PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959297

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959297

Exhaust Aftertreatments System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

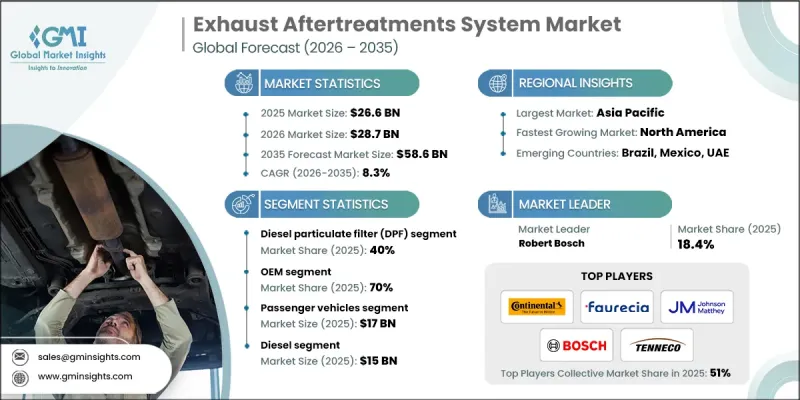

The Global Exhaust Aftertreatment System Market was valued at USD 26.6 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 58.6 billion by 2035.

Growth is driven by tightening emission requirements across major automotive regions, increasing global vehicle production, and a growing focus on minimizing harmful exhaust emissions, including nitrogen oxides, particulate matter, carbon monoxide, and unburned hydrocarbons. Automakers and fleet operators are under continuous pressure to deliver cleaner and more efficient vehicles while meeting compliance targets under real-world operating conditions. This has accelerated the integration of advanced exhaust aftertreatment solutions across both passenger and commercial vehicle segments. Manufacturers are increasingly prioritizing system durability, fuel efficiency improvement, and emission performance optimization. The market is also benefiting from ongoing innovation in catalyst formulations, system integration, sensor-based control, and digital diagnostics, which are redefining how exhaust emissions are monitored and managed. These developments are enabling higher system efficiency, faster regulatory compliance, and improved long-term performance, reinforcing the importance of exhaust aftertreatment technologies within the evolving global automotive ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $26.6 Billion |

| Forecast Value | $58.6 Billion |

| CAGR | 8.3% |

Demand for advanced exhaust aftertreatment systems continues to rise as manufacturers seek solutions capable of addressing diverse engine platforms and operating conditions. Technologies such as diesel particulate filters, selective catalytic reduction systems, diesel oxidation catalysts, gasoline particulate filters, and three-way catalysts are increasingly deployed as part of integrated emission control architectures. The growing use of diesel powertrains in commercial vehicles and gasoline direct injection engines in passenger cars is further supporting the adoption of high-performance aftertreatment systems. Continuous advancements in catalyst efficiency, modular system design, real-time emission sensing, and onboard diagnostics are enhancing system reliability and compliance while reducing lifecycle costs.

The diesel particulate filter segment held a 40% share in 2025 and is expected to grow at a CAGR of 8.1% between 2026 and 2035. This segment remains critical due to its effectiveness in capturing fine particulate emissions from diesel engines, making it a core requirement for emission compliance across multiple vehicle categories. Its proven performance and regulatory necessity continue to drive strong demand among manufacturers and suppliers.

The original equipment manufacturers segment accounted for 70% share in 2025 and is projected to grow at a CAGR of 8.6% through 2035. OEM dominance is supported by the integration of aftertreatment systems during vehicle production, ensuring optimized calibration, system durability, and consistent emission performance. OEM-installed systems offer better quality control, seamless compatibility with engine management systems, and long-term compliance assurance, making this channel the preferred route for advanced emission solutions.

China Exhaust Aftertreatment System Market held a 41% share in 2025 and reached USD 4.2 billion. Market leadership is supported by large-scale vehicle manufacturing, rapid adoption of advanced emission control technologies, and strong collaboration between automakers, component suppliers, and catalyst developers. Government support, high production volumes, and established supply chains continue to accelerate the deployment of modern aftertreatment systems across the country.

