PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936498

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936498

Agri-bulk Ship Loading and Unloading Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

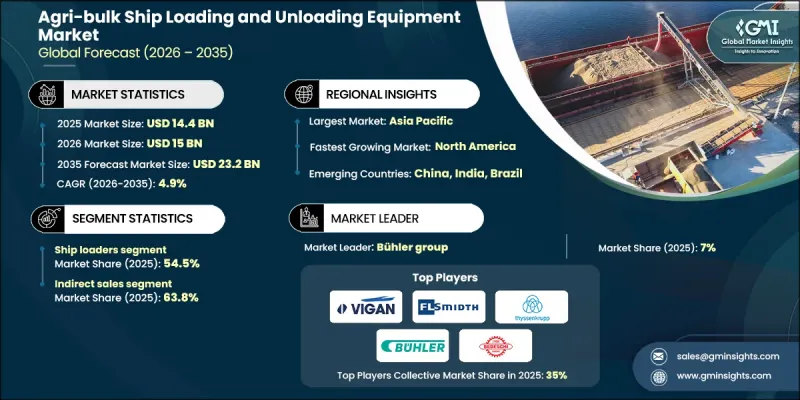

The Global Agri-bulk Ship Loading and Unloading Equipment Market was valued at USD 14.4 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 23.2 billion by 2035.

Demand is fueled by a shift toward automated and mechanized solutions in ports and bulk terminals, as traditional manual operations and gravity-fed systems become less viable for high-throughput agricultural exports. Modern continuous ship unloaders (CSUs) are emerging as a greener solution, incorporating closed conveyor systems, dust suppression, and regenerative braking technology, which can reduce energy consumption by up to 30-40%, aligning with global sustainability goals. Investment in port infrastructure, grain transfer facilities, and industrial maritime hubs is driving adoption across North America, Europe, and Asia-Pacific. Grain traders and terminal operators increasingly prefer high-capacity, automated systems that enhance productivity, minimize product loss, and streamline operations, making technological upgrades a central market trend.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.4 Billion |

| Forecast Value | $23.2 Billion |

| CAGR | 4.9% |

In 2025, the ship loaders segment generated USD 7.8 billion and capturing 54.5% share. Ship loaders are preferred for their ability to increase throughput, reduce vessel turnaround times, and enhance operational safety. Integration of features like telescopic chutes, automated positioning, and dust suppression technology has improved efficiency and reliability. The segment's dominance reflects the industry's ongoing shift toward high-capacity export terminals and advanced maritime handling solutions designed to maximize performance while minimizing environmental impact.

The indirect sales segment accounted for 63.8% share in 2025, highlighting the market's reliance on regional distributors and engineering service providers. This distribution model supports rapid replacement of critical components and on-site maintenance contracts, particularly during peak harvest seasons. Port operators rely on these channels to access localized technical expertise, ensuring uninterrupted operations and timely support for complex equipment.

U.S. Agri-bulk Ship Loading and Unloading Equipment Market held a 64.4% share in 2025, generating substantial demand through investments in grain export infrastructure and modernized port logistics. Environmental compliance, dust control measures, and energy efficiency are major factors shaping procurement decisions. The U.S. market continues to grow as operators focus on improving operational throughput while adhering to stricter environmental regulations.

Leading players in the Global Agri-bulk Ship Loading and Unloading Equipment Market include AGI (Ag Growth International), AUMUND Group, Bedeschi S.p.a., Buhler Group, Cargotec (MacGregor), Ems-tech Inc., FLSmidth, Konecranes, Liebherr-International AG, NEUERO Industrietechnik GmbH, PNM Bulk Handling, Siwertell AB, Thyssenkrupp AG, VIGAN Engineering S.A., and WAMGROUP S.p.A. Companies in Agri-bulk Ship Loading and Unloading Equipment Market are strengthening their presence through several strategies. They are investing in R&D to develop more energy-efficient, dust-free, and automated shiploader and unloader systems. Strategic partnerships with ports, grain terminals, and distributors enable better regional coverage and faster delivery of service contracts. Firms are expanding manufacturing capacities across Europe, North America, and Asia-Pacific to meet rising demand and reduce lead times. Additionally, companies are offering lifecycle services, predictive maintenance solutions, and modular system upgrades, which increase customer loyalty and reinforce long-term market positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global food security and grain trade expansion

- 3.2.1.2 Smart port initiatives and automation

- 3.2.1.3 Environmental regulations and dust control

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial CAPEX & infrastructure costs

- 3.2.2.2 Complexity of retrofitting existing berths

- 3.2.3 Opportunities

- 3.2.3.1 Digital twins and predictive maintenance

- 3.2.3.2 Digital twins and predictive maintenance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Automatic

- 5.4 Semi-automatic

Chapter 6 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Direct

- 6.3 Indirect

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 AGI (Ag Growth International)

- 8.2 AUMUND Group

- 8.3 Bedeschi S.p.a.

- 8.4 Buhler Group

- 8.5 Cargotec (MacGregor)

- 8.6 Ems-tech Inc.

- 8.7 FLSmidth

- 8.8 Konecranes

- 8.9 Liebherr-International AG

- 8.10 NEUERO Industrietechnik GmbH

- 8.11 PNM Bulk Handling

- 8.12 Siwertell AB

- 8.13 Thyssenkrupp AG

- 8.14 VIGAN Engineering S.A.

- 8.15 WAMGROUP S.p.A