PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936555

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936555

Printed Circuit Board (PCB) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

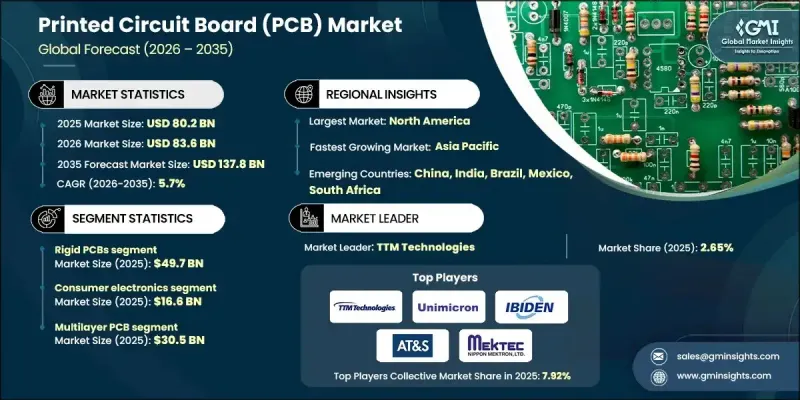

The Global Printed Circuit Board (PCB) Market was valued at USD 80.2 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 137.8 billion by 2035.

The growth is driven by the increasing complexity of modern electronic devices and the shift toward larger and more sophisticated PCB designs. Industries are demanding highly efficient assembly machines capable of handling multi-layer, high-density boards while maintaining thermal stability and signal integrity. The proliferation of 5G networks, AI computing, and high-speed data centers has fueled the need for advanced materials and ultra-low-loss PCBs. The industry is embracing automated assembly, precision soldering, and inspection tools to ensure quality, reliability, and scalability across sectors, including consumer electronics, industrial machinery, telecommunications, and wearable technology. Rising demand for miniaturized, flexible, and multi-directional devices is further boosting the adoption of advanced PCBA solutions globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $80.2 billion |

| Forecast Value | $137.8 billion |

| CAGR | 5.5% |

The flexible PCB segment generated USD 44 billion in 2025. Flexible assemblies are highly sought for their lightweight, compact designs, multi-directional connectivity, and integration into wearables, medical devices, IoT, and automotive systems. Their established production processes and scalability make them ideal for high-volume manufacturing.

The wave soldering segment accounted for USD 52.8 billion in 2025 and remains a preferred method for high-volume PCB assembly. Its uniform solder application, reliability, and suitability for through-hole components make it critical for complex board manufacturing. Growing automation in production lines continues to drive wave soldering adoption across various industries.

North America Printed Circuit Board (PCB) Market held 75.9% share in 2025. Strong demand from aerospace, defense, medical electronics, and automotive sectors, combined with reshoring initiatives and government incentives such as the U.S. CHIPS Act, has strengthened domestic PCB assembly capabilities. Adoption of HDI and flexible assemblies is rising with 5G deployment and electric vehicle integration, while sustainability efforts are accelerating the use of lead-free and eco-friendly materials.

Key players in the Global Printed Circuit Board (PCB) Market include Alfa Electronics, ALLPCB.com, Altek Electronics, Inc., Benchmark Electronics, Inc., Bittele Electronics Inc., Clarydon Electronic Services Limited, Eurocircuits, Jayshree Instruments Pvt. Ltd, Miracle Electronics Devices Pvt Ltd, PCB Assembly Express, INC, PCB Power Market, PCB Unlimited, PCBGOGO, PCBWay, Podrain Electronics, RAYMING TECHNOLOGY, Seeed Technology Co., Ltd., Tempo, Vexos, Visual Communications Company, LLC, and WellPCB Technology Co., Ltd. Companies in the Printed Circuit Board (PCB) Market are employing several strategies to strengthen their market position. These include investing in R&D for high-density and flexible PCB assembly technologies, expanding production capacities to meet growing demand, and adopting automation to improve efficiency and reduce defects. Strategic partnerships, mergers, and acquisitions allow firms to broaden their client base and enter new geographic regions. Companies are also prioritizing sustainability by introducing lead-free and environmentally friendly manufacturing processes. Offering end-to-end solutions, including design, assembly, testing, and after-sales support, enhances customer loyalty and long-term retention, while digitalization and AI-enabled production lines improve quality control and operational agility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 PCB structure trends

