PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936629

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936629

Wire and Cable Polymer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

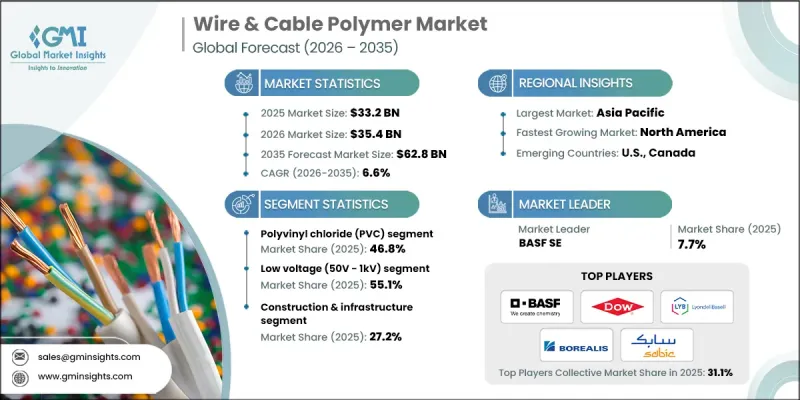

The Global Wire and Cable Polymer Market was valued at USD 33.2 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 62.8 billion by 2035.

The market is experiencing robust growth due to rising demand across sectors such as construction, automotive, telecommunications, and energy. A key trend in the market is the shift from conventional polymer materials to advanced high-performance polymers, including cross-linked polyethylene (XLPE), thermoplastic elastomers (TPE), and flame-retardant plastics, which offer superior durability, flexibility, and safety. These modern polymers are increasingly preferred because of their excellent electrical insulation, resistance to environmental stress, and capacity to prevent short circuits and power loss. Their applications are widespread: in construction for power and wiring systems, in automotive for wiring harnesses and electronic components, in telecommunications for fiber optic cables, and in renewable energy for solar and wind power cabling. Key benefits such as chemical resistance, lightweight design, ease of processing, and long-term reliability continue to drive polymer adoption in wire and cable applications worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $33.2 Billion |

| Forecast Value | $62.8 Billion |

| CAGR | 6.6% |

The low voltage cables (50V-1kV) segment held 55.1% share and is expected to grow at a CAGR of 6.8% from 2026 to 2035. This segment is widely used in residential and commercial applications and has been propelled by urbanization, smart building developments, and the increasing integration of energy-efficient wiring solutions. Investments by governments and private enterprises in smart grid modernization and renewable energy integration have further accelerated demand for durable, high-performance polymers in low-voltage cabling while emphasizing safety, reliability, and environmental sustainability.

The construction and infrastructure sector accounted for 27.2% share in 2025 and is anticipated to grow at a CAGR of 6.9% through 2035. Urbanization, smart city projects, and large-scale infrastructure development continue to drive the need for robust, long-lasting wiring systems. Additionally, the growth of renewable energy projects, such as solar and wind power, has increased demand for polymer cables with higher thermal stability, superior insulation, and enhanced durability to withstand harsh environmental conditions and ensure reliable power transmission.

North America Wire and Cable Polymer Market accounted for 15.1% share in 2025. The region's expansion is fueled by infrastructural modernization, renewable energy investments, and the growth of the telecommunications sector. Rising adoption of electric vehicles and smart grid initiatives has created increasing demand for high-performance polymers that combine excellent insulation, fire resistance, and flexibility. Strict safety and environmental regulations in the region are encouraging manufacturers to develop eco-friendly, flame-retardant polymer cables, aligning product innovation with sustainability and regulatory compliance.

Major companies in the Global Wire and Cable Polymer Market include Dow Inc., Arkema SA, LG Chem Ltd, ExxonMobil Corporation, Borealis AG, LyondellBasell Industries N.V., Solvay SA, Mitsui Chemicals, Inc., Eastman Chemical Company, BASF SE, Sumitomo Chemical Co., Ltd., and SABIC. Leading players in the wire and cable polymer market are adopting several strategies to strengthen their presence and expand market share. They are investing heavily in research and development to create high-performance, eco-friendly polymers with superior insulation, fire resistance, and mechanical properties. Strategic partnerships with manufacturers, construction companies, and energy providers help ensure a consistent supply and market penetration. Companies are also focusing on product diversification to meet the needs of low-, medium-, and high-voltage applications across various industries. Expansion into emerging markets and regional production facilities reduces lead times and cost, while sustainability initiatives, such as biodegradable and flame-retardant polymers, help align with regulatory standards and growing consumer demand for safe, environmentally responsible materials.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Polymer type

- 2.2.3 Voltage

- 2.2.4 End-user industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Polymer Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene

- 5.2.1 Low Density Polyethylene (LDPE)

- 5.2.2 High Density Polyethylene (HDPE)

- 5.2.3 Linear Low Density Polyethylene (LLDPE)

- 5.3 Polypropylene

- 5.4 Polyvinyl Chloride (PVC)

- 5.4.1 Flexible PVC

- 5.4.2 Rigid PVC

- 5.5 Elastomers

- 5.5.1 Ethylene Propylene Rubber (EPR)

- 5.5.2 Ethylene Propylene Diene Monomer (EPDM)

- 5.5.3 Silicone Rubber

- 5.5.4 Thermoplastic Elastomers (TPE)

- 5.5.5 Thermoplastic Polyurethane (TPU)

- 5.6 Fluoropolymers

- 5.6.1 Polytetrafluoroethylene (PTFE)

- 5.6.2 Fluorinated Ethylene Propylene (FEP)

- 5.6.3 Perfluoroalkoxy (PFA)

- 5.6.4 Ethylene Tetrafluoroethylene (ETFE)

- 5.7 High-Performance Polymers

- 5.7.1 Polyether Ether Ketone (PEEK)

- 5.7.2 Polyetherimide (PEI)

- 5.7.3 Polyphenylene Sulfide (PPS)

- 5.8 Halogen-Free Flame Retardant (HFFR) Compounds

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Voltage, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Low voltage (50V - 1kV)

- 6.3 Medium voltage (1kV - 35kV)

- 6.4 High voltage (35kV - 150kV)

Chapter 7 Market Estimates and Forecast, By End-User Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Power generation

- 7.3 Telecommunications

- 7.4 Automotive & transportation

- 7.5 Construction & infrastructure

- 7.6 Industrial manufacturing

- 7.7 Oil & gas

- 7.8 Mining & resources

- 7.9 Renewable energy

- 7.10 Data centers & IT

- 7.11 Aerospace & defense

- 7.12 Healthcare

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Arkema SA

- 9.2 BASF SE

- 9.3 Borealis AG

- 9.4 Dow Inc.

- 9.5 Eastman Chemical Company

- 9.6 ExxonMobil Corporation

- 9.7 LG Chem Ltd

- 9.8 LyondellBasell Industries N.V.

- 9.9 Mitsui Chemicals, Inc.

- 9.10 SABIC

- 9.11 Solvay SA

- 9.12 Sumitomo Chemical Co., Ltd.