PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936647

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936647

Powered Mobility Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

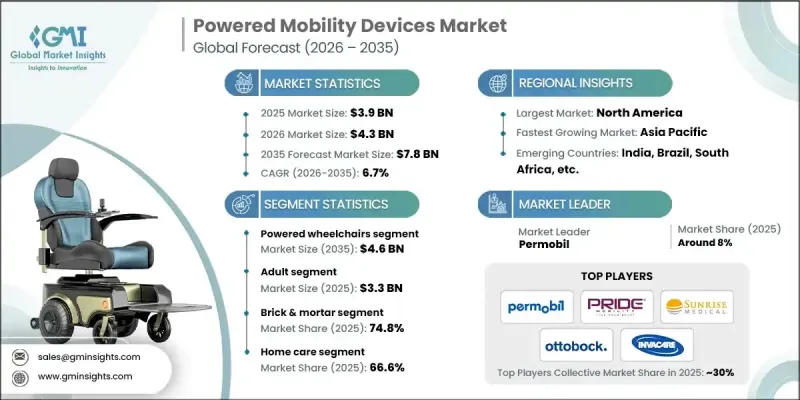

The Global Powered Mobility Devices Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a 6.7% CAGR to reach USD 7.8 billion by 2035.

Market growth is supported by the rising prevalence of mobility-impairing conditions and the expanding elderly population that increasingly depends on powered assistance to preserve independence and day-to-day function. Unlike basic mobility aids, powered mobility devices are moving quickly into the smart medical device lane, as manufacturers integrate longer-range battery systems, more efficient motors, ergonomic seating systems, and programmable controls that improve comfort and reduce caregiver strain. The market's momentum is also reinforced by the broader shift toward home-based care, where patients and families prefer practical mobility solutions that support aging-in-place, reduce repeated facility visits, and enable safer indoor/outdoor navigation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 6.7% |

From a product and adoption perspective, the market is benefiting from demand across a wide severity range, from users who need full-time powered support to those who want a boost through add-on units. Clinical need is rising with chronic conditions such as arthritis, post-stroke impairments, spinal cord injuries, and neurodegenerative disorders, which often require long-term, reliable mobility assistance rather than short-duration rehabilitation support. Technology is also helping unlock demand: modern devices increasingly emphasize lightweight materials, better maneuverability, intelligent braking, improved seating customization, and safety-oriented features that reduce falls and enhance stability, making powered mobility devices more acceptable for everyday use, not only in institutional settings.

The powered wheelchairs segment generated USD 4.6 billion in 2025, as it remains the preferred solution for users with severe or progressive mobility limitations who need advanced control options, stronger postural support, and consistent performance across indoor and outdoor environments. These products are increasingly differentiated by drive options, seating modules, and safety systems, and they are gaining further traction as more care pathways move into the home, where comfort, reliability, and customization matter as much as clinical specifications.

The home care segment held 66.6% share in 2025, driven by aging-in-place preferences, growing chronic disease prevalence, and the need for convenient mobility within residential environments where daily routine, safety, and independence are the non-negotiables. Home care demand is also supported by improvements in device usability, such as compact footprints, improved turning radius for indoor navigation, smarter controls, and easier charging, while service models (delivery, installation, maintenance) help reduce barriers for older adults and caregivers who want a low-friction ownership experience.

North America Powered Mobility Devices Market held 41.3% share in 2025, anchored by stronger healthcare infrastructure, higher diagnosis and treatment rates for mobility-impairing conditions, and relatively better access through reimbursement pathways and established rehabilitation/home-care ecosystems. The region's market strength is also reinforced by faster adoption of technology-forward devices that emphasize safety, connectivity, and comfort features that resonate strongly with both clinicians and consumers who expect measurable improvements in daily functioning and quality of life.

Key players involved in the Global Powered Mobility Devices Market include Airwheel, Callidai Motor Works, Decon, Drive DeVilbiss Healthcare, Frido, Golden Technologies, INVACARE, Karman Healthcare, LEVO, Merits Health Products, MEYRA, Ostrich Mobility Instruments, Ottobock, Permobil, Pride Mobility, Sunrise Medical. Companies are strengthening their market foothold by accelerating product innovation, lightweight/foldable designs, improved battery performance, and smarter controls that enhance safety and comfort for home use. They are also widening access through multi-channel distribution, combining clinician-led brick-and-mortar fitting and service with faster-growing online models that improve reach into underserved geographies. To improve conversion and retention, leading players bundle devices with after-sales maintenance, training, and customization (seating, controls, accessories), reducing user anxiety and improving long-term satisfaction.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Patient trends

- 2.2.4 Distribution channel trends

- 2.2.5 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of neurological diseases

- 3.2.1.2 Technological advancements in powered mobility products

- 3.2.1.3 Rising percentage of geriatric population

- 3.2.1.4 Increasing prevalence of disabilities worldwide

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of powered wheelchairs

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Opportunities

- 3.2.3.1 Focus on lightweight and foldable electric wheelchairs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Value chain analysis

- 3.7 Reimbursement scenario

- 3.8 Consumer behavior and trends

- 3.9 Pricing analysis, by product type, 2025

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Powered wheelchairs

- 5.2.1 Rear-wheel drive wheelchairs

- 5.2.2 Mid-wheel drive wheelchairs

- 5.2.3 Front-wheel drive wheelchairs

- 5.2.4 Combination-drive wheelchairs

- 5.3 Power mobility scooters

- 5.3.1 3-wheel devices

- 5.3.2 4-wheel devices

- 5.4 Power add-on or propulsion-assist units

Chapter 6 Market Estimates and Forecast, By Patient, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Brick & mortar

- 7.3 Online channel

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Home care

- 8.3 Rehabilitation centers

- 8.4 Hospitals

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Airwheel

- 10.2 Callidai Motor Works

- 10.3 Decon

- 10.4 DriveDeVilbiss Healthcare

- 10.5 Frido

- 10.6 Golden Technologies

- 10.7 INVACARE

- 10.8 Karman Healthcare

- 10.9 LEVO

- 10.10 Merits Health Products

- 10.11 MEYRA

- 10.12 Ostrich Mobility Instruments

- 10.13 Ottobock

- 10.14 Permobil

- 10.15 Pride Mobility

- 10.16 Sunrise medical