PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936477

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936477

Automotive Computer Vision AI Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

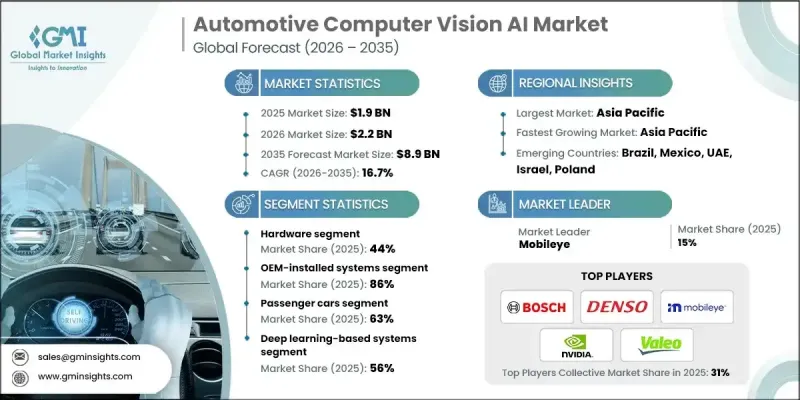

The Global Automotive Computer Vision AI Market was valued at USD 1.9 billion in 2025 and is estimated to grow at a CAGR of 16.7% to reach USD 8.9 billion by 2035.

Automotive manufacturers are embedding vision-based AI to enable vehicles to interpret road conditions, detect objects, and react in real time, significantly improving safety and driving efficiency. The ongoing digital transformation of the automotive sector continues to accelerate adoption across passenger and commercial vehicles. Cost reductions across advanced driver assistance technologies, driven by scale manufacturing, semiconductor innovation, and improved algorithms, are making computer vision solutions viable beyond premium segments. Vision AI is now positioned as a core enabler of next-generation mobility rather than an optional enhancement. The industry is steadily shifting toward data-driven learning architectures that improve perception accuracy in dynamic environments. These developments collectively support rapid market penetration, strong investment momentum, and long-term demand across global automotive ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.9 Billion |

| Forecast Value | $8.9 Billion |

| CAGR | 16.7% |

Advanced driver assistance and vision-based safety features are increasingly offered across mass-market and entry-level vehicles. A 40% reduction in ADAS-related costs over the past five years has improved affordability and adoption. This decline reflects production efficiencies, optimized AI models, and improved chip performance, enabling automakers to deploy computer vision AI at scale. As a result, vehicle buyers now expect intelligent safety and perception capabilities as standard offerings rather than premium add-ons. The automotive computer vision AI landscape is evolving toward unified deep learning architectures that process raw sensor data and generate driving actions without segmented rule-based workflows.

The hardware segment held 44% share in 2025, growing at a CAGR of 16.9% from 2026 to 2035. This segment includes cameras, image sensors, AI acceleration chips, memory units, power control components, and integrated sensor modules. Automotive-grade hardware requires high durability, functional safety compliance, and long operational life, which increases development and production costs. These factors reinforce the central role of hardware in enabling reliable computer vision performance in vehicles.

The OEM-installed solutions segment held an 86% share in 2025 and is projected to grow at a CAGR of 17% through 2035. Automakers prefer factory-installed systems due to regulatory alignment, seamless vehicle integration, warranty coverage, and cost efficiencies achieved through large-scale deployment. Computer vision AI is being embedded during manufacturing across multiple vehicle categories, supporting rapid standardization of features that were once limited to higher-priced models.

China Automotive Computer Vision AI Market held 38% share in 2025 and is forecast to reach USD 1.4 billion by 2035, growing at a CAGR of 17.2%. The country benefits from strong policy support for intelligent vehicles, widespread adoption of electric mobility, and cost-efficient domestic supply chains. Local manufacturers actively compete by integrating vision-based systems as standard features, reinforcing China's leadership in large-scale deployment.

Key companies operating in the Global Automotive Computer Vision AI Market include NVIDIA, Robert Bosch, Mobileye, Continental, Qualcomm Technologies, Magna, Denso, Intel, Valeo, and Aptiv. Companies in the automotive computer vision AI market focus on vertical integration, long-term OEM partnerships, and continuous investment in AI model optimization to strengthen their market position. Many players prioritize scalable hardware-software platforms that can be deployed across multiple vehicle models and regions. Strategic collaborations with semiconductor manufacturers help ensure access to high-performance, automotive-grade chips. Firms also invest heavily in data acquisition and simulation to improve model accuracy and reliability. Expanding manufacturing footprints and localizing supply chains allow companies to reduce costs and meet regional regulatory requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Components

