PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936557

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936557

Surgical Navigation Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

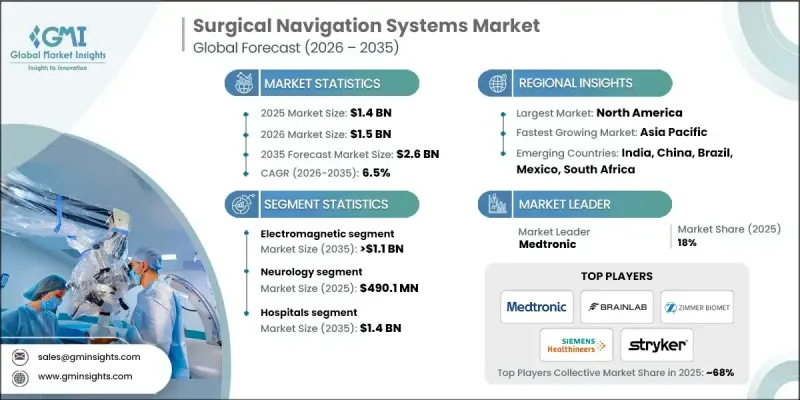

The Global Surgical Navigation Systems Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 2.6 billion by 2035.

Market growth is driven by the rising number of complex surgical procedures, increasing adoption of minimally invasive surgeries, and continuous technological advancements in imaging and navigation. Surgical navigation systems provide computer-assisted, real-time visualization, helping surgeons plan and execute procedures with higher accuracy, safety, and efficiency. By combining pre-operative or intraoperative imaging with advanced tracking devices, these systems improve outcomes in orthopedic, neurosurgical, ENT, and spinal interventions. Innovations such as 3D imaging, AI-enabled software, real-time tracking, and integration with CT/MRI have enhanced usability and precision. Augmented reality and virtual reality are increasingly incorporated to overlay digital guides onto the surgical field, enabling surgeons to reduce cognitive load, optimize intraoperative decision-making, and enhance surgical planning. Rising awareness of the benefits of accurate, minimally invasive procedures is prompting hospitals to invest in advanced navigation technologies, fueling sustained market growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 6.5% |

The electromagnetic navigation segment held 44.5% share in 2025. Its popularity stems from high tracking accuracy without line-of-sight limitations, ease of use in complex anatomical regions, and strong adoption in ENT, neurosurgery, and minimally invasive procedures. Electromagnetic systems allow surgeons to visualize the exact position of instruments in real-time, even when direct visual access is blocked. This precise localization enhances safety and ensures accurate navigation through deep or restricted surgical sites, making it indispensable for complex interventions.

The neurology segment generated USD 490.1 million in 2025 and is expected to grow at a CAGR of 5.9% from 2026 to 2035. The increasing prevalence of brain tumors, epilepsy, stroke, and degenerative neurological disorders is driving demand for precise neurosurgical procedures. Navigation systems enable surgeons to accurately target lesions while avoiding critical brain structures, reducing complications, and improving postoperative recovery. Real-time guidance ensures delicate operations are performed with minimal risk to vital tissues, directly enhancing clinical outcomes and patient safety.

U.S. Surgical Navigation Systems Market was valued at USD 497.1 million in 2025, reflecting strong adoption of navigation systems in North American healthcare facilities. Hospitals in the region prioritize minimally invasive procedures and accurate interventions to improve patient outcomes, which has increased the reliance on surgical navigation systems. Additionally, North America leads in clinical research and trials involving advanced surgical technologies. Evidence generated from these studies validates the effectiveness of navigation systems, encouraging widespread adoption among clinicians. Government support, advanced hospital infrastructure, and high healthcare expenditure further strengthen the region's market dominance.

Key players operating in the Global Surgical Navigation Systems Market include Philips, Medtronic, Stryker, Zimmer Biomet, Johnson & Johnson, KARL STORZ, Amplitude Surgical, B. BRAUN, Corin, Fiagon, BRAINLAB, Siemens Healthineers, and Smith+Nephew. Companies in the surgical navigation systems market are expanding their presence by focusing on technological innovation, developing AI-enabled and AR/VR-integrated platforms, and enhancing product accuracy and usability. Strategic collaborations with hospitals, research institutes, and clinical trial organizations allow companies to validate solutions and increase adoption. Expanding geographic reach, establishing regional distribution networks, and providing comprehensive after-sales and training services strengthen market foothold. Manufacturers are also investing in modular, customizable systems for diverse surgical specialties to address niche requirements.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for minimally invasive surgical procedures

- 3.2.1.2 Technological advancements in surgical navigation systems

- 3.2.1.3 Rise in orthopedic and neurology disorders

- 3.2.1.4 Surging target patient pool of ENT disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High instrument and procedural costs

- 3.2.2.2 Stringent government regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Increasing use in non-traditional specialties

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Start-up scenarios

- 3.7 Future market trends

- 3.8 Value chain analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Electromagnetic

- 5.3 Optical

- 5.4 Hybrid

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Neurology

- 6.3 Orthopedic

- 6.3.1 Knee

- 6.3.2 Hip

- 6.3.3 Shoulder

- 6.4 ENT

- 6.5 Dental

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amplitude Surgical

- 9.2 B. BRAUN

- 9.3 BRAINLAB

- 9.4 Corin

- 9.5 Fiagon

- 9.6 Johnson & Johnson

- 9.7 KARL STORZ

- 9.8 Medtronic

- 9.9 Philips

- 9.10 Siemens Healthineers

- 9.11 Smith+Nephew

- 9.12 Stryker

- 9.13 Zimmer Biomet