PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936551

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936551

Automotive Front Windshield Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

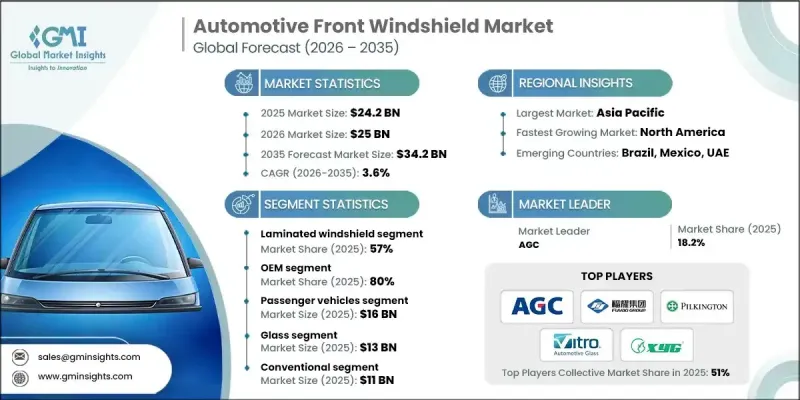

The Global Automotive Front Windshield Market was valued at USD 24.2 billion in 2025 and is estimated to grow at a CAGR of 3.6% to reach USD 34.2 billion by 2035.

The market is experiencing consistent expansion driven by rising global vehicle production, increasingly strict vehicle safety standards, and the rapid integration of advanced driver-assistance technologies. Automakers are prioritizing enhanced driver visibility, improved passenger protection, reduced cabin noise, and better thermal insulation, which is accelerating the adoption of advanced front windshield solutions. Windshields are no longer passive components and are engineered to support sensors, cameras, and display systems that are essential for modern vehicle safety and automation features. Growth in electric and premium vehicle production is further boosting demand for lightweight, acoustically optimized, and technologically integrated windshields. Manufacturers and suppliers are increasingly focusing on multifunctional designs that combine safety, comfort, and digital compatibility while meeting evolving regulatory and performance expectations across global automotive markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24.2 Billion |

| Forecast Value | $34.2 Billion |

| CAGR | 3.6% |

Ongoing innovations in windshield technology are reshaping traditional designs by improving durability, functionality, and passenger comfort. Advanced laminated glass structures, thermal and light-reflective coatings, sound-dampening interlayers, and display-ready surfaces are enhancing impact resistance, reducing interior noise, and supporting seamless system integration. The use of strengthened glass and advanced polymer layers is enabling better optical clarity, longer service life, and weight optimization, helping manufacturers align with safety regulations and efficiency targets while supporting next-generation vehicle architectures.

The laminated windshields segment accounted for 57% share in 2025 and is expected to grow at a CAGR of 4% from 2026 to 2035. This segment leads due to its essential role in safety performance, structural integrity, and compatibility with advanced vehicle systems. Multi-layer construction allows for the incorporation of sound-control films, thermal coatings, and sensor integration, making laminated windshields the preferred solution for both passenger and commercial vehicles.

The OEM segment represented 80% share in 2025 and is forecast to grow at a CAGR of 3.8% during 2026-2035. OEM-installed windshields dominate the market because they ensure precise fitment, seamless system integration, consistent quality control, and compliance with global safety requirements. Vehicle manufacturers rely on OEM solutions to support advanced windshield technologies and meet regulatory and performance standards.

China Automotive Front Windshield Market held 41% share in 2025, generating USD 3.9 billion. The country leads regional demand due to high vehicle manufacturing volumes, strong adoption of advanced windshield technologies, and close collaboration across the automotive supply chain. Supportive industrial policies, large-scale production capabilities, and integrated supplier networks continue to accelerate the deployment of technologically advanced front windshields across domestic vehicle platforms.

