PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959300

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959300

Bulk Solid-State Laser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

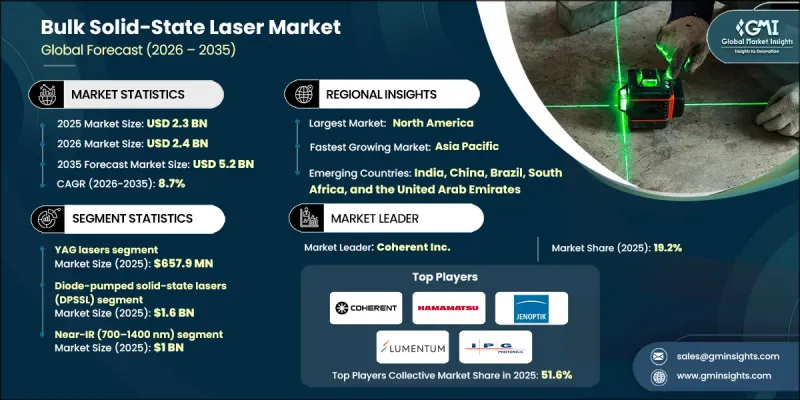

The Global Bulk Solid-State Laser Market was valued at USD 2.3 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 5.2 billion by 2035.

Market momentum is fueled by rising demand for high-power laser systems in industrial material processing, expanding semiconductor and microelectronics production, growing utilization in medical and aesthetic treatments, increasing deployment in aerospace and defense systems, and technological progress in crystal growth and pump sources. The expansion of advanced electronics manufacturing and precision component fabrication continues to drive the need for reliable, high-accuracy laser platforms. Public sector funding initiatives and regional investment programs designed to strengthen domestic manufacturing capabilities are reinforcing supply chain resilience and accelerating technology development. Bulk solid-state laser systems utilize solid crystalline or glass gain media, energized by optical pumping methods to generate coherent, high-energy beams. Their superior beam quality, operational stability, precision, and ability to deliver high power output position them as critical tools across industrial processing, semiconductor fabrication, healthcare applications, scientific research, and defense operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.3 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 8.7% |

The Nd: YAG laser segment reached USD 657.9 million in 2025. These systems are recognized for delivering strong output power combined with excellent beam quality, making them highly effective in demanding industrial material processing operations across automotive, aerospace, and electronics manufacturing environments. In medical and aesthetic applications, their precision and controlled energy delivery support procedures requiring minimal collateral impact and consistent clinical performance. Manufacturers are prioritizing the development of high-power Nd: YAG platforms designed for both industrial and medical applications, emphasizing durability, scalable configurations, and comprehensive after-sales support to secure long-term customer relationships and recurring revenue streams.

The diode-pumped solid-state laser segment accounted for USD 1.6 billion in 2025. Strong energy efficiency and enhanced beam performance are key factors driving adoption across industrial, semiconductor, aerospace, and medical sectors. Compared with traditional pumping approaches, diode-pumped systems offer extended operational lifespan and reduced thermal stress, enabling continuous high-throughput manufacturing and mission-critical defense operations. Their ability to maintain stable performance while lowering operating costs makes them well-suited for large-scale production environments. Manufacturers are focusing on high-efficiency diode architectures, modular power scalability, and advanced thermal management technologies to meet stringent industrial, medical, and defense performance requirements while prioritizing energy optimization.

North America Bulk Solid-State Laser Market held 34.6% share in 2025. The region maintains a leading position due to strong industrial automation capabilities, advanced healthcare infrastructure, and significant defense investments. The United States represents the primary revenue contributor, driven by precision manufacturing, aerospace engineering, and medical laser applications, alongside sustained research and development activity in automotive and electronics sectors. Established industrial ecosystems and diversified end-use industries support steady adoption of next-generation solid-state laser technologies. Vendors operating in the region are investing in ruggedized, high-precision systems tailored for industrial and defense applications while strengthening collaboration with research institutions to influence technology standards and accelerate commercialization among early adopters.

Major companies active in the Bulk Solid-State Laser Market include IPG Photonics, Coherent Inc., Lumentum Operations LLC, Hamamatsu Photonics K.K., Jenoptik Laser GmbH, Northrop Grumman Corporation, LUMIBIRD, Quanta System SP, ALPHALAS GmbH, CrystaLaser, LLC, LASEROPTEK Co., Ltd., Laserglow Technologies, Daheng New