PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959270

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959270

Fiber Ingredients for Sugar Reduction Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

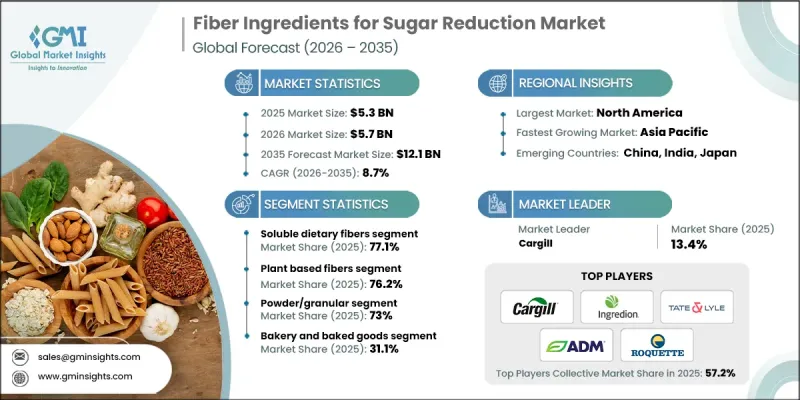

The Global Fiber Ingredients for Sugar Reduction Market was valued at USD 5.3 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 12.1 billion by 2035.

Market growth is driven by a strong global shift toward healthier eating habits and rising awareness of the negative effects of excess sugar consumption. Consumers are increasingly seeking products that deliver sweetness and texture without compromising nutritional value. Fiber-based ingredients are gaining widespread adoption as effective sugar-reduction solutions because they enhance mouthfeel, balance sweetness perception, and improve overall sensory quality while contributing minimal calories and low glycemic impact. These ingredients also support the development of functional food products aligned with digestive wellness, metabolic balance, and weight management goals. Their ability to deliver clean-label formulations without artificial sweeteners makes them particularly attractive to food and beverage manufacturers. Growing regulatory pressure to reduce sugar levels in packaged foods is further accelerating demand, while continuous formulation innovation is expanding application potential across a broad range of product categories.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.3 Billion |

| Forecast Value | $12.1 Billion |

| CAGR | 8.7% |

The soluble dietary fibers segment accounted for 77.1% share in 2025 and is expected to grow at a CAGR of 8.7% through 2035. Demand for this segment is supported by increasing consumer focus on wellness-oriented nutrition and preventive health. Soluble fibers are widely incorporated into functional foods, beverages, and nutrition-focused formulations due to their role in supporting cholesterol management, blood sugar regulation, and digestive balance. Their functional versatility and compatibility with diverse formulations continue to drive strong adoption across the industry.

The plant-based fibers segment held a 76.2% share in 2025 and is forecast to grow at a CAGR of 8.8% from 2026 to 2035. Market leadership is sustained by the broad availability and functionality of fibers sourced from grains, legumes, fruits, and root crops. Demand is rising for fibers that deliver both nutritional and sensory benefits, particularly those offering prebiotic functionality and naturally derived sweetness. This diversity of plant-based sources enables manufacturers to address varying formulation needs while meeting consumer expectations for natural and recognizable ingredients.

North America Fiber Ingredients for Sugar Reduction Market held 36% share in 2025. High consumer awareness around nutrition, coupled with a strong functional food and beverage sector, supports regional expansion. Advanced processing capabilities and continuous product innovation further strengthen market development across the United States and Canada.

Key companies operating in the Global Fiber Ingredients for Sugar Reduction Market include Tate & Lyle, ADM, Ingredion, Cargill, BENEO, Roquette, Kerry Group, Nexira, Sensus, and BioNeutra. Companies in the fiber ingredients for sugar reduction market are strengthening their market foothold through sustained investment in research and development aimed at improving taste, texture, and formulation performance. Many players are expanding their portfolios with clean-label and multifunctional fiber solutions to meet evolving consumer and regulatory demands. Strategic collaborations with food and beverage manufacturers are being used to accelerate innovation and application development. Capacity expansion, supply chain optimization, and sourcing transparency are also key priorities. Firms are increasingly focusing on sustainability initiatives and regulatory compliance to enhance brand trust, while geographic expansion into high-growth regions supports long-term competitive positioning.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fiber type

- 2.2.3 Sources

- 2.2.4 Form

- 2.2.5 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Fiber Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Soluble dietary fibers

- 5.3 Insoluble dietary fibers

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Plant-based fibers

- 6.2.1 Cereal-derived fibers

- 6.2.2 Legume-derived fibers

- 6.2.3 Root & tuber-derived fibers

- 6.2.4 Fruit-derived fibers

- 6.2.5 Others

- 6.3 Synthetic/modified fibers

- 6.3.1 Polydextrose

- 6.3.2 Resistant maltodextrin

- 6.4 Enzymatically-produced fibers

- 6.4.1 Galactooligosaccharides (GOS)

- 6.4.2 Fructooligosaccharides (FOS)

- 6.4.3 Others

Chapter 7 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Powder/granular

- 7.3 Liquid/syrup

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Bakery & baked goods

- 8.2.1 Breads & rolls

- 8.2.2 Cakes & pastries

- 8.2.3 Cookies & biscuits

- 8.2.4 Cereal bars & snack bars

- 8.3 Beverages

- 8.4 Dairy & frozen desserts

- 8.5 Confectionery

- 8.5.1 Chocolate & chocolate confectionery

- 8.5.2 Sugar confectionery & gummies

- 8.6 Specialized nutrition

- 8.6.1 Dietary supplements

- 8.6.2 Medical nutrition

- 8.6.3 Sports nutrition

- 8.6.4 Weight management products

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 ADM

- 10.2 BENEO

- 10.3 BioNeutra

- 10.4 Cargill

- 10.5 Ingredion

- 10.6 Kerry Group

- 10.7 Nexira

- 10.8 Roquette

- 10.9 Sensus

- 10.10 Tate & Lyle