- 2.2.3 Vehicles

- 2.2.4 Technology

- 2.2.5 Deployment Mode

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Increasing adoption of advanced driver assistance systems (ADAS) in vehicles

- 3.2.1.3 Rising demand for autonomous and semi-autonomous vehicles

- 3.2.1.4 Stringent safety and emission regulations encouraging AI-based vision systems

- 3.2.1.5 Technological advancements in AI, machine learning, and sensor fusion

- 3.2.1.6 Growing investment by OEMs and Tier-1 suppliers in smart vehicle technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and integration costs

- 3.2.2.2 Complexity in sensor fusion and real-time data processing

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of autonomous and semi-autonomous vehicles

- 3.2.3.2 Advanced AI algorithms for better perception

- 3.2.3.3 Integration with connected vehicle technologies

- 3.2.3.4 Rising demand for in-cabin monitoring and safety features

- 3.2.3.5 Collaborations between OEMs and tech providers

- 3.2.3.6 Expansion in emerging automotive markets

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- FMVSS and NHTSA guidelines

- 3.4.1.2 Canada - Motor vehicle safety regulations (MVSR)

- 3.4.2 Europe

- 3.4.2.1 Germany- EU General Safety Regulation (GSR)

- 3.4.2.2 UK- Road Vehicles (Approval) Regulations

- 3.4.2.3 France- EU AV and road safety frameworks

- 3.4.2.4 Italy- National Road Safety Plan (PNSS)

- 3.4.3 Asia Pacific

- 3.4.3.1 China- GB/T and GB standards

- 3.4.3.2 India- Motor Vehicles (Amendment) Act and AIS standards

- 3.4.3.3 Japan- Road Traffic Act and MLIT autonomous driving guidelines

- 3.4.3.4 Australia- Australian Design Rules (ADR)

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Use cases & success stories

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Future outlook and opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Cameras (mono, stereo, surround, infrared)

- 5.2.2 Sensors (LiDAR, radar, ultrasonic)

- 5.2.3 Processors & Edge AI chips

- 5.3 Software

- 5.3.1 AI & machine learning algorithms

- 5.3.2 Computer vision platforms

- 5.3.3 Image processing & object detection software

- 5.4 Services

- 5.4.1 System integration

- 5.4.2 Consulting & customization

- 5.4.3 Deployment & installation

- 5.4.4 Maintenance & support

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 SUV

- 6.2.3 Sedan

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

- 6.4 Electric vehicles (EVs)

- 6.5 Autonomous vehicles

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Machine vision-based system

- 7.3 Deep learning-based system

- 7.4 Sensor fusion-based system

Chapter 8 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Advanced driver assistance systems (ADAS)

- 9.2.1 Forward collision warning (FCW)

- 9.2.2 Automatic emergency braking (AEB)

- 9.2.3 Lane departure warning (LDW)

- 9.2.4 Lane keeping assist (LKA)

- 9.2.5 Adaptive cruise control (ACC)

- 9.2.6 Traffic sign recognition (TSR)

- 9.2.7 Blind spot detection (BSD)

- 9.2.8 Parking assist and surround view monitoring

- 9.3 Autonomous driving

- 9.3.1 Object and pedestrian detection

- 9.3.2 Road edge and lane boundary detection

- 9.3.3 Free space detection

- 9.3.4 Environmental mapping

- 9.3.5 Path planning support

- 9.4 In-cabin monitoring

- 9.4.1 Driver monitoring system (DMS)

- 9.4.2 Occupant monitoring system (OMS)

- 9.4.3 Gesture recognition

- 9.4.4 Seatbelt and child presence detection

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aptiv PLC

- 11.1.2 Continental

- 11.1.3 Denso

- 11.1.4 Intel

- 11.1.5 Magna International

- 11.1.6 Mobileye

- 11.1.7 NVIDIA

- 11.1.8 Qualcomm Technologies

- 11.1.9 Robert Bosch

- 11.1.10 Valeo

- 11.2 Regional Players

- 11.2.1 Aisin Seiki

- 11.2.2 Hitachi Astemo

- 11.2.3 Hyundai Mobis

- 11.2.4 Panasonic Automotive

- 11.2.5 Renesas Electronics

- 11.2.6 Samsung Electronics

- 11.2.7 ZF Friedrichshafen

- 11.3 Emerging Technology Innovators

- 11.3.1 Ambarella

- 11.3.2 Arbe Robotics

- 11.3.3 DeepRoute.ai

- 11.3.4 Ficosa International

- 11.3.5 Horizon Robotics

- 11.3.6 Innoviz Technologies

- 11.3.7 StradVision

- 11.3.8 Veoneer