- 2.2.3 Type trends

- 2.2.4 Substrate trends

- 2.2.5 End Use industry trends

- 2.2.6 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand from Consumer Electronics and IoT Devices

- 3.2.1.2 Expansion of Automotive Electronics and Electric Vehicles (EVs)

- 3.2.1.3 Growing Adoption in 5G Infrastructure and Telecommunications

- 3.2.1.4 Increased Use in Industrial Automation and Smart Manufacturing

- 3.2.1.5 Advancements in High-Density Interconnect (HDI) and Flexible PCBs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply Chain Disruptions and Raw Material Volatility

- 3.2.2.2 High Manufacturing Complexity and Cost Pressures

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with Electric Vehicles (EVs) and Advanced Automotive Electronics

- 3.2.3.2 Expansion into 5G Infrastructure and Telecommunications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Sustainability Measures

- 3.13 Consumer Sentiment Analysis

- 3.14 Patent and IP analysis

- 3.15 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive Benchmarking of key Players

- 4.3.1 Financial Performance Comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit Margin

- 4.3.1.3 R&D

- 4.3.2 Product Portfolio Comparison

- 4.3.2.1 Product Range Breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1 Global Footprint Analysis

- 4.3.3.2 Service Network Coverage

- 4.3.3.3 Market Penetration by Region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche Players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial Performance Comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and Acquisitions

- 4.4.2 Partnerships and Collaborations

- 4.4.3 Technological Advancements

- 4.4.4 Expansion and Investment Strategies

- 4.4.5 Sustainability Initiatives

- 4.4.6 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates and Forecast, By PCB Structure, 2022 - 2035 ($ Bn & Units)

- 5.1 Key trends

- 5.2 Rigid PCB

- 5.3 Flexible PCB (FPC)

- 5.4 Rigid-flex PCB

Chapter 6 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Bn & Units)

- 6.1 Key trends

- 6.2 Single-sided PCB

- 6.3 Double-sided PCB

- 6.4 Multilayer PCB

- 6.5 High-Layer-Count PCB

Chapter 7 Market Estimates and Forecast, By Substrate, 2022 - 2035 ($ Bn & Units)

- 7.1 Key trends

- 7.2 FR-4 (Glass Epoxy)

- 7.3 Metal-core

- 7.4 Polyimide

- 7.5 PTFE

- 7.6 Ceramic Substrate

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 ($ Bn & Units)

- 8.1 Key trends

- 8.2 Consumer Electronics

- 8.3 Automotive

- 8.4 Telecommunications

- 8.5 Industrial Electronics

- 8.6 Medical Devices

- 8.7 Aerospace & Defense

- 8.8 Computing & Data Centers

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Bn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players:

- 10.1.1 AT&S

- 10.1.2 Ibiden

- 10.1.3 Nippon Mektron

- 10.1.4 Samsung Electro-Mechanics

- 10.1.5 Tripod Technology

- 10.1.6 TTM Technologies

- 10.1.7 Unimicron

- 10.2 Regional Players

- 10.2.1 Allied Circuit (ACCL)

- 10.2.2 Benchmark Electronics

- 10.2.3 Compeq Manufacturing

- 10.2.4 Daeduck Electronics

- 10.2.5 Meiko Electronics

- 10.2.6 Sanmina

- 10.2.7 Schweizer Electronic

- 10.3 Emerging Players

- 10.3.1 Cirexx

- 10.3.2 Epec

- 10.3.3 Flex

- 10.3.4 Jabil

- 10.3.5 Sheldahl (Multek / Flex subsidiary)