PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936506

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936506

Vertical Farming Automation System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

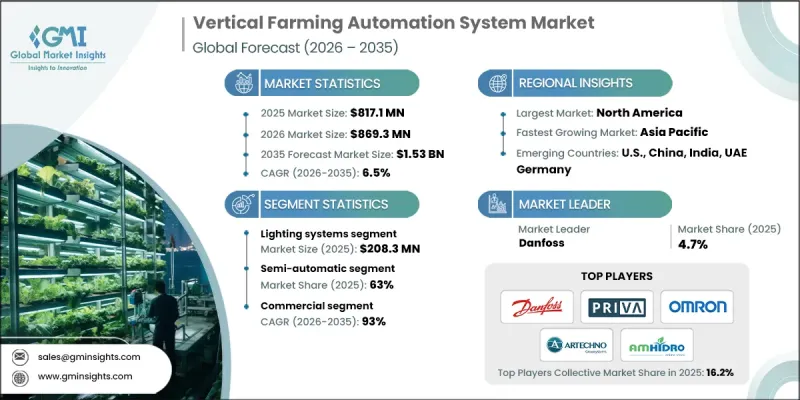

The Global Vertical Farming Automation System Market was valued at USD 817.1 million in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 1.53 billion by 2035.

Growth is driven by the need to maximize crop output in constrained spaces while reducing resource consumption. Vertical farming relies on stacked cultivation systems that allow higher yields with lower water usage and reduced dependency on chemical inputs. Automation plays a central role in improving productivity, consistency, and operational efficiency across these controlled environments. Supportive government initiatives and financial incentives that encourage sustainable farming practices further contribute to market expansion. Awareness of environmental benefits, such as water efficiency and reduced land use, strengthens adoption across regions. Advanced lighting technologies remain essential to vertical farming, as artificial illumination replicates optimal growth conditions for different crops. Modern LED solutions enable precise control of light intensity and spectrum while minimizing heat output, allowing closer placement to crops and improved space utilization. Dynamic lighting systems enhance growth cycles, improve yield quality, and support nutrient optimization throughout cultivation stages.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $817.1 Million |

| Forecast Value | $1.53 Billion |

| CAGR | 6.5% |

The lighting systems segment generated USD 208.3 million in 2025 and is expected to grow at a CAGR of 6.7% during 2026-2035. Demand rises alongside the need for accurate environmental management within vertical farms. Climate control solutions regulate temperature, humidity, and carbon dioxide levels to ensure uniform crop development. Advancements in intelligent climate management improve system efficiency while lowering operating costs. Lighting remains a critical component because it directly influences plant development, productivity, and quality. Energy-efficient LED technologies continue gaining preference due to their adaptability across crop types and growth phases.

The commercial segment is projected to grow at a CAGR of 93% from 2026 to 2035. Commercial operations increasingly depend on automation to support large-scale food production, reduce labor intensity, and maintain consistent crop quality. Technologies such as robotics, artificial intelligence, and connected systems support yield optimization and operational reliability.

United States Vertical Farming Automation System Market held 77% share, generating USD 320.1 million in 2025. Growth is supported by rising urbanization, demand for sustainable food systems, and the need to enhance agricultural efficiency. Increased adoption of urban farming solutions brings food production closer to consumption centers, reducing logistical complexity and improving supply freshness.

Key companies operating in the Global Vertical Farming Automation System Market include Signify Holding, Danfoss, OMRON Corporation, Heliospectra, Swisslog, American Hydroponics, Priva, AutoStore, Jungheinrich, Artechno Growsystems, Green Automation, Modula USA, Logiqs, Arianetech, and TTA. Companies in the vertical farming automation system market strengthen their market position by investing in advanced automation technologies that improve precision, scalability, and energy efficiency. Many focus on integrating AI-driven monitoring systems to optimize growing conditions and reduce operational costs. Strategic partnerships with agricultural operators help accelerate system adoption and customization. Manufacturers emphasize modular system designs to support flexible deployment and future expansion. Continuous innovation in lighting, climate control, and data analytics enhances performance differentiation. Expanding global distribution networks and offering long-term technical support further reinforce customer confidence.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System Type

- 2.2.3 Technology Type

- 2.2.4 Automation Level

- 2.2.5 Crop Type

- 2.2.6 End Users

- 2.2.7 Distribution Channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By system type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By System Type, 2022 - 2035 ($Million, Thousand Units)

- 5.1 Key trends

- 5.2 Climate control systems

- 5.2.1 HVAC systems

- 5.2.2 Dehumidifiers

- 5.2.3 Humidification systems

- 5.2.4 Ventilation systems

- 5.2.5 Others (Co2 injection/enrichment systems etc.)

- 5.3 Lighting systems

- 5.3.1 LED grow light systems

- 5.3.2 Fluorescent light systems

- 5.3.3 Others (light distribution hardware etc.)

- 5.4 Irrigation & fertigation systems

- 5.4.1 Drip irrigation systems

- 5.4.2 Automated dosing equipment

- 5.4.3 Water filtration & treatment systems

- 5.4.4 Others (nutrient film technique systems etc.)

- 5.5 Sensor & monitoring hardware

- 5.5.1 Environmental sensors

- 5.5.2 Light measurement sensors

- 5.5.3 Gas sensors

- 5.5.4 Others (water quality sensors etc.)

- 5.6 Others (robotic automation systems etc.)

Chapter 6 Market Estimates & Forecast, By Technology Type, 2022 - 2035 ($Million, Thousand Units)

- 6.1 Key trends

- 6.2 Hydroponics

- 6.3 Aeroponics

- 6.4 Aquaponics

Chapter 7 Market Estimates & Forecast, By Automation Level, 2022 - 2035 ($Million, Thousand Units)

- 7.1 Key trends

- 7.2 Semi-automatic

- 7.3 Fully automatic

Chapter 8 Market Estimates & Forecast, By Crop Type, 2022 - 2035 ($Million, Thousand Units)

- 8.1 Key trends

- 8.2 Leafy greens & herbs

- 8.3 Fruiting vegetables

- 8.4 Flowers & ornamentals

- 8.5 Others (medicinal plants etc.)

Chapter 9 Market Estimates & Forecast, By End Users, 2022 - 2035 ($Million, Thousand Units)

- 9.1 Key trends

- 9.2 Individual/residential

- 9.3 Commercial

- 9.3.1 Retail & Hospitality

- 9.3.2 Restaurants

- 9.3.3 Grocery stores

- 9.3.4 Others (research & educational institutions etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Million, Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Million, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 American Hydroponics

- 12.2 Arianetech

- 12.3 Artechno Growsystems

- 12.4 AutoStore

- 12.5 Danfoss

- 12.6 Green Automation

- 12.7 Heliospectra

- 12.8 Jungheinrich

- 12.9 Logiqs

- 12.10 Modula USA

- 12.11 OMRON Corporation

- 12.12 Priva

- 12.13 Signify Holding

- 12.14 Swisslog

- 12.15 TTA