PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913381

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913381

Industrial 3D Printer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

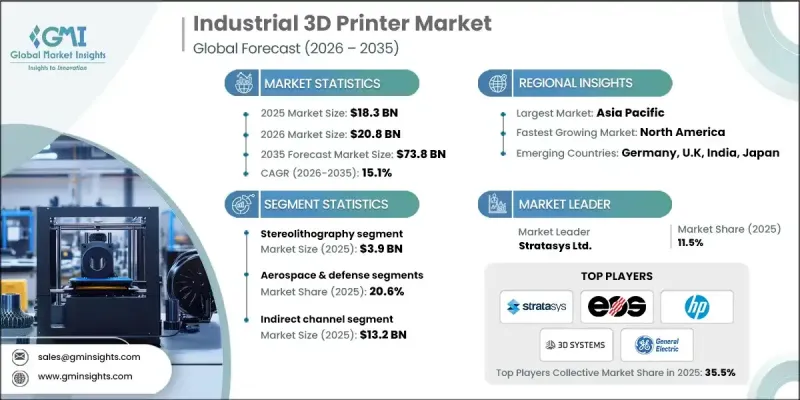

The Global Industrial 3D Printer Market was valued at USD 18.3 billion in 2025 and is estimated to grow at a CAGR of 15.1% to reach USD 73.8 billion by 2035.

Cost efficiency remains a key factor driving market growth, with manufacturers able to reduce tooling costs by up to 80-90%, translating into savings of over USD 100,000 per part in certain applications, even for limited production runs. The market benefits from 3D printing's ability to produce highly customized and geometrically complex components. In the healthcare sector, companies are delivering patient-specific implants, enhancing recovery outcomes. Material efficiency and sustainability also play a crucial role, as 3D printing reduces waste by 30-95% depending on the application. Technological innovations, including metal additive manufacturing and multi-material printing, are further broadening the market by enabling new industrial use cases. Government initiatives and funding programs are supporting research and adoption, particularly for applications requiring precision and advanced material capabilities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18.3 Billion |

| Forecast Value | $73.8 Billion |

| CAGR | 15.1% |

The stereolithography (SLA) generated USD 3.9 billion in 2025. SLA enables the production of highly intricate prototypes and functional parts with exceptional precision, making it ideal for industries that demand complex designs. Its industrial adoption is bolstered by government funding and initiatives, fostering innovation in specialized SLA resins and targeted applications.

The aerospace and defense sector held 20.6% share in 2025, driven by the need for lightweight, fuel-efficient, and geometrically sophisticated components. Additive manufacturing allows production of lattice structures and conformal cooling channels that are impossible to achieve with conventional techniques, cementing aerospace and defense as a leading adopter of industrial 3D printing.

United States Industrial 3D Printer Market held 78.1% share in 2025. The growth is supported by a strong manufacturing base and rapid adoption of advanced technologies. Leading companies such as Stratasys and 3D Systems have propelled the U.S. market by expanding their portfolios to meet the demands of high-precision sectors, including aerospace and healthcare, and collaborating with major manufacturers to scale 3D production lines.

Key players in the Global Industrial 3D Printer Market include HP, Markforged, Nano Dimension, Prodways, SLM Solutions, 3D Systems, Stratasys, EOS, General Electric, Formlabs, Ultimaker, Velo3D, and Materialise. Companies in the Global Industrial 3D Printer Market are strengthening their position through several strategic initiatives. They are heavily investing in R&D to enhance precision, material versatility, and production speed. Partnerships with OEMs and industry leaders enable large-scale adoption of 3D printing technologies. Firms focus on expanding regional distribution networks and service infrastructure to improve accessibility and customer support. They are also introducing software solutions for process optimization and workflow integration. Emphasis on sustainability, including reducing material waste and energy consumption, helps companies meet regulatory requirements and attract environmentally conscious clients.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 End use

- 2.2.4 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Wide use of rapid prototyping

- 3.2.1.2 Improvements in product development and supply chains

- 3.2.1.3 Government investments in 3D printing projects

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Material limitations and quality control

- 3.2.2.2 Ease of replicating designs with 3D printing technology

- 3.2.3 Opportunities

- 3.2.3.1 Expansion into healthcare and bioprinting

- 3.2.3.2 Sustainability and regulatory compliance solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By technology

- 3.6.2 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Gap analysis

- 3.9 Risk assessment and mitigation

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Selective laser sintering

- 5.3 Stereolithography

- 5.4 Fuse deposition modeling

- 5.5 Direct metal laser sintering

- 5.6 Inkjet printing

- 5.7 Polyjet printing

- 5.8 Electron beam melting

- 5.9 Laminated object manufacturing

- 5.10 Digital light processing

- 5.11 Laser metal deposition

- 5.12 Others

Chapter 6 Market Estimates & Forecast, By End-User, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automotive

- 6.3 Aerospace & defense

- 6.4 Healthcare

- 6.5 Consumer electronics

- 6.6 Food & culinary

- 6.7 Power & energy

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Direct

- 7.3 Indirect

Chapter 8 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 UK

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3D Systems

- 9.2 Desktop Metal

- 9.3 EOS

- 9.4 Formlabs

- 9.5 General Electric

- 9.6 HP

- 9.7 Markforged

- 9.8 Materialise

- 9.9 Nano Dimension

- 9.10 Prodways

- 9.11 Renishaw

- 9.12 SLM Solutions

- 9.13 Stratasys

- 9.14 Ultimaker

- 9.15 Velo3D