PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936649

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936649

Metal Injection Molding (MIM) Parts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

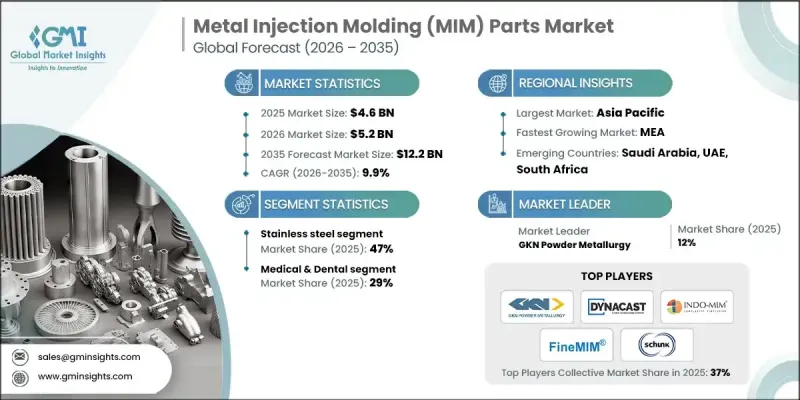

The Global Metal Injection Molding (MIM) Parts Market was valued at USD 4.6 billion in 2025 and is estimated to grow at a CAGR of 9.9% to reach USD 12.2 billion by 2035.

The market is gaining momentum as designers increasingly seek to integrate complex, miniaturized metal components into modern products. More original equipment manufacturers (OEMs) are choosing MIM to produce parts that are too small, intricate, or delicate for conventional machining or casting processes. MIM is particularly suited to sectors requiring high levels of miniaturization and precision, including medical, dental, aerospace, and consumer electronics. Stainless steel, titanium, and specialty magnetic alloys are increasingly used to manufacture lightweight, functional, and biocompatible components. Advanced CAD modeling, topology optimization, and digital process simulation are being leveraged to improve part design, shrinkage control, density distribution, and flow characteristics, enabling first-time-right production, especially for safety-critical automotive and aerospace components. The combination of precision, repeatability, and design flexibility is solidifying MIM's adoption across multiple high-growth industries worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.6 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 9.9% |

The stainless steel segment held 47% share and is expected to grow at a CAGR of 7.1% through 2035. Stainless steel and low-alloy steel dominate the market due to extensive applications in automotive, industrial, and hardware segments. Titanium and biocompatible stainless steel are gaining traction in medical and dental applications, while copper and magnetic alloys are increasingly used in sensors, actuators, and electrical connectivity applications. These material trends reflect the growing demand for durable, lightweight, and high-performance components across a wide range of industries, highlighting the versatility of MIM as a production technology.

The medical and dental sector accounted for 29% share in 2025 and is projected to grow at a CAGR of 9.8% during 2026-2035. The primary driver for MIM adoption in these segments is the demand for small, precise, and geometrically complex components. In medical and dental applications, stainless steel and titanium MIM parts are extensively used for implants, surgical instruments, and biocompatible components. Consumer electronics also drive demand for miniature MIM components that require both robustness and aesthetic finishes. The ability of MIM to produce intricate designs that are lightweight, functional, and repeatable is a key reason for its rising adoption in sectors where precision and performance are critical.

North America Metal Injection Molding (MIM) Parts Market reached USD 1.2 billion in 2025. Growth is primarily driven by high-value applications in medical, firearms, and automotive sectors. The region benefits from advanced design capabilities, rigorous quality standards, and early adoption of MIM technology in regulated industries. The United States remains the core market in North America, supported by diverse demand from medical devices, aerospace, defense, consumer electronics, and performance automotive sectors. The presence of advanced contract manufacturers and the focus on high-precision, high-volume production foster ongoing innovation in materials, tooling, and MIM processes.

Major players operating in the Global Metal Injection Molding (MIM) Parts Market include Dynacast, Akron Porcelain & Plastics Co., Rockleigh Industries, Smith Metal Products, Advanced Materials Technologies Pte. Ltd., MPP (Metal Powder Products), FineMIM, CMG Technologies, GKN Powder Metallurgy, Hamamatsu Metal Works Co., Ltd., Zcmim (Zhejiang Yibo Technology), Epson Atmix Corporation, OptiMIM, Parmaco Metal Injection Molding, Injectamax International LLC, ARC Group Worldwide, Inc., ASH Industries, Form Technologies Company (Dynacast), INDO-MIM, and Schunk Group. Companies in the metal injection molding parts market are pursuing several strategies to strengthen their market presence and expand global reach. They are investing heavily in research and development to optimize MIM processes, improve material performance, and develop innovative lightweight and biocompatible components. Strategic partnerships with OEMs, aerospace firms, medical device manufacturers, and electronics companies are being formed to secure long-term contracts and access to emerging high-value markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material type

- 2.2.3 End-Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Miniaturization of medical and electronic devices

- 3.2.1.2 Automotive light-weighting and efficiency requirements

- 3.2.1.3 Design freedom and material utilization benefits

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High tooling and upfront development costs

- 3.2.2.2 Process complexity and qualification timelines

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in implants, surgical and dental devices

- 3.2.3.2 Rising adoption in wearables and smart hardware

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By material type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022-2035 (USD Billion) (Mn Units)

- 5.1 Key trends

- 5.2 Stainless steel

- 5.3 Low alloy steel

- 5.4 Molybdenum alloys

- 5.5 Titanium

- 5.6 Magnetic materials

- 5.7 Copper & copper alloys

- 5.8 Others (tungsten, cobalt alloys)

Chapter 6 Market Estimates and Forecast, By End-User, 2022-2035 (USD Billion) (Mn Units)

- 6.1 Key trends

- 6.2 Medical & dental

- 6.2.1 Surgical instruments

- 6.2.2 Orthodontic brackets

- 6.2.3 Dental implants

- 6.2.4 Others

- 6.3 Automotive

- 6.3.1 Turbocharger components

- 6.3.2 Fuel system parts

- 6.3.3 Transmission parts

- 6.3.4 Others

- 6.4 Consumer electronics

- 6.4.1 Smartphone hinges

- 6.4.2 Wearable device components

- 6.4.3 Others

- 6.5 Aerospace & defense

- 6.5.1 Engine components

- 6.5.2 Missile guidance parts

- 6.6 Industrial

- 6.6.1 Valve parts

- 6.6.2 Hydraulic component

- 6.6.3 Others

- 6.7 Firearms

- 6.7.1 Triggers

- 6.7.2 Sights

- 6.8 Others (recreation, IT etc.)

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Mn Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Smith Metal Products

- 8.2 Advanced Materials Technologies Pte. Ltd

- 8.3 CMG Technologies

- 8.4 Form Technologies Company (Dynacast)

- 8.5 ARC Group Worldwide, Inc.

- 8.6 Akron Porcelain & Plastics Co.

- 8.7 Dynacast

- 8.8 Nippon Piston Ring Co. Ltd.

- 8.9 INDO-MIM

- 8.10 ASH Industries

- 8.11 Hamamatsu Metal Works Co., Ltd.

- 8.12 Parmaco Metal Injection Molding

- 8.13 GKN Powder Metallurgy

- 8.14 MPP (Metal Powder Products)

- 8.15 Zcmim (Zhejiang Yibo Technology)

- 8.16 Epson Atmix Corporation

- 8.17 Schunk Group

- 8.18 FineMIM

- 8.19 OptiMIM

- 8.20 Advanced Power Products

- 8.21 Rockleigh Industries

- 8.22 Injectamax International, LLC