PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936604

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936604

Automotive Radar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

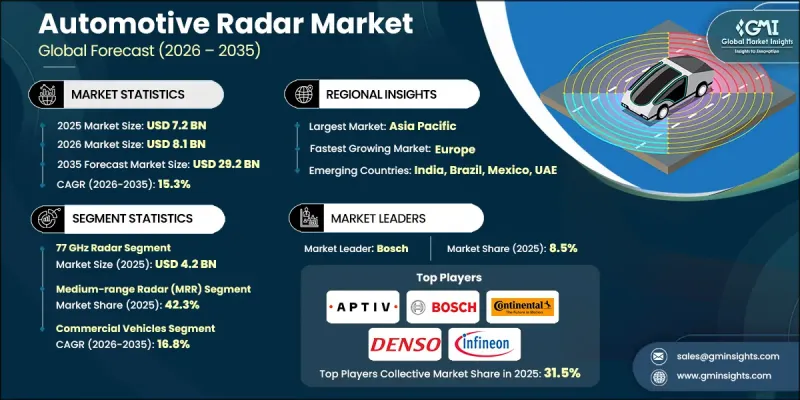

The Global Automotive Radar Market was valued at USD 7.2 billion in 2025 and is estimated to grow at a CAGR of 15.3% to reach USD 29.2 billion by 2035.

The rising adoption of advanced driver-assistance systems (ADAS) has significantly fueled the demand for automotive radars, as they serve as critical components within these systems. Increasing patent filings related to ADAS technologies further sustain the consistent need for radar solutions. The automotive sector is also experiencing growth in connected vehicles, which integrate multiple radar sensors to enhance safety and automation features. These radars support real-time AI and machine learning applications, enabling vehicles to make faster decisions, anticipate hazards, and optimize traffic handling. Short-range radar is gaining prominence in assisting parking, monitoring blind spots, and preventing low-speed collisions by accurately detecting nearby objects. Manufacturers are now combining these radars with cameras and ultrasonic sensors to improve precision, performance in adverse weather conditions, and cost efficiency for both commercial and passenger vehicles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.2 Billion |

| Forecast Value | $29.2 Billion |

| CAGR | 15.3% |

The 77 GHz radar segment accounted for USD 4.2 billion in 2025. Offering superior accuracy and detection range, 77 GHz radars are highly reliable for identifying vehicles, pedestrians, and obstacles at varying distances. Their capabilities are crucial for modern ADAS features, including adaptive cruise control, autonomous emergency braking, forward collision alerts, and blind-spot monitoring, which are increasingly mandated in several regions. Automotive companies are deploying multiple radar units throughout vehicles' front, rear, and corners, most of which rely on 77 GHz sensors due to their robustness and scalability.

The medium-range radar (MRR) held a 42.3% share in 2025 and is expected to reach USD 12.3 billion by 2035. MRR systems are essential for autonomous parking, urban collision prevention, and enabling a comprehensive awareness of the surrounding environment. As urban centers transition toward intelligent transportation systems, commercial fleets, ride-hailing services, and last-mile delivery vehicles are relying heavily on MRR for navigating high-traffic zones. The growth of smart transport initiatives and connected infrastructure is creating increasing demand for radar-based safety solutions in both commercial and passenger vehicles.

United States Automotive Radar Market reached USD 817.4 million in 2025. Commercial trucking fleets are increasingly integrating radar detection technologies to minimize highway accidents and enhance driver assistance during long-haul operations. These systems are also being installed in passenger vehicles to provide improved safety features such as blind-spot detection and lane departure alerts, driven by the presence of major domestic automakers producing high-tech vehicles.

Key players dominating the Global Automotive Radar Market include Bosch, Denso, Aptiv, Continental, Infineon, NXP Semiconductors, Analog Devices, ZF Friedrichshafen, Valeo, and Texas Instruments. Leading companies in the automotive radar market are adopting strategic measures to solidify their market presence. These include forging alliances and partnerships with automotive manufacturers to integrate radar technologies into new vehicles, expanding research and development for next-generation radar sensors, and investing in AI and machine learning capabilities to enhance real-time decision-making in vehicles. They are also focusing on regional expansion, acquiring smaller tech firms, and offering cost-effective, high-performance solutions for both commercial and passenger vehicles. By continuously innovating and diversifying product portfolios, these companies strengthen their foothold in the growing radar market while meeting evolving regulatory and technological demands.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Frequency

- 2.2.3 Range

- 2.2.4 Placement

- 2.2.5 Vehicle

- 2.2.6 Vehicle Class

- 2.2.7 Propulsion

- 2.2.8 Application

- 2.2.9 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of advanced driver assistance systems (ADAS)

- 3.2.1.2 Growing demand for autonomous and semi-autonomous vehicles

- 3.2.1.3 Increasing focus on collision avoidance and road safety

- 3.2.1.4 Expansion of electric and software-defined vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of automotive radar systems and integration

- 3.2.2.2 Complexity in signal processing and calibration

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of level 2+ and level 3 autonomous driving functions

- 3.2.3.2 Increasing adoption in commercial vehicles and fleet safety

- 3.2.3.3 Rapid growth of automotive radar in emerging markets

- 3.2.3.4 Demand for short-range radar in parking and blind spot applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Communications Commission (FCC)

