PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1928969

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1928969

Hydraulic Motors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

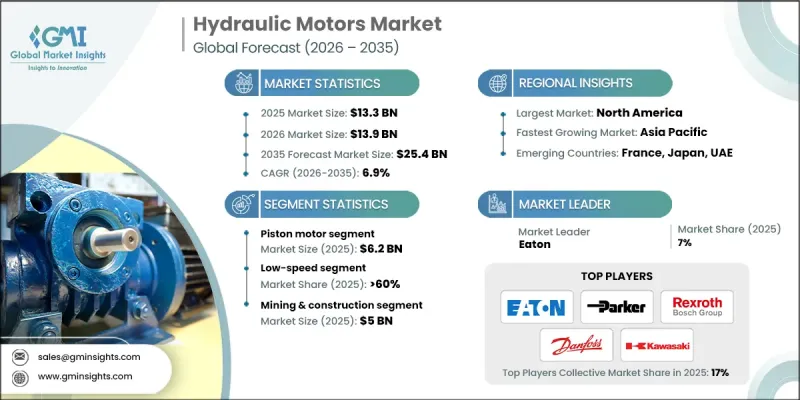

The Global Hydraulic Motors Market was valued at USD 13.3 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 25.4 billion by 2035.

The rising demand is fueled by the global growth of construction, agriculture, and mining sectors. Government investments in transportation infrastructure, housing, and industrial projects are driving the need for heavy machinery such as loaders, cranes, and excavators, all of which rely on hydraulic motors for high torque and reliable performance in demanding conditions. Mining operations continue to depend on hydraulic-powered equipment for drilling, mineral transport, crushing, and material handling, further boosting market demand. In agriculture, mechanization and the shift toward high-efficiency equipment are accelerating adoption, allowing companies to reduce manual labor, increase reliability, and enhance productivity. The growing trend of large-scale machinery in these industries is creating a strong growth opportunity for hydraulic motors, as they provide precise control, high power density, and durability for long-term operations across multiple sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.3 Billion |

| Forecast Value | $25.4 Billion |

| CAGR | 6.9% |

In 2025, the piston motors segment generated USD 6.2 billion. Piston motors offer higher power density, improved controllability, and greater maximum pressure capacity than other hydraulic motors. By converting hydraulic energy into rotational mechanical energy through reciprocating pistons arranged radially or axially, they provide exceptionally high torque at low rotational speeds.

The low-speed hydraulic motors segment accounted for 60% share in 2025. These motors, operating below 500 RPM, deliver substantial torque with low energy consumption and minimal stress on the system. They are primarily used in heavy-duty applications requiring precise movement and accurate positioning, making them essential for many industrial hydraulic systems.

U.S. Hydraulic Motors Market held 79.4% share, generating USD 3.6 billion in 2025. Rising demand is driven by industries such as construction, mining, agriculture, manufacturing, and material handling. Federal and state infrastructure initiatives, including highway maintenance, bridge construction, renewable energy projects, and industrial facility upgrades, are boosting hydraulic motor adoption. The U.S. manufacturing sector is increasingly incorporating high-capacity hydraulic motors into robotics, automation, and precision machinery, further supporting market growth.

Key players in the Global Hydraulic Motors Market include KYB, Casappa, Concentric AB, Eaton, Bosch Rexroth AG, Linde Hydraulics, Moog, Bucker Hydraulics, Parker Hannifin, Daikin, Fluitronics GmbH, Nachi-Fujikoshi, Kawasaki Heavy Industries, Danfoss Group, and SAI Group. Companies in the Global Hydraulic Motors Market strengthen their foothold by focusing on technological innovation, product diversification, and high-performance solutions. Emphasizing high-torque, low-speed, and piston motor offerings allows manufacturers to address heavy-duty applications across multiple industries. Expanding presence through strategic partnerships, global distribution networks, and local service centers enhances market access. R&D investments drive the development of energy-efficient, durable, and precision-controlled motors, while the adoption of predictive maintenance and smart hydraulic systems improves client satisfaction.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Speed

- 2.2.4 Application

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of construction, agriculture & mining sectors

- 3.2.1.2 Industrial automation & industry 4.0

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment & maintenance costs

- 3.2.2.2 Competition from electric motors

- 3.2.3 Opportunities

- 3.2.3.1 Smart / digitized hydraulic systems

- 3.2.3.2 Development of eco-friendly hydraulic fluids & low-leak systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter';s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Gear motor

- 5.3 Vane motor

- 5.4 Piston motor

Chapter 6 Market Estimates and Forecast, By Speed, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low-speed (< 500 Rpm)

- 6.3 High-speed (>500 Rpm)

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Mining & construction

- 7.3 Oil & gas

- 7.4 Agriculture & forestry

- 7.5 Automotive

- 7.6 Packaging

- 7.7 Machine tool

- 7.8 Material handling

- 7.9 Aerospace & defense

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bosch Rexroth AG

- 9.2 Bucker Hydraulics GmbH

- 9.3 Casappa

- 9.4 Concentric AB

- 9.5 Daikin

- 9.6 Danfoss Group

- 9.7 Eaton

- 9.8 Fluitronics GmbH

- 9.9 SAI Group

- 9.10 KYB

- 9.11 Kawasaki Heavy Industries

- 9.12 Linde Hydraulics

- 9.13 Moog

- 9.14 Nachi-Fujikoshi

- 9.15 Parker Hannifin