PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936576

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936576

Vehicle Tolling System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

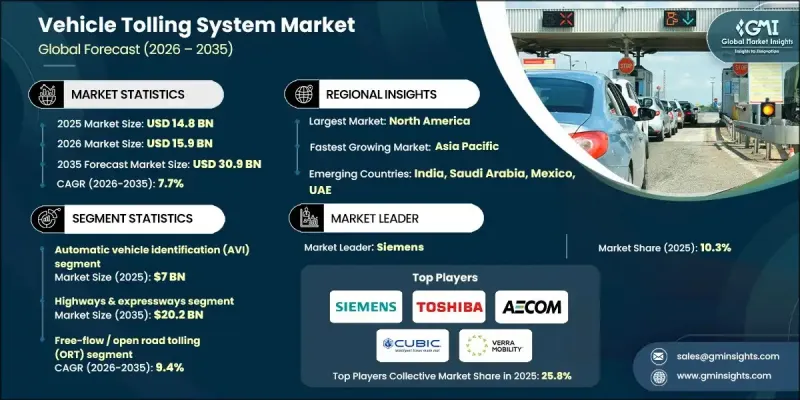

The Global Vehicle Tolling System Market was valued at USD 14.8 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 30.9 billion by 2035.

Governments worldwide are accelerating the adoption of electronic and connected tolling solutions through infrastructure modernization policies and regulatory support. Cashless tolling is increasingly viewed as essential for reducing congestion, improving road efficiency, and enhancing user convenience across passenger and commercial transport. Digital tolling platforms now manage extensive tolled road networks, enabling automated payment processing and smoother traffic movement. Public investment frameworks continue to support congestion management and intelligent transport systems, reinforcing long-term demand. Transport authorities are rapidly replacing physical toll booths with advanced electronic models that allow uninterrupted vehicle movement. Interoperability requirements are becoming standard, allowing a single vehicle identification device to function across multiple regions. Industry data indicates that nearly 78% of toll transactions worldwide are now processed electronically. Collaboration between public agencies and private operators is improving system compatibility, simplifying user access, and reducing administrative complexity.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.8 Billion |

| Forecast Value | $30.9 Billion |

| CAGR | 7.7% |

The automatic vehicle identification segment generated USD 7 billion in 2025. This segment leads due to its ability to deliver fast and accurate vehicle recognition using electronic identification technologies. Automated identification reduces manual intervention, improves toll accuracy, and supports seamless integration with modern tolling infrastructure. Rising deployment of electronic toll collection systems globally continues to support strong growth for this segment.

The highways and expressways segment accounted for 68.1% share in 2025 and is expected to reach USD 20.2 billion by 2035. These roadways dominate tolling investments due to high traffic density, consistent revenue generation, and early adoption of advanced tolling technologies that support long-distance and high-speed travel.

US Vehicle Tolling System Market reached USD 5.1 billion in 2025. State-level initiatives focus on improving freight efficiency, enhancing regional connectivity, and reducing congestion through expanded toll road networks. Automated tolling technologies are increasingly replacing manual collection to improve operational efficiency and traffic flow.

Key companies operating in the Global Vehicle Tolling System Market include Thales, Siemens, Kapsch TrafficCom, Cubic, Conduent, Toshiba, Verra Mobility, ST Engineering, AECOM, and Mundys. Companies in the vehicle tolling system market strengthen their competitive position by investing in advanced digital platforms, interoperability standards, and scalable infrastructure solutions. Providers focus on developing end-to-end tolling ecosystems that integrate hardware, software, analytics, and back-office operations. Strategic partnerships with governments and infrastructure operators support long-term contracts and large-scale deployments. Firms also prioritize data security, real-time traffic analytics, and system reliability to meet regulatory and user expectations. Expansion into emerging regions, along with modular solutions that support multi-lane free-flow environments, helps companies capture new revenue streams and reinforce their global market presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 System

- 2.2.4 Technology

- 2.2.5 Tolling Method

- 2.2.6 Payment Method

- 2.2.7 Application

- 2.2.8 Vehicle

- 2.2.9 End Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of electronic toll collection (ETC) systems

- 3.2.1.2 Increasing road infrastructure development and highway expansion

- 3.2.1.3 Growing traffic congestion and need for efficient traffic management

- 3.2.1.4 Integration of RFID, ANPR, and GNSS technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Interoperability challenges across tolling systems

- 3.2.2.2 Operational and maintenance complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of open road tolling and barrier-free systems

