PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959283

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959283

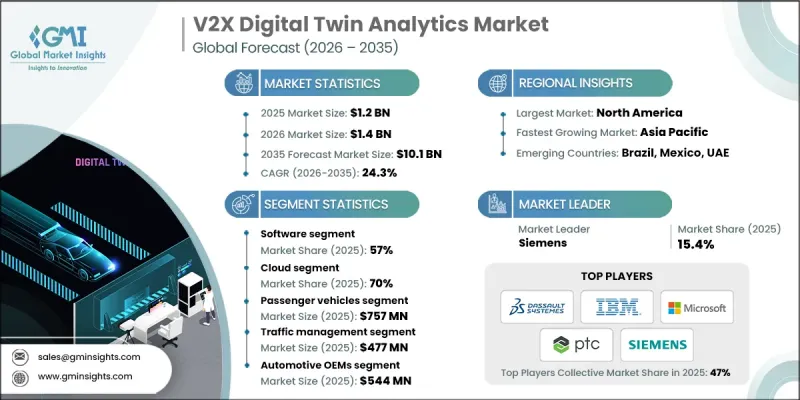

V2X Digital Twin Analytics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global V2X Digital Twin Analytics Market was valued at USD 1.2 billion in 2025 and is estimated to grow at a CAGR of 24.3% to reach USD 10.1 billion by 2035.

Growth is fueled by the accelerating shift toward connected mobility ecosystems and the rising integration of intelligent transportation systems. Stakeholders across mobility networks increasingly rely on data-driven platforms to enhance safety outcomes, improve traffic efficiency, and meet tightening regulatory expectations related to emissions and data governance. Digital twin analytics solutions are gaining traction as they enable real-time visibility, advanced simulation, and predictive decision-making across transportation networks. Continuous progress in analytics engines, communication technologies, and integrated data architectures is reshaping how mobility operations are planned and managed. Market participants are steadily moving toward flexible, cloud-enabled, and interoperable platforms that support real-time insights and proactive system optimization. As digital infrastructure matures globally, V2X digital twin analytics is becoming a critical enabler of intelligent, efficient, and resilient mobility frameworks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.2 Billion |

| Forecast Value | $10.1 Billion |

| CAGR | 24.3% |

The software segment held 57% share and is forecast to grow at a CAGR of 24.8% from 2026 to 2035. Software solutions form the foundation of digital twin analytics by delivering advanced modeling capabilities, continuous simulation, and intelligent data processing. These platforms support high levels of accuracy, scalability, and operational control, making them essential for managing complex mobility environments. Their ability to deliver real-time insights and predictive intelligence continues to drive widespread adoption across transportation ecosystems.

The cloud-based segment held 70% share in 2025 and is anticipated to grow at a CAGR of 24.6% through 2035. Cloud platforms are favored for their adaptability, centralized data access, and support for advanced analytics without heavy infrastructure investment. They enable seamless data integration, rapid scalability, and remote system management, which significantly enhances operational efficiency across geographically distributed mobility networks.

North America V2X Digital Twin Analytics Market held 83% share and generated USD 354.7 million in 2025. Strong digital infrastructure, advanced connectivity frameworks, and early adoption of intelligent mobility technologies have supported regional leadership. The U.S. continues to benefit from robust innovation ecosystems, large-scale mobility programs, and established regulatory frameworks that encourage advanced analytics deployment.

Key companies active in the Global V2X Digital Twin Analytics Market include Siemens, Microsoft, IBM, Dassault Systemes, ANSYS, Hexagon, PTC, OverBuilt, EZ Crusher, and Keestrack. Companies operating in the V2X Digital Twin Analytics Market focus on platform innovation, ecosystem partnerships, and scalable deployment models to strengthen their competitive position. Many invest heavily in advanced analytics capabilities, artificial intelligence integration, and real-time simulation performance to enhance solution value. Strategic alliances with mobility stakeholders help accelerate adoption and expand application scope. Firms also prioritize cloud-native architectures and interoperability to support seamless integration with existing systems. Continuous enhancement of cybersecurity, compliance readiness, and data governance strengthens customer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Application

- 2.2.5 Deployment Mode

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid growth of connected and autonomous vehicles

- 3.2.1.2 Smart city and intelligent transportation initiatives

- 3.2.1.3 Advanced AI/ML and edge-to-cloud analytics

- 3.2.1.4 Regulatory pressure on safety and emissions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation costs

- 3.2.2.2 Data privacy, security, and interoperability issues

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in Asia-pacific and emerging markets

- 3.2.3.2 Integration with autonomous vehicle and fleet management system

- 3.2.3.3 Regulatory compliance and safety solutions

- 3.2.3.4 Fleet and logistics optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: NHTSA & FCC Guidelines

- 3.4.1.2 Canada: Transport Canada & ISED Guidelines

- 3.4.2 Europe

- 3.4.2.1 Germany: Federal Ministry of Transport & Digital Infrastructure

- 3.4.2.2 France: Ministry for the Ecological Transition

- 3.4.2.3 UK: Department for Transport

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Ministry of Industry and Information Technology

- 3.4.3.2 Japan: Ministry of Land, Infrastructure, Transport and Tourism

- 3.4.3.3 South Korea: Ministry of Land, Infrastructure and Transport

- 3.4.3.4 India: Ministry of Road Transport & Highways

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Transport Agency

- 3.4.4.2 Mexico: Secretariat of Communications and Transportation (SCT)

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: Ministry of Industry and Advanced Technology

- 3.4.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

- 3.13 Data Architecture & Interoperability Frameworks

- 3.14 Cybersecurity, Data Governance & Functional Safety Implications

- 3.15 Deployment & Commercialization Models

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Digital twin platforms

- 5.2.2 Simulation & modeling engines

- 5.2.3 Analytics & AI software

- 5.3 Hardware

- 5.3.1 Edge computing devices

- 5.3.2 Sensors & RSUs

- 5.3.3 On-board vehicle computing units

- 5.4 Services

- 5.4.1 Integration & deployment

- 5.4.2 Managed analytics services

- 5.4.3 Consulting & customization

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Traffic Management

- 7.3 Predictive Maintenance

- 7.4 Fleet Management

- 7.5 Safety & Security

- 7.6 Autonomous Driving

Chapter 8 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 Cloud

- 8.3 On-Premises

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 Automotive OEMs

- 9.3 Government & transportation authorities

- 9.4 Fleet Operators

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 ANSYS

- 11.1.2 Dassault Systemes

- 11.1.3 EZ Crusher

- 11.1.4 Hexagon

- 11.1.5 IBM

- 11.1.6 Keestrack

- 11.1.7 Microsoft

- 11.1.8 OverBuilt

- 11.1.9 PTC

- 11.1.10 Siemens

- 11.2 Regional Player

- 11.2.1 Al-Jon Manufacturing

- 11.2.2 Eagle Crusher Company

- 11.2.3 Fayat

- 11.2.4 Hammel Recyclingtechnik

- 11.2.5 Liebherr

- 11.2.6 McCloskey International

- 11.2.7 Metso Outotec

- 11.2.8 Sandvik

- 11.2.9 Sierra International Machinery

- 11.2.10 Terex

- 11.3 Emerging Players

- 11.3.1 BHS-Sonthofen

- 11.3.2 Komplet America

- 11.3.3 Mobile Crushers International

- 11.3.4 Rockster Recycler

- 11.3.5 Rubble Master