Seasonal Raw Materials

- 3.2.2.2 Stringent Food Safety and Quality Regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into Plant-Based and Functional Products

- 3.2.3.2 Export potential to regions with limited local production

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product Type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fruits

- 5.2.1 Citrus fruits

- 5.2.2 Berries

- 5.2.3 Stone fruits

- 5.2.4 Tropical fruits

- 5.2.5 Other fruits

- 5.3 Vegetables

- 5.3.1 Leafy & cruciferous vegetables

- 5.3.2 Root & bulb vegetables

- 5.3.3 Other vegetables

Chapter 6 Market Estimates and Forecast, By Processing Form, 2022 - 2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Canned / jarred products

- 6.3 Frozen products

- 6.4 Dried & dehydrated

- 6.5 Fresh-cut / minimally processed

- 6.6 Juices & concentrates

- 6.7 Preserves, jams & jellies

- 6.8 Purees & sauces

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By Packaging Type, 2022 - 2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Rigid packaging

- 7.2.1 Metal cans

- 7.2.2 Glass jars

- 7.2.3 Rigid plastic containers

- 7.3 Flexible packaging

- 7.3.1 Stand-up pouches

- 7.3.2 Retort pouches

- 7.3.3 Bags, films & wraps

- 7.4 Bulk packaging

- 7.4.1 Drums & pails

- 7.4.2 Totes & IBC containers

- 7.4.3 Aseptic bulk containers

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Online platforms

- 8.3 Direct to retailers

- 8.4 Wholesalers

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Dole Food Company

- 10.2 Conagra Brands, Inc.

- 10.3 Del Monte Foods, Inc.

- 10.4 Nestle S.A.

- 10.5 The Kraft Heinz Company

- 10.6 General Mills, Inc.

- 10.7 B&G Foods, Inc.

- 10.8 ADM

- 10.9 ABC Fruits

- 10.10 Conagra

- 10.11 Vebzy Nature

- 10.12 Grofresh Agrofoods Pvt Ltd