- 3.2.3.2 Adoption of GNSS-based and distance-based tolling

- 3.2.3.3 Growth opportunities in emerging economies

- 3.2.3.4 Public-private partnerships (PPPs) in toll road projects

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Highway Administration (FHWA) - USA

- 3.4.1.2 State Road and Tollway Authority (SRTA)

- 3.4.1.3 North Texas Tollway Authority (NTTA)

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 Autorita di Regolazione dei Trasporti (ART)

- 3.4.2.3 Highways England / National Highways

- 3.4.3 Asia Pacific

- 3.4.3.1 National Highways Authority of India (NHAI)

- 3.4.3.2 Ministry of Transport (MoT)

- 3.4.3.3 Land Transport Authority (LTA)

- 3.4.3.4 Australia’s Tolling Authorities

- 3.4.4 Latin America

- 3.4.4.1 Agencia Nacional de Transportes Terrestres (ANTT)

- 3.4.4.2 National Roads Directorate (DNV)

- 3.4.5 Middle East & Africa

- 3.4.5.1 South African National Roads Agency Limited (SANRAL)

- 3.4.5.2 Roads and Transport Authority (RTA)

- 3.4.5.3 Saudi Ministry of Transport & Logistic Services

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Interoperability and standardization landscape

- 3.11.1 Regional interoperability initiatives

- 3.11.2 Cross-border tolling challenges and solutions

- 3.11.3 Universal toll tag and multi-protocol compatibility

- 3.11.4 Harmonization efforts and future roadmap

- 3.12 Smart city integration and mobility-as-a-service

- 3.12.1 Tolling integration with urban mobility platforms

- 3.12.2. Connected vehicle ecosystem and V2 X communication

- 3.12.3 Seamless intermodal payment systems

- 3.12.4 Smart parking integration with toll accounts

- 3.13 Case studies

- 3.14 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Roadside Equipment (RSE)

- 5.2.2 On-Board Units (OBU)

- 5.2.3 Central & Network Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By System, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Automatic Vehicle Identification (AVI)

- 6.3 Automatic Vehicle Classification (AVC)

- 6.4 Violation Enforcement System (VES)

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Radio-Frequency Identification (RFID)

- 7.3 Dedicated Short-Range Communication (DSRC)

- 7.4 Global Navigation Satellite System (GNSS)/GPS

- 7.5 Video analytics/CCTV-based systems

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Tolling Method, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Automatic Tolling / Electronic Toll Collection (ETC)

- 8.3 Manual toll collection

- 8.4 Free-Flow / Open Road Tolling (ORT)

Chapter 9 Market Estimates & Forecast, By Payment Method, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Prepaid

- 9.3 Postpaid

- 9.4 Pay-By-Plate

Chapter 10 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 Passenger cars

- 10.2.1 Hatchback

- 10.2.2 Sedan

- 10.2.3 SUV

- 10.3 Commercial vehicles

- 10.3.1 LCV

- 10.3.2 MCV

- 10.3.3 HCV

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 Highways & Expressways

- 11.3 Urban tolling

- 11.4 Bridges & Tunnels

- 11.5 Parking & Access Control

Chapter 12 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 12.1 Key trends

- 12.2 Government / Public Sector

- 12.3 Private Sector

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 US

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.3.6 Russia

- 13.3.7 Nordics

- 13.3.8 Benelux

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 ANZ

- 13.4.6 Singapore

- 13.4.7 Malaysia

- 13.4.8 Indonesia

- 13.4.9 Vietnam

- 13.4.10 Thailand

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.5.4 Colombia

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global companies

- 14.1.1 Kapsch TrafficCom

- 14.1.2 Siemens

- 14.1.3 Thales

- 14.1.4 Conduent

- 14.1.5 ST Engineering (TransCore)

- 14.1.6 Cubic

- 14.1.7 EFKON

- 14.1.8 Neology

- 14.1.9 Toshiba

- 14.1.10 VINCI

- 14.1.11 Q-Free

- 14.1.12 AECOM

- 14.1.13 Mitsubishi

- 14.1.14 SICE

- 14.1.15 Indra Sistemas

- 14.2 Regional companies

- 14.2.1 Mundys

- 14.2.2 Autostrade per l'Italia

- 14.2.3 Brisa

- 14.2.4. ( Automatic systems) TollPlus

- 14.2.5 P Square Solutions

- 14.2.6 Perceptics

- 14.3 Emerging companies

- 14.3.1 BestPass

- 14.3.2 AEye

- 14.3.3 Star Systems International

- 14.3.4 Kistler