PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959287

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959287

Halal Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

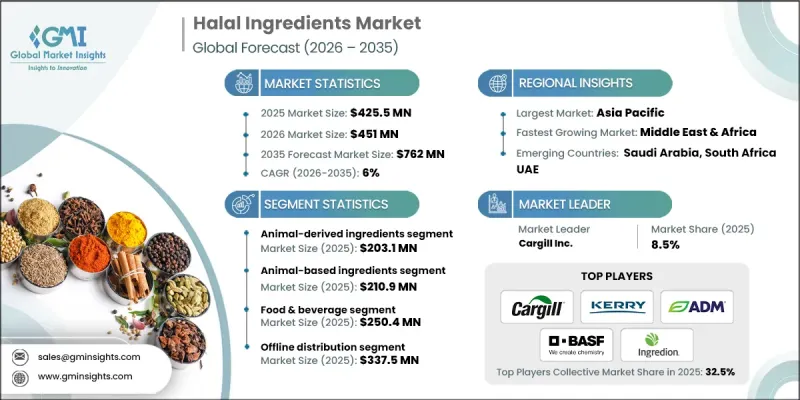

The Global Halal Ingredients Market was valued at USD 425.5 million in 2025 and is estimated to grow at a CAGR of 6% to reach USD 762 million by 2035.

The market is defined as the worldwide ecosystem responsible for the production and supply of ingredients used across food and beverages, pharmaceuticals, cosmetics, and related sectors that comply with halal requirements. Halal ingredients are positioned as being developed under strict ethical and religious frameworks, ensuring that sourcing, processing, and logistics adhere to recognized halal principles. This compliance framework is presented as a key factor in building consumer confidence. Market growth is attributed to expanding global demand for halal-certified offerings, supported by rising income levels, rapid urban development, and growing cross-border trade. Strong consumption trends are noted across Southeast Asia as well as the Middle East and North Africa, while demand is also accelerating in Europe and North America due to broader consumer trust in halal standards. The market is further supported by increased transparency enabled through harmonized certification systems and labeling practices, which reinforce product credibility among both traditional and non-traditional consumers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $425.5 Million |

| Forecast Value | $762 Million |

| CAGR | 6% |

The animal-based ingredients segment reached USD 203.1 million in 2025. This category includes materials that require strict oversight of sourcing practices, traceability, and quality assurance systems to align with international halal regulations. At the same time, demand for plant-origin ingredients continues to rise, driven by changing dietary preferences and the growing appeal of plant-forward nutrition. Ingredients produced through microbial and fermentation-based methods are also gaining attention, with manufacturers ensuring compliance through certified production environments and controlled processes.

The offline distribution segment generated USD 337.5 million in 2025. The market structure includes both physical and digital sales platforms; however, in-person purchasing remains dominant due to long-standing procurement habits among industrial buyers. Physical retail and business-to-business channels continue to play a central role, as buyers prioritize direct verification of certification, particularly when sourcing large volumes.

North America Halal Ingredients Market is expected to reach USD 80.1 million by 2035. Growth in this region is linked to increasing cultural diversity and greater public understanding of halal standards. Food retailers and service providers are expanding halal-certified portfolios, while consumers show heightened interest in ethically sourced and plant-focused formulations. Urban centers remain the primary demand hubs, supported by improved labeling practices and dedicated halal product placements in retail environments.

Key companies active in the Global Halal Ingredients Market include Cargill Inc., ADM, DSM-Firmenich, BASF SE, Ingredion, Kerry Group, Ajinomoto, Corbion, Roquette, and Givaudan. Companies operating in the halal ingredients market are strengthening their market positions through strategic investments in certification, supply chain transparency, and portfolio diversification. Many players are prioritizing compliance management by aligning production facilities with globally recognized halal standards. Product innovation focused on clean-label, plant-based, and ethically sourced ingredients is being used to attract a wider consumer base. Firms are also expanding their geographic reach through partnerships with regional distributors and food manufacturers. Branding efforts centered on trust, traceability, and quality assurance are helping companies reinforce credibility, while digital tools are increasingly used to improve documentation, audit readiness, and customer engagement across global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Source Origin

- 2.2.3 Application

- 2.2.4 Distribution Channel

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global demand for halal-compliant products

- 3.2.1.2 Increasing disposable incomes and urbanization in key markets

- 3.2.1.3 Growing health consciousness and preference for ethically sourced products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs associated with Halal certification and compliance

- 3.2.2.2 Complex supply chains that increase operational challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of blockchain and IoT for supply chain traceability

- 3.2.3.2 Automation in food processing and quality control for efficiency

- 3.2.3.3 Development of plant-based and lab-grown Halal-compliant alternatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By Product type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Animal-derived ingredients

- 5.2.1 Meat

- 5.2.2 Dairy

- 5.2.3 Gelatin

- 5.2.4 Collagen

- 5.2.5 Enzymes

- 5.3 Plant-derived ingredients

- 5.3.1 Proteins

- 5.3.2 Grains

- 5.3.3 Oils

- 5.3.4 Extracts

- 5.4 Microbial/fermentation-derived

- 5.4.1 Enzymes

- 5.4.2 Cultures

- 5.5 Precision fermentation proteins

- 5.5.1 Synthetic/chemical

- 5.5.2 Synthetic additives

- 5.5.3 Flavors

- 5.5.4 Colors

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Source Origin, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Animal-based ingredients

- 6.3 Plant-based ingredients

- 6.4 Microbial/fermentation-derived ingredients

- 6.5 Synthetic/chemically synthesized ingredients

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.2.1 Meat and poultry products

- 7.2.2 Dairy and dairy alternatives

- 7.2.3 Bakery and confectionery

- 7.2.4 Beverages

- 7.2.5 Snacks and savory foods

- 7.2.6 Processed and ready meals

- 7.2.7 Condiments and sauces

- 7.2.8 Others

- 7.3 Pharmaceuticals

- 7.3.1 Gelatin capsules

- 7.3.2 Excipients

- 7.3.3 Active pharmaceutical ingredients (APIs)

- 7.3.4 Vitamins and supplements

- 7.3.5 Others

- 7.4 Cosmetics & personal care

- 7.4.1 Skincare and body care

- 7.4.2 Haircare

- 7.4.3 Oral care

- 7.4.4 Fragrances and perfumes

- 7.4.5 Color cosmetics (makeup)

- 7.4.6 Others

- 7.5 Animal feed & pet food

- 7.5.1 Livestock feed (cattle, sheep, goat)

- 7.5.2 Poultry feed (chicken, turkey)

- 7.5.3 Aquaculture feed (fish, shrimp)

- 7.5.4 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Offline distribution

- 8.2.1 Hypermarkets and supermarkets

- 8.2.2 Convenience stores

- 8.2.3 Specialty halal stores

- 8.2.4 Traditional markets and bazaars

- 8.2.5 Foodservice

- 8.2.6 Others

- 8.3 Online distribution

- 8.3.1 E-commerce marketplaces

- 8.3.2 Direct-to-consumer (DTC) brand websites

- 8.3.3 Online grocery delivery

- 8.3.4 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 ADM

- 10.2 Ajinomoto

- 10.3 BASF SE

- 10.4 Cargill Inc.

- 10.5 Corbion

- 10.6 DSM-Firmenich

- 10.7 Givaudan

- 10.8 Ingredion

- 10.9 Kerry Group

- 10.10 Roquette