Key companies operating in the Global Automotive Front Windshield Market include Saint-Gobain Sekurit, Fuyao Glass Industry, AGC, Xinyi Glass, Guardian Industries, Vitro Automotive Glass, NSG Group (Pilkington), Pilkington Automotive, PPG Industries, and Sekurit Saint-Gobain Automotive Glass. Companies in the Automotive Front Windshield Market are strengthening their market position by investing in advanced glass processing technologies and multifunctional windshield solutions. Manufacturers are expanding R&D efforts to support ADAS compatibility, acoustic performance, and thermal efficiency while reducing weight. Strategic partnerships with automakers and Tier 1 suppliers are enabling early integration of new technologies into vehicle platforms. Firms are also increasing production capacity in key automotive regions to improve supply reliability and cost efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 Material

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Vehicle Production

- 3.2.1.2 Stringent Safety Regulations

- 3.2.1.3 Advanced Technology Integration

- 3.2.1.4 Electric & Premium Vehicle Growth

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Manufacturing Costs

- 3.2.2.2 Complex Installation & Calibration

- 3.2.3 Market opportunities

- 3.2.3.1 Smart Windshield Adoption

- 3.2.3.2 Expansion of Emerging Markets

- 3.2.3.3 Increasing focus on vehicle safety regulations

- 3.2.3.4 Advancements in coating and interlayer technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: NHTSA, DOT, and AI Safety Regulations

- 3.4.1.2 Canada: Transport Canada, CMVSS 205

- 3.4.2 Europe

- 3.4.2.1 Germany: BMDV, UNECE R43 Automotive Safety Glazing

- 3.4.2.2 France: Ministry of Transport, Safety Glazing Standards

- 3.4.2.3 UK: Department for Transport, Construction & Use Regulations

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport, Vehicle Glazing Rules

- 3.4.3 Asia Pacific

- 3.4.3.1 China: MIIT, GB Automotive Safety Glass Standards

- 3.4.3.2 Japan: MLIT, JIS Automotive Safety Glazing

- 3.4.3.3 South Korea: MOLIT, KS Safety Glass Regulations

- 3.4.3.4 India: MoRTH, AIS & CMVR Automotive Glazing Norms

- 3.4.4 Latin America

- 3.4.4.1 Brazil: DENATRAN, CONTRAN Automotive Glazing Standards

- 3.4.4.2 Mexico: Ministry of Communications & Transport, Vehicle Safety Regulations

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA Vehicle Safety & Glazing Standards

- 3.4.5.2 Saudi Arabia: Ministry of Communications & Transport, SASO Vehicle Regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Use case scenarios

- 3.14 OEM Sourcing & Procurement Dynamics

- 3.14.1 Windshield supplier qualification criteria

- 3.14.2 Long-term supply contracts vs spot sourcing

- 3.14.3 OEM pricing pressure & localization mandates

- 3.15 ADAS & Sensor Integration Economics

- 3.15.1 Cost impact of camera-based ADAS calibration

- 3.15.2 HUD, LiDAR, rain/light sensor integration complexity

- 3.15.3 Replacement vs recalibration economics in aftermarket

- 3.16 Aftermarket Replacement Economics

- 3.16.1 Insurance-driven replacement cycles

- 3.16.2 Price difference: OEM vs aftermarket glass

- 3.16.3 Role of mobile installation service providers

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Laminated Windshield

- 5.3 Tempered Windshield

- 5.4 Smart / Advanced Windshield

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Conventional

- 7.3 Heated

- 7.4 Acoustic

- 7.5 Heads-Up Display (HUD) Enabled

Chapter 8 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Glass

- 8.3 Polymer Interlayer

- 8.4 Coatings & Films

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 AGC

- 11.1.2 Fuyao Glass Industry

- 11.1.3 Guardian Industries

- 11.1.4 NSG (Pilkington)

- 11.1.5 Pilkington Automotive

- 11.1.6 PPG Industries

- 11.1.7 Saint-Gobain Sekurit

- 11.1.8 Vitro Automotive Glass

- 11.1.9 Xinyi Glass

- 11.2 Regional Player

- 11.2.1 Asahi India Glass Limited (AIS)

- 11.2.2 Benson Automotive Glass

- 11.2.3 Cardinal Automotive Glass

- 11.2.4 Glasslam Europe

- 11.2.5 Olimpia Auto Glass

- 11.2.6 Samvardhana Motherson Automotive Glass

- 11.2.7 Shanghai Yaohua Pilkington Glass

- 11.2.8. Sisecam Automotive

- 11.2.9 Soliver

- 11.2.10 Trakya Cam Automotive

- 11.3 Emerging Players

- 11.3.1 AGP

- 11.3.2 Kibing

- 11.3.3 Nippon Electric Glass

- 11.3.4 PGW Auto Glass

- 11.3.5 Xinyi Overseas Automotive Glass Units