PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959290

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959290

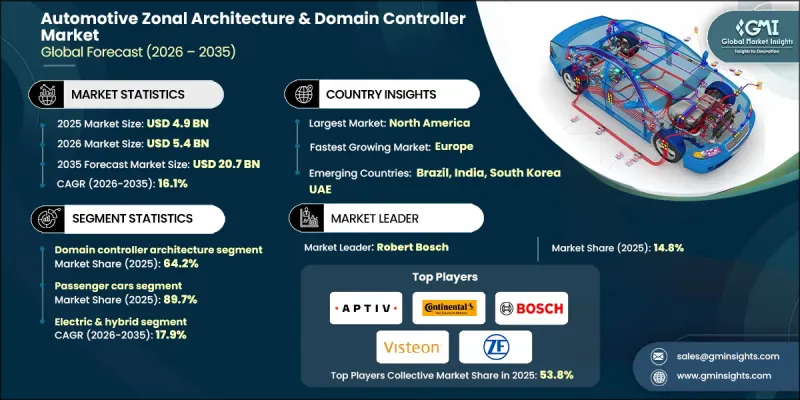

Automotive Zonal Architecture and Domain Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Automotive Zonal Architecture & Domain Controller Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 16.1% to reach USD 20.7 billion by 2035.

Market growth is driven by a fundamental shift in how vehicle electronics are designed and integrated. Automakers are moving away from highly fragmented electronic systems toward more centralized and software-focused architectures. Traditional vehicle designs relied on many independent electronic control units connected through extensive wiring networks, which increased vehicle weight, production complexity, and manufacturing costs. Zonal architecture restructures this approach by organizing electronics based on physical vehicle zones and connecting them through high-speed data networks, significantly reducing wiring requirements. This streamlined structure improves energy efficiency, simplifies assembly processes, and supports the transition toward software-defined vehicles where functionality can be updated digitally. Advanced communication protocols enable faster data handling from sensors and onboard systems, while improved power distribution helps optimize vehicle performance, particularly in electrified platforms. Together, these benefits are accelerating adoption across the global automotive industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $20.7 Billion |

| CAGR | 16.1% |

The domain controller architecture segment held 64.2% share, generating USD 3.2 billion in 2025. Automakers are favoring centralized computing systems because they consolidate multiple vehicle functions into fewer, high-performance units. By integrating areas such as driver assistance, infotainment, and body electronics into unified controllers, manufacturers reduce system complexity and wiring density. This approach also enhances scalability and makes it easier to deploy advanced software capabilities compared to legacy vehicle electronics designs.

The passenger cars segment accounted for 89.7% share in 2025 and is expected to reach USD 18.1 billion by 2035. Adoption is higher in this segment due to the growing concentration of advanced digital features and connected technologies. High production volumes and consumer demand for innovation make passenger vehicles the primary platform for introducing zonal and centralized electronic systems, enabling more efficient management of complex vehicle functions.

U.S. Automotive Zonal Architecture & Domain Controller Market reached USD 1.4 billion in 2025. The regional market is being shaped by strong momentum toward software-defined vehicle platforms, with manufacturers emphasizing centralized electronic architectures to support remote software updates and faster feature deployment. This shift is reinforcing demand for domain controller solutions across electric and next-generation vehicles.

Key companies operating in the Global Automotive Zonal Architecture & Domain Controller Market include Robert Bosch, Aptiv, Continental, ZF, Visteon, Valeo, NXP, Infineon, Qualcomm, and Onsemi. Companies in the automotive zonal architecture and domain controller market are strengthening their market position through heavy investment in advanced semiconductor development and centralized computing platforms. Strategic partnerships with automakers and software providers are helping accelerate the integration of scalable electronic architectures. Many players are expanding research efforts focused on high-speed networking, power management, and cybersecurity to support software-defined vehicles. Portfolio diversification, regional expansion, and early involvement in next-generation vehicle programs are also key priorities.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Architecture

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Autonomy level

- 2.2.6 Communication Protocol

- 2.2.7 Voltage

- 2.2.8 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising vehicle electrification

- 3.2.1.2 Increasing software-defined vehicle adoption

- 3.2.1.3 Growing demand for advanced driver assistance systems (ADAS)

