PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959274

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959274

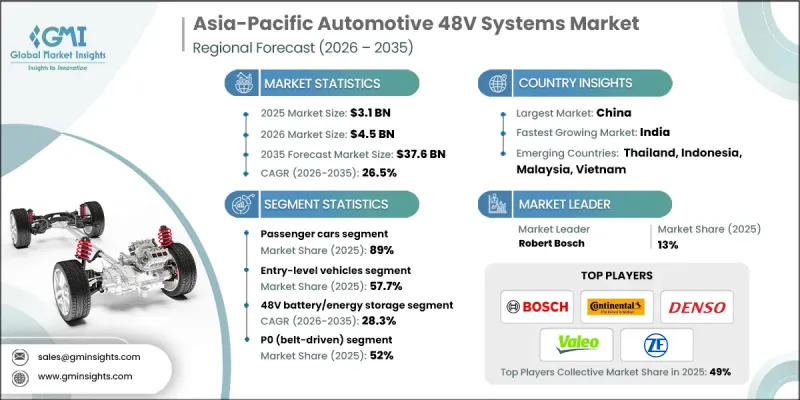

Asia-Pacific Automotive 48V Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

Asia-Pacific Automotive 48V Systems Market was valued at USD 3.1 billion in 2025 and is estimated to grow at a CAGR of 26.5% to reach USD 37.6 billion by 2035.

Market growth is driven by accelerated vehicle electrification efforts and increasingly strict emission reduction targets across the region. Regulatory pressure to lower carbon output is pushing automakers toward 48V mild-hybrid architectures as a balanced solution that improves efficiency without the cost burden of full electrification. Rapid urbanization, evolving mobility needs, and structural changes in vehicle electrical systems are reshaping how manufacturers design next-generation platforms. Automakers are actively reengineering vehicle power distribution to support higher electrical loads while maintaining affordability. The regional shift toward advanced vehicle electronics, combined with regulatory alignment with global climate commitments, is fundamentally transforming automotive electrical architectures. As production volumes rise and technology matures, 48V systems are becoming a mainstream feature rather than a premium addition. This transformation is positioning Asia-Pacific as the fastest-growing regional market, supported by strong policy frameworks, manufacturing scale, and continuous innovation across the automotive value chain.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Billion |

| Forecast Value | $37.6 Billion |

| CAGR | 26.5% |

Regulatory intensity across Asia-Pacific continues to accelerate the adoption of 48V technology. Fleet efficiency mandates and tightening fuel consumption thresholds are compelling manufacturers to deploy mild-hybrid systems at scale. Rising integration of electronically powered vehicle functions is placing increased demand on electrical architectures, with average system loads expanding significantly. As adoption of advanced electronic features rises from 18% in 2024 to an expected 68% by 2035, traditional electrical platforms are reaching functional limits, reinforcing the transition toward higher-voltage systems.

The passenger vehicles segment accounted for 89% share in 2025 and is forecast to grow at a CAGR of 26.8% through 2035. This dominance reflects widespread integration of 48V systems in everyday vehicles to improve fuel efficiency, enhance driving smoothness, and reduce mechanical stress, aligning well with consumer demand for comfort and sustainability.

The entry-level vehicles segment held a 57.7% share in 2025 and will grow at a CAGR of 25.4% through 2035. Automakers are embedding 48V systems into cost-sensitive models to meet emissions standards while preserving competitive pricing. The mid-premium segment continues to grow steadily as buyers seek a balance of performance, efficiency, and comfort supported by mild-hybrid functionality.

China Automotive 48V Systems Market generated USD 1.3 billion in 2025 and is expected to grow at a CAGR of 26.7% from 2026 to 2035. The country remains the world's largest automotive market, recording 26 million vehicle sales in 2024. Strong policy backing for electrification and targeted industrial programs are reinforcing domestic supply chains and accelerating large-scale deployment of 48V technologies.

Key companies operating in the Asia-Pacific Automotive 48V Systems Market include Robert Bosch, Denso, Continental, ZF Friedrichshafen, Valeo, BorgWarner, Infineon Technologies, Aptiv, Magna International, and Mitsubishi Electric. Companies active in the Asia-Pacific Automotive 48V Systems Market are strengthening their competitive position through aggressive localization strategies and platform-level integration. Manufacturers are investing heavily in scalable 48V architectures that can be deployed across multiple vehicle segments. Strategic partnerships with regional automakers and suppliers are helping reduce production costs and accelerate adoption. Firms are also expanding regional manufacturing capacity to support high-volume demand and ensure supply chain resilience. Continuous investment in power electronics, energy management software, and system optimization is enabling differentiation. Additionally, companies are aligning product roadmaps with regulatory timelines, allowing faster market entry and long-term contracts with major OEMs across the region.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 System Architecture

- 2.2.4 Vehicles

- 2.2.5 Vehicle Class

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent emission and CO2 reduction regulations across Asia-Pacific

- 3.2.1.2 Rising fuel costs and demand for fuel-efficient vehicles

- 3.2.1.3 Government incentives supporting vehicle electrification

- 3.2.1.4 Rapid urbanization increasing adoption of start-stop systems

- 3.2.1.5 OEM electrification strategies and ADAS integration

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of 48V systems and components

