PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936540

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936540

Liquid Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

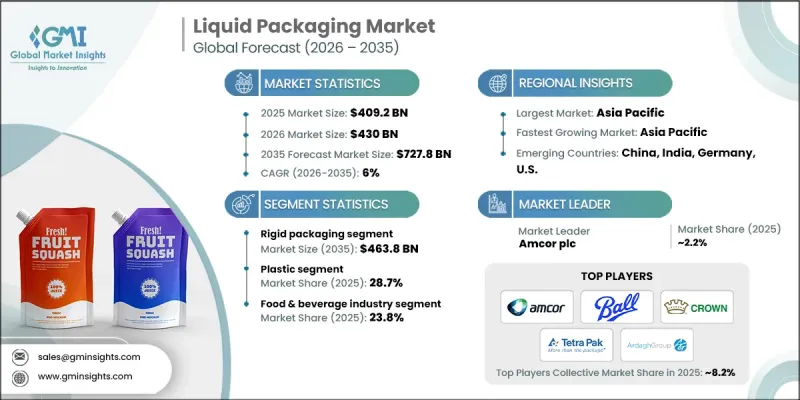

The Global Liquid Packaging Market was valued at USD 409.2 billion in 2025 and is estimated to grow at a CAGR of 6% to reach USD 727.8 billion by 2035.

Market growth is supported by rising demand for packaging solutions that ensure safety, convenience, and environmental responsibility across food, beverage, pharmaceutical, and consumer product applications. Increasing consumption of packaged liquids in both developed and emerging economies continues to drive demand, while regulatory pressure related to sustainability is reshaping material selection and packaging design. The market landscape is evolving rapidly as manufacturers respond to consumer preferences for lightweight, durable, and recyclable packaging formats. Advances in material science and production efficiency are enabling companies to reduce packaging weight while maintaining performance standards. The growth of e-commerce has further increased the need for protective liquid packaging capable of withstanding complex logistics and distribution networks. In parallel, packaging suppliers are adopting intelligent and traceable packaging solutions that enhance product transparency, improve supply chain monitoring, and reinforce brand trust. These developments, combined with cost optimization and sustainability goals, are accelerating global adoption and reshaping long-term market dynamics.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $409.2 Billion |

| Forecast Value | $727.8 Billion |

| CAGR | 6% |

The rigid packaging segment is expected to generate USD 463.8 billion by 2035. This segment continues to maintain a strong position due to its structural strength, long shelf-life protection, and strong consumer acceptance across premium and mass-market liquid products. Improvements in material engineering have enabled manufacturers to reduce overall packaging weight while preserving durability and performance. These characteristics support efficient filling processes, streamlined transportation, and consistent product quality, allowing rigid formats to remain a preferred choice for large-scale production and distribution.

The plastic segment held 28.7% share in 2025 and is growing at a CAGR of 6.5% through 2035. Its continued dominance is supported by cost efficiency, versatility, and compatibility with high-speed manufacturing systems. Manufacturers favor plastic-based solutions for their ability to support scalable production while maintaining consistent quality standards. These advantages contribute to widespread adoption across a broad range of liquid applications, reinforcing plastic's role as a core material in the global packaging ecosystem.

North America Liquid Packaging Market generated USD 88.1 billion in 2025. The region benefits from mature consumer markets, advanced manufacturing infrastructure, and sustained investment in packaging innovation. A robust network of packaging producers, material suppliers, and brand owners actively supports the development of sustainable designs, enhanced barrier performance, and efficient filling technologies. These factors collectively strengthen North America's contribution to global market expansion.

Key participants in the Global Liquid Packaging Industry include Tetra Pak International SA, Amcor plc, SIG Combibloc Group AG, Ball Corporation, Ardagh Group, Crown Holdings, Inc., ALPLA Group, O-I Glass (Owens-Illinois), WestRock Company, International Paper Company, Huhtamaki Oyj, Smurfit Kappa Group plc, Elopak AS, Evergreen Packaging Inc., Stora Enso Oyj, Greatview Aseptic Packaging Co., and Nippon Paper Industries Co., Ltd. Companies operating in the liquid packaging market are strengthening their competitive position through sustainability-driven innovation, capacity expansion, and strategic collaboration. Leading players are investing in recyclable and lightweight material technologies to align with regulatory requirements and consumer expectations. Many firms are enhancing production efficiency through automation and digitalization while expanding global manufacturing footprints to serve high-growth regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Material trends

- 2.2.3 End Use Industries trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of sustainable barrier coatings.

- 3.2.1.2 Growing consumer preference for smaller pack sizes.

- 3.2.1.3 E-commerce expansion is driving demand for advanced liquid packaging solutions.

- 3.2.1.4 Integration of IoT and real-time logistics sensors driving innovation in liquid packaging.

- 3.2.1.5 Customer experience enhancement driving adoption of user-friendly liquid packaging.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising costs of key raw materials impacting the liquid packaging market

- 3.2.2.2 Limited recycling infrastructure hindering growth of the liquid packaging market

- 3.2.3 Market opportunities

- 3.2.4 Leveraging real-time supply-chain insights and data-driven predictive planning to enhance distribution and efficiency.

- 3.2.5 Smart warehousing and robotics as a strategic opportunity to optimize safety and efficiency in liquid packaging.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2022-2025)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2026-2035)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability roi analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Liquid Packaging Market Estimates & Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends,

- 5.2 Flexible packaging

- 5.3 Rigid packaging

Chapter 6 Liquid Packaging Market Estimates and Forecast, By Materials, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Paper & boards

- 6.4 Glass

- 6.5 Metal

- 6.6 Others

Chapter 7 Liquid Packaging Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Personal care

- 7.4 Pharmaceutical

- 7.5 Household care

- 7.6 Industrial

- 7.7 Others

Chapter 8 Liquid Packaging Market Estimates & Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends, by region

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Rest of Europe

- 8.4 Asia-Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Rest of Asia-Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of MEA

Chapter 9

- 9.1 Amcor plc

- 9.2 Ball Corporation

- 9.3 Crown Holdings, Inc.

- 9.4 Tetra Pak International SA

- 9.5 Ardagh Group

- 9.6 O-I Glass (Owens-Illinois)

- 9.7 SIG Combibloc Group AG

- 9.8 Elopak AS

- 9.9 Greatview Aseptic Packaging Co.

- 9.10 Evergreen Packaging Inc.

- 9.11 Stora Enso Oyj

- 9.12 Nippon Paper Industries Co., Ltd.

- 9.13 Smurfit Kappa Group plc

- 9.14 WestRock Company

- 9.15 International Paper Company

- 9.16 ALPLA Group

- 9.17 Huhtamaki Oyj

- 9.18 Liqui-Box Corporation

- 9.19 Comar LLC