- 3.2.1.4 Expansion of over-the-air (OTA) update capabilities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity and functional safety challenges

- 3.2.2.2 High development and integration complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of electric and hybrid vehicle platforms

- 3.2.3.2 Advancements in automotive ethernet technologies

- 3.2.3.3 Expansion of Software-Centric Automotive Ecosystems

- 3.2.3.4 Emerging opportunities in autonomous commercial vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Communications Commission

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.3 California Air Resources Board (CARB)

- 3.4.1.4 Transport Canada

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 UNECE World Forum for Harmonization of Vehicle Regulations

- 3.4.2.3 Vehicle Certification Agency

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Industry and Information Technology (MIIT), China

- 3.4.3.2 Japan Automobile Standards Internationalization Center

- 3.4.3.3 Automotive Industry Standards (AIS)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian Association of Automotive Vehicle Manufacturers (ANFAVEA)

- 3.4.4.2 INMETRO

- 3.4.4.3 National Road Safety Commission

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Standards Organization

- 3.4.5.2 South African Bureau of Standards

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Architecture & system design

- 3.11.1 Domain controller architecture fundamentals

- 3.11.2 Zonal architecture design principles

- 3.11.3 Hybrid architecture implementation strategies

- 3.11.4 Centralized vs decentralized computing models

- 3.11.5 High-performance computing (HPC) integration

- 3.12 Vehicle server architecture

- 3.12.1 Zonal gateway design and placement

- 3.12.2 Software Defined Vehicle (SDV) Strategy

- 3.12.3 Service-oriented architecture (SOA) implementation

- 3.12.4 Middleware platforms and standards

- 3.13 Zonal architecture in autonomous vehicles

- 3.13.1 ADAS domain integration in zonal systems

- 3.13.2 Sensor fusion architecture for autonomy

- 3.13.3 Real-time data processing requirements

- 3.13.4 Redundancy and fail-operational systems

- 3.13.5 Centralized perception and decision making

- 3.14 Case studies

- 3.15 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Architecture, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Domain controller architecture

- 5.3 Zonal architecture

- 5.4 Hybrid architecture

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Medium commercial vehicles

- 6.3.3 Heavy commercial vehicles

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Internal Combustion Engine (ICE) vehicles

- 7.3 Electric & hybrid vehicles

- 7.3.1 Battery Electric Vehicles (BEV)

- 7.3.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 7.3.3 Fuel Cell Electric Vehicles (FCEV)

Chapter 8 Market Estimates & Forecast, By Autonomy level, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Level 1

- 8.3 Level 2

- 8.4 Level 3

- 8.5 Level 4 & Level 5

Chapter 9 Market Estimates & Forecast, By Communication protocol, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 CAN / LIN-based system

- 9.3 Ethernet-based system

Chapter 10 Market Estimates & Forecast, By Voltage, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 12V system

- 10.3 48V system

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 ADAS domain

- 11.3 Powertrain / EV power domain

- 11.4 Body & comfort domain

- 11.5 Cockpit / infotainment domain

- 11.6 Safety domain

- 11.7 Chassis & motion domain

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Czech Republic

- 12.3.7 Belgium

- 12.3.8 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.4.10 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 Robert Bosch

- 13.1.2 Continental

- 13.1.3 Aptiv

- 13.1.4 NXP Semiconductors

- 13.1.5 Infineon

- 13.1.6 Valeo

- 13.1.7 STMicroelectronics

- 13.1.8 Texas Instruments

- 13.1.9 Visteon

- 13.1.10 Harman

- 13.1.11 Panasonic

- 13.1.12 NVIDIA

- 13.1.13 Qualcomm

- 13.1.14 onsemi

- 13.2 Regional players

- 13.2.1 HiRain

- 13.2.2 SemiDrive

- 13.2.3 Sonatus

- 13.2.4 ETAS

- 13.2.5 Elektrobit

- 13.2.6 Lear

- 13.2.7 Magna

- 13.2.8 Marelli

- 13.2.9 DENSO

- 13.3 Emerging players

- 13.3.1 TTTech

- 13.3.2 GuardKnox

- 13.3.3 Ambarella

- 13.3.4 Aurora Labs

- 13.3.5 Rivian

- 13.3.6 AUMOVIO

- 13.3.7 Molex