- 3.2.2.2 Competition from full hybrids and battery electric vehicles

- 3.2.2.3 Limited consumer awareness of mild-hybrid benefits

- 3.2.2.4 Technical complexity of dual-voltage architectures

- 3.2.3 Market opportunities

- 3.2.3.1 Affordable mild-hybrid solutions for emerging markets

- 3.2.3.2 Growing adoption in commercial and fleet vehicles

- 3.2.3.3 Advancements in battery and power semiconductor technologies

- 3.2.3.4 Two-wheeler and three-wheeler 48V applications in Asia

- 3.2.3.5 Localization of manufacturing and strategic partnerships

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 China

- 3.4.1.1 MIIT dual-credit policy (CAFC + NEV Credits)

- 3.4.1.2 GB / GB-T vehicle electrical safety & EMC standards

- 3.4.2 Japan

- 3.4.2.1 Road transport vehicle act

- 3.4.2.2 MLIT fuel economy & emission standards

- 3.4.3 South Korea

- 3.4.3.1 K-MOE greenhouse gas & fuel efficiency regulations

- 3.4.3.2 MOLIT vehicle safety standards

- 3.4.4 India

- 3.4.4.1 Bharat stage VI (BS VI) emission norms

- 3.4.4.2 Automotive industry standards (AIS) under Motor Vehicles Act

- 3.4.5 Australia

- 3.4.5.1 Australian design rules (ADR)

- 3.4.5.2 National light vehicle emissions standards (ADR-linked CO2 targets)

- 3.4.1 China

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 48V system architecture evolution (P0 to P4)

- 3.7.1.2 Battery technology advancements

- 3.7.1.3 Power electronics innovation

- 3.7.2 Emerging technologies

- 3.7.2.1 Integrated starter-generator (ISG) development

- 3.7.2.2 DC-DC converter efficiency improvements

- 3.7.2.3 Thermal management solutions

- 3.7.1 Current technological trends

- 3.8 Pricing analysis

- 3.8.1 Component-level pricing trends

- 3.8.2 System-level cost structure

- 3.8.3 Price comparison between 12V and 48V systems

- 3.8.4 Regional price variations

- 3.8.5 Cost reduction roadmap (2024-2034)

- 3.8.6 Impact of economies of scale

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.11.1 Patent filing trends (2019-2025)

- 3.11.2 Key patent holders and technology leaders

- 3.11.3 Geographic distribution of patents

- 3.11.4 Technology domain analysis

- 3.11.5 Emerging patent clusters

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook and opportunities

- 3.14 Use cases & success stories

- 3.14.1 Passenger car use case

- 3.14.2 Commercial vehicle use cases

- 3.14.3 Best-case scenario analysis by architecture

- 3.14.4 Best-case ROI analysis by market segment

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Market concentration and competitive dynamics

- 4.7.1 Component-level market concentration

- 4.7.2 System integration competitive landscape

- 4.7.3 Emerging player threat analysis

- 4.7.4 Barriers to entry assessment

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 48V battery/energy storage

- 5.3 Starter-generator units

- 5.4 DC-DC converters

- 5.5 Inverters

- 5.6 Control units & power distribution

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By System Architecture, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 P0 (belt-driven)

- 6.3 P1 (crankshaft-mounted)

- 6.4 P2 (transmission input shaft)

- 6.5 P3 (dual-clutch/transmission-mounted)

- 6.6 P4 (rear axle/output shaft)

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchbacks

- 7.2.2 SUV

- 7.2.3 Sedan

- 7.3 Commercial vehicles

- 7.3.1 Vans

- 7.3.2 Utility & service vehicles

- 7.3.3 Pickup trucks

- 7.3.4 Light-duty buses

Chapter 8 Market Estimates & Forecast, By Vehicle Class, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Entry-level vehicles

- 8.3 Mid-premium vehicles

- 8.4 Luxury vehicles

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Regenerative braking & energy recuperation

- 9.3 Start-stop functionality

- 9.4 Electric boost/torque assist

- 9.5 Active chassis & stability control

- 9.6 Electric power steering (EPS)

- 9.7 HVAC & thermal management

- 9.8 Electric turbocharging

- 9.9 Fuel efficiency optimization

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 China

- 10.3 Japan

- 10.4 South Korea

- 10.5 India

- 10.6 Thailand

- 10.7 Australia

- 10.8 Malaysia

- 10.9 Vietnam

- 10.10 Indonesia

- 10.11 Singapore

- 10.12 New Zealand

- 10.13 Rest of Asia Pacific

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aptiv

- 11.1.2 BorgWarner

- 11.1.3 Continental

- 11.1.4 Denso

- 11.1.5 Magna International

- 11.1.6 Panasonic

- 11.1.7 Robert Bosch

- 11.1.8 Schaeffler

- 11.1.9 Valeo

- 11.1.10 ZF Friedrichshafen

- 11.2 Regional Players

- 11.2.1 Aisin

- 11.2.2 BYD

- 11.2.3 Contemporary Amperex Technology

- 11.2.4 Hitachi Astemo

- 11.2.5 Hyundai Mobis

- 11.2.6 Johnson Controls / Clarios

- 11.2.7 LG Electronics

- 11.2.8 Mando

- 11.2.9 Marelli

- 11.2.10 Mitsubishi Electric

- 11.3 Emerging Technology Innovators

- 11.3.1 AVL List

- 11.3.2 Eaton

- 11.3.3 Infineon Technologies

- 11.3.4 Mahle Powertrain

- 11.3.5 Tenneco