PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959282

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959282

Automotive eSIM Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

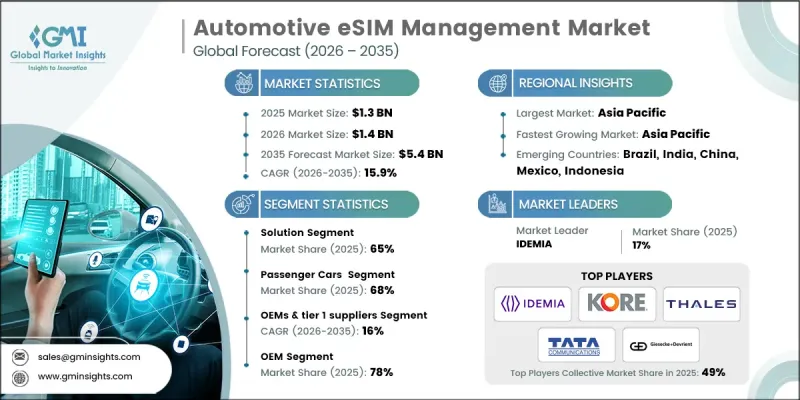

The Global Automotive eSIM Management Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 15.9% to reach USD 5.4 billion by 2035.

The market expansion is fueled by the increasing demand for secure, remotely managed cellular connectivity in vehicles. Unlike traditional removable SIM cards, eSIMs are embedded within telematics control units, allowing mobile network profiles to be updated, activated, or switched without physical intervention. Automotive eSIM management platforms have become essential for modern vehicle connectivity, supporting telematics, over-the-air updates, infotainment, emergency communications, and vehicle-to-everything (V2X) services for OEMs, fleet operators, and mobility service providers. The rapid growth of advanced driver assistance systems (ADAS) and autonomous driving technologies further drives demand, as uninterrupted high-bandwidth cellular connectivity is required for real-time sensor data, cloud-based decision-making, and HD map updates. Regulatory mandates, increasing consumer expectations for seamless in-car connectivity, and the digital transformation of the automotive ecosystem are key forces shaping market growth. Asia Pacific emerges as the largest and fastest-growing regional market due to high vehicle production in China, Japan, and South Korea, alongside expanding 5G networks and smart mobility initiatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 15.9% |

The solution segment held a 65% share in 2025 and is expected to grow at a CAGR of 16.6% through 2035. This segment includes eSIM management software platforms, secure hardware elements, and integrated provisioning systems. Solution adoption is high due to the significant costs associated with deploying enterprise-grade eSIM management platforms, with licensing fees for global OEMs ranging from USD 5 million to USD 15 million. These platforms provide subscription management, remote SIM provisioning servers, profile generation, and middleware integration with automotive backend systems. With gross margins of 75-85% post-development, solution providers benefit from strong vendor economics, driving recurring revenue and incentivizing ongoing platform enhancements.

The passenger car segment accounted for 68% share in 2025 and is expected to maintain a 16.2% CAGR through 2035. Passenger vehicles dominate the market in terms of unit volume and early adoption of connectivity features, including safety systems, infotainment, remote vehicle services, and emerging autonomous capabilities. Consumer expectations for smartphone-like experiences in cars, particularly in premium and luxury segments, are driving eSIM adoption. Stricter safety regulations in passenger vehicles, including emergency call mandates, also reinforce the need for reliable connectivity solutions.

China Automotive eSIM Management Market reached USD 183.1 million in 2025 and is projected to grow at a CAGR of 16.2% through 2035. The market growth in China is driven by widespread connected vehicle adoption, government-backed intelligent transportation initiatives, 5G network expansion, and rising consumer demand for digital vehicle services. With over 27 million vehicles produced annually, China's automotive market is rapidly integrating eSIM-enabled connected services, supported by domestic technology providers and electric vehicle innovators.

Key players operating in the Global Automotive eSIM Management Market include Aeris Communications, AT&T, Deutsche Telekom, Giesecke+Devrient (G+D), IDEMIA, Kigen (Arm Company), KORE Wireless, Tata Communications, Thales, and Verizon Communications. Companies in the Automotive eSIM Management Market are strengthening their presence by investing in comprehensive eSIM platforms that support remote provisioning, network switching, and lifecycle management across global OEMs. Strategic partnerships with vehicle manufacturers, telecom operators, and cloud providers enable seamless integration of connectivity services and ensure compliance with regional regulations. Vendors are expanding their service portfolios to include subscription management, middleware integration, and analytics for connected services. Investments in R&D focus on improving scalability, security, and interoperability of eSIM platforms, while regional expansions target high-growth markets in Asia Pacific and Europe.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Vehicle

- 2.2.4 Connectivity

- 2.2.5 Propulsion

- 2.2.6 Sales Channel

- 2.2.7 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in connected & autonomous vehicle deployments

- 3.2.1.2 5G network infrastructure expansion

- 3.2.1.3 Regulatory mandates for vehicle connectivity (eCall, C-V2X)