- 3.4.1.2 American National Standards Institute (ANSI)

- 3.4.1.3 Society of Automotive Engineers (SAE)

- 3.4.2 Europe

- 3.4.2.1 European Telecommunications Standards Institute (ETSI)

- 3.4.2.2 United Nations Economic Commission for Europe

- 3.4.2.3 European Committee for Electrotechnical Standardization

- 3.4.3 Asia Pacific

- 3.4.3.1 Vehicle Network Communication Protocol (China)

- 3.4.3.2 Association of Radio Industries and Businesses

- 3.4.3.3 Ministry of Internal Affairs and Communications (MIC)

- 3.4.4 Latin America

- 3.4.4.1 Agencia Nacional de Telecomunicacoes (ANATEL)

- 3.4.4.2 Comision de Regulacion de Comunicaciones

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council regulatory framework

- 3.4.5.2 National Communications Authority (UAE)

- 3.4.5.3 Vehicle regulations for safety systems

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact

- 3.11.1 Environmental impact assessment

- 3.11.2 Social impact & community benefits

- 3.11.3 Governance & corporate responsibility

- 3.11.4 Sustainable finance & investment trends

- 3.12 Cybersecurity and functional safety framework

- 3.12.1 Cybersecurity threats and vulnerability assessment

- 3.12.2 Over-the-air (OTA) update security protocols

- 3.12.3 Redundancy and fail-safe mechanism design

- 3.12.4 Data privacy and protection in radar sensing

- 3.13 Installation, calibration, and maintenance ecosystem

- 3.13.1 Factory calibration vs. field calibration requirements

- 3.13.2 Aftermarket installation complexity

- 3.13.3 Recalibration needs after collision repair

- 3.13.4 Diagnostic tools and equipment requirements

- 3.14 Semiconductor & Chipset Ecosystem Analysis

- 3.15 ADAS & Autonomy Roadmap Mapping

- 3.16 OEM Radar Strategy & Sourcing Models

- 3.17 Case studies

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Frequency, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 24 GHz Radar

- 5.3 77 GHz Radar

- 5.4 79 GHz Radar

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Range, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Short-Range Radar (SRR)

- 6.3 Medium-Range Radar (MRR)

- 6.4 Long-Range Radar (LRR)

Chapter 7 Market Estimates & Forecast, By Placement, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Exterior

- 7.2.1 Front Radar

- 7.2.2 Rear Radar

- 7.2.3 Side Radar

- 7.3 Interior

- 7.3.1 Driver Monitoring Radar

- 7.3.2 Occupant Monitoring Radar

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 SUV

- 8.2.3 Sedan

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCV)

- 8.3.2 Medium Commercial Vehicles (MCV)

- 8.3.3 Heavy Commercial Vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Vehicle Class, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Economy (Below USD 25,000)

- 9.3 Mid-Range (USD 25,000 - USD 50,000)

- 9.4 Premium/Luxury (Above USD 50,000)

Chapter 10 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 ICE

- 10.3 EV

- 10.3.1 BEV

- 10.3.2 HEV

- 10.3.3 PHEV

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 Adaptive Cruise Control (ACC)

- 11.3 Blind Spot Detection (BSD)

- 11.4 Forward Collision Warning (FCW)

- 11.5 Lane Departure Warning System (LDWS)

- 11.6 Automatic Emergency Braking (AEB)

- 11.7 Parking Assistance (PA)

- 11.8 Others

Chapter 12 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 12.1 Key trends

- 12.2 OEM

- 12.3 Aftermarket

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 US

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.3.6 Russia

- 13.3.7 Nordics

- 13.3.8 Benelux

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 ANZ

- 13.4.6 Singapore

- 13.4.7 Malaysia

- 13.4.8 Indonesia

- 13.4.9 Vietnam

- 13.4.10 Thailand

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.5.4 Colombia

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global companies

- 14.1.1 Robert Bosch

- 14.1.2 Continental

- 14.1.3 Denso

- 14.1.4 Aptiv

- 14.1.5 NXP Semiconductors

- 14.1.6 ZF Friedrichshafen

- 14.1.7 Valeo

- 14.1.8 Magna

- 14.1.9 Infineon

- 14.1.10 Texas Instruments

- 14.1.11 Autoliv

- 14.1.12 Analog Devices

- 14.1.13 Renesas Electronics

- 14.1.14 BorgWarner

- 14.1.15 Hyundai Mobis

- 14.1.16 Mobileye

- 14.2 Regional companies

- 14.2.1 Huawei Technologies

- 14.2.2 Cheng-Tech

- 14.2.3 HASCO

- 14.2.4 HiRain Technologies

- 14.2.5 Calterah Semiconductor

- 14.2.6 HL Klemove

- 14.2.7 Desay SV Automotive

- 14.2.8 WeiFu

- 14.2.9 Fusionride

- 14.3 Emerging companies

- 14.3.1 Uhnder

- 14.3.2 Zendar

- 14.3.3 Waveye

- 14.3.4 Altos Radar

- 14.3.5 Xavveo