Key companies operating in the Global Exhaust Aftertreatment System Market include Robert Bosch, BorgWarner, Tenneco, Johnson Matthey, Continental, Cummins, Faurecia, Eberspacher, MANN+HUMMEL, and HJS Emission Technology. Companies in the exhaust aftertreatment system market are strengthening their market position through continuous investment in technology innovation and system integration. Manufacturers are focusing on developing compact, lightweight, and modular solutions that improve efficiency while reducing overall system costs. Strategic collaborations with automakers help align product development with evolving engine platforms and emission targets. Firms are also expanding global manufacturing footprints to improve supply reliability and reduce lead times. Enhanced digital monitoring, diagnostics, and sensor integration are being used to improve system performance and compliance over vehicle lifecycles. In addition, companies emphasize research into advanced catalyst materials and durability improvements to meet long-term regulatory and customer requirements, reinforcing competitiveness in a highly regulated market environment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Fuel type

- 2.2.5 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent Global Emission Regulations

- 3.2.1.2 Rising Production of Commercial Vehicles

- 3.2.1.3 Increasing Adoption of Gasoline Direct Injection (GDI) Engines

- 3.2.1.4 Advancements in Aftertreatment Technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High System Cost and Material Price Volatility

- 3.2.2.2 Growing Penetration of Battery Electric Vehicles (BEVs)

- 3.2.3 Market opportunities

- 3.2.3.1 Upcoming Euro 7 and Ultra-Low NOx Regulations

- 3.2.3.2 Expansion of Aftermarket and Retrofit Solutions

- 3.2.3.3 Technological Innovation in Catalysts and Sensors

- 3.2.3.4 Industrial Partnerships and OEM Collaborations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, CARB, NHTSA Emission Standards

- 3.4.1.2 Canada: Transport Canada, CMVSS 305

- 3.4.2 Europe

- 3.4.2.1 Germany: BMDV, Euro 6/7 Regulations

- 3.4.2.2 France: Ministry of Transport, Euro 6/7

- 3.4.2.3 UK: Department for Transport, Euro 6/7

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport, Emission Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: MIIT, China 6/7 Standards

- 3.4.3.2 Japan: MLIT, JIS Emission Regulations

- 3.4.3.3 South Korea: MOLIT, KS Emission Standards

- 3.4.3.4 India: MoRTH, BS6 Norms

- 3.4.4 Latin America

- 3.4.4.1 Brazil: DENATRAN, CONAMA Standards

- 3.4.4.2 Mexico: Ministry of Communications & Transport, NOM Emission Regulations

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA Emission Regulations

- 3.4.5.2 Saudi Arabia: Ministry of Transport, SASO Emission Standards

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Diesel Particulate Filter (DPF)

- 5.3 Selective Catalytic Reduction (SCR)

- 5.4 Diesel Oxidation Catalyst (DOC)

- 5.5 Three-Way Catalyst (TWC)

- 5.6 Exhaust Gas Recirculation (EGR)

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Conventional

- 7.3 Heated

- 7.4 Acoustic

- 7.5 Heads-Up Display (HUD) Enabled

Chapter 8 Market Estimates & Forecast, By Fuel Type, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 Diesel

- 8.3 Gasoline

- 8.4 Alternative Fuels

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 BorgWarner

- 11.1.2 Continental AG

- 11.1.3 Cummins

- 11.1.4 Eberspacher Group

- 11.1.5 Faurecia SE

- 11.1.6 HJS Emission Technology GmbH

- 11.1.7 Johnson Matthey

- 11.1.8 MANN+HUMMEL GmbH

- 11.1.9 Robert Bosch GmbH

- 11.1.10 Tenneco

- 11.2 Regional Player

- 11.2.1 Akebono Brake Industry

- 11.2.2 Calsonic Kansei

- 11.2.3 Denso Corporation

- 11.2.4 Dongfeng Motor Component

- 11.2.5 Johnson Controls

- 11.2.6 Mahle GmbH

- 11.2.7 NGK Insulators

- 11.2.8 Tofas Engine Systems

- 11.2.9 Umicore

- 11.2.10 Valeo

- 11.3 Emerging Players

- 11.3.1 Anhui Ankai Automotive Components

- 11.3.2 Clean Emission Technologies

- 11.3.3 EcoMotors

- 11.3.4 GreenTech Catalysts

- 11.3.5 ZF Aftermarket Solutions