PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936672

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936672

Blood and Blood Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

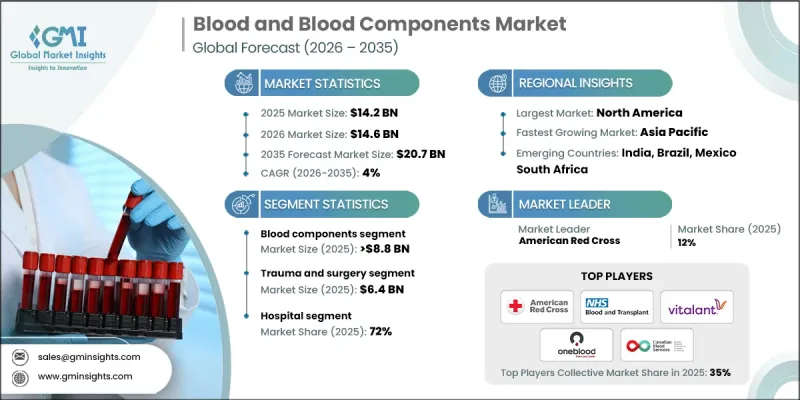

The Global Blood and Blood Components Market was valued at USD 14.2 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 20.7 billion by 2035.

The market is experiencing steady growth due to the rising number of surgical procedures worldwide, the increasing prevalence of long-term medical conditions, and the expanding use of plasma-based therapies across a wide range of clinical treatments. Continuous awareness initiatives and donation drives conducted by blood collection organizations are supporting a stable supply pipeline. Blood and blood components remain essential to modern healthcare systems, as they ensure uninterrupted access to red blood cells, plasma, and platelets required for transfusion-based therapies. These products are widely used across emergency care, surgical interventions, oncology treatments, and the long-term management of blood-related disorders. The market operates under strict quality and safety frameworks to maintain product integrity and patient safety. Ongoing innovation in blood collection methods, component separation, testing, storage, and logistics is improving efficiency and meeting the rising demands of global healthcare systems. The industry continues to evolve with a strong focus on reliability, traceability, and regulatory compliance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.2 Billion |

| Forecast Value | $20.7 Billion |

| CAGR | 4% |

The blood components segment generated USD 8.8 billion in 2025. This segment includes red blood cells, plasma, platelets, and white blood cells, each fulfilling specialized therapeutic roles. Red blood cells remain in high demand due to their essential function in restoring oxygen delivery in patients with reduced hemoglobin levels. The global burden of blood-related conditions continues to support sustained utilization of component-based therapies, making this segment a core revenue contributor.

The hospitals segment accounted for 72% share in 2025. Healthcare facilities remain the primary consumers of blood and blood components due to their central role in managing emergency care, surgical procedures, oncology services, and chronic disease treatment. The growing volume of complex medical interventions, combined with increasing trauma cases and advanced treatment protocols, continues to drive consistent demand from hospitals, reinforcing their dominance as end users.

North America Blood and Blood Components Market held a 39.8% share in 2025. The region benefits from a well-established healthcare infrastructure, strong donor participation, and high utilization of transfusion therapies across multiple clinical applications. Advanced medical practices, efficient blood management systems, and strong institutional frameworks continue to support regional market leadership.

Key organizations operating in the Global Blood and Blood Components Market include Vitalant, Canada Blood Services, American Red Cross, OneBlood, NHS Blood and Transplant, ImpactLife, America's Blood Centers, Versiti, Bloodworks Northwest, Carter BloodCare, Indian Red Cross Society, Associazione Volontari Italiani del Sangue, Northern Ireland Blood Transfusion Service, Scottish National Blood Transfusion Service, and the Welsh Blood Service. Companies in the blood and blood components market are strengthening their market position by expanding donor networks, improving collection efficiency, and investing in advanced processing and storage technologies. Organizations are focusing on digital donor engagement platforms to improve donor retention and streamline appointment scheduling. Strategic collaborations with hospitals and healthcare systems are enhancing supply reliability and demand forecasting.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing volume of surgeries globally

- 3.2.1.2 Rising number of people suffering from chronic conditions including cancer

- 3.2.1.3 Growing popularity of plasma therapy to treat various sport injuries, cosmetic as well as orthopedic procedures

- 3.2.1.4 Several blood donation campaigns undertaken by various blood organizations

- 3.2.2 Industry Pitfalls and Challenges:

- 3.2.2.1 Short shelf life of blood components

- 3.2.2.2 Transfusion transmitted infection (TTI) related to donated blood

- 3.2.3 Market Opportunities

- 3.2.3.1 Growth in personalized and targeted therapies

- 3.2.3.2 Integration of digital solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Whole blood

- 5.3 Blood components

- 5.3.1 Red blood cells

- 5.3.2 Platelets

- 5.3.3 Plasma

- 5.3.4 White blood cells

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Trauma and Surgery

- 6.3 Blood disorders

- 6.3.1 Anaemia

- 6.3.2 Bleeding disorders

- 6.3.2.1 Hemophilia

- 6.3.2.2 Von willebrand disease

- 6.3.3 Other blood disorders

- 6.4 Cancer treatment

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 American Red Cross

- 9.2 America's Blood Centers

- 9.3 Associazione Volontari Italiani del Sangue (AVIS)

- 9.4 Bloodworks Northwest

- 9.5 Canada Blood Services

- 9.6 Carter BloodCare

- 9.7 ImpactLife

- 9.8 Indian Red Cross Society

- 9.9 NHS Blood and Transplant (NHSBT)

- 9.10 Northern Ireland Blood Transfusion Service

- 9.11 OneBlood

- 9.12 Scottish National Blood Transfusion Service (NHS National Services Scotland)

- 9.13 Versiti

- 9.14 Vitalant

- 9.15 Welsh blood service