- 3.2.1.4 OEM demand for remote subscription management

- 3.2.1.5 Cost optimization in global fleet operations

- 3.2.1.6 Enhanced vehicle cybersecurity requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Legacy fleet management complexity

- 3.2.2.2 High initial implementation costs

- 3.2.2.3 Cybersecurity vulnerabilities & threat landscape

- 3.2.2.4 Inconsistent global regulatory frameworks

- 3.2.3 Market opportunities

- 3.2.3.1 Electric vehicle (EV) connectivity expansion

- 3.2.3.2 Fleet telematics digitalization

- 3.2.3.3 V2X communication ecosystem development

- 3.2.3.4 Aftermarket connectivity solutions growth

- 3.2.3.5 Emerging markets penetration (India, Southeast Asia)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal vehicle safety, emissions, and post-repair service regulations

- 3.4.1.2 Canada - Certified maintenance and EV servicing framework

- 3.4.2 Europe

- 3.4.2.1 Germany- EU vehicle safety regulations & national service standards

- 3.4.2.2 UK- Post-Brexit service compliance & connected vehicle guidance

- 3.4.2.3 France- National vehicle inspection & EV servicing policy

- 3.4.2.4 Italy- ITS pilots & smart-service regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT vehicle servicing mandates & standards

- 3.4.3.2 India- Emerging automotive service & connectivity regulations

- 3.4.3.3 Japan- ITS connect & certified service policies

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Remote SIM provisioning (RSP) technology

- 3.7.1.2 SM-DP+ architecture advancements

- 3.7.1.3 SM-SR security enhancements

- 3.7.2 Emerging technologies

- 3.7.2.1 Zero-touch provisioning (ZTP) innovations

- 3.7.2.2 In-factory profile provisioning (IFPP) emergence

- 3.7.2.3 Multi-mode connectivity solutions

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.9 Pricing analysis

- 3.9.1 Pricing models (per-device, subscription, hybrid)

- 3.9.2 Regional price variations

- 3.9.3 Price trend analysis

- 3.9.4 Cost structure breakdown

- 3.10 Use cases & success stories

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Security & privacy framework

- 3.12.1 Data encryption protocols

- 3.12.2 Secure OTA updates & remote provisioning

- 3.12.3 Compliance with global privacy regulations

- 3.12.4 Cyber threat mitigation strategies

- 3.13 Service & support infrastructure

- 3.13.1 Authorized service center readiness for eSIM and connected vehicles

- 3.13.2 Technician training & certification programs

- 3.13.3 Remote diagnostics & predictive maintenance support

- 3.13.4 Customer support & troubleshooting frameworks

- 3.14 OEM & Tier-1 Adoption Roadmap

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Connectivity management platforms (CMP)

- 5.2.2 Subscription manager data preparation

- 5.2.3 Subscription manager secure routing (SM-SR)

- 5.2.4 Integrated RSP platforms

- 5.2.5 Security & authentication solutions

- 5.2.6 Others

- 5.3 Services

- 5.3.1 Managed services

- 5.3.2 Professional services

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchbacks

- 6.2.2 SUV

- 6.2.3 Sedan

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCVs)

- 6.3.2 Medium commercial vehicles (MCVs)

- 6.3.3 Heavy commercial vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Connectivity, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 4G/LTE eSIM

- 7.3 5G eSIM

- 7.4 NB-IoT / LTE-M eSIM

- 7.5 Hybrid (4G + 5G) eSIM

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Battery electric vehicles (BEV)

- 8.3 Plug-in hybrid electric vehicles (PHEV)

- 8.4 Hybrid electric vehicles (HEV)

- 8.5 Internal combustion engine (ICE) vehicles

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 OEM embedded

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 OEMs & tier 1 suppliers

- 10.3 Fleet operators

- 10.4 Aftermarket service providers

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.3.9 Denmark

- 11.3.10 Poland

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Israel

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Aeris Communications

- 12.1.2 AT&T

- 12.1.3 Deutsche Telekom

- 12.1.4 Giesecke+Devrient (G+D)

- 12.1.5 IDEMIA

- 12.1.6 Kigen (Arm Company)

- 12.1.7 KORE Wireless

- 12.1.8 Tata Communications

- 12.1.9 Thales

- 12.1.10 Verizon Communications

- 12.2 Regional Players

- 12.2.1 Eseye

- 12.2.2 Infineon Technologies

- 12.2.3 NTT DOCOMO

- 12.2.4 NXP Semiconductors

- 12.2.5 Pelion

- 12.2.6 Qualcomm Technologies

- 12.2.7 Soracom

- 12.2.8 STMicroelectronics

- 12.2.9 Telefonica

- 12.2.10 Trasna Solutions

- 12.3 Emerging Players & Technology Enablers

- 12.3.1 1Global

- 12.3.2 Onomondo

- 12.3.3 Singapore Telecommunications (Singtel)

- 12.3.4 Valid

- 12.3.5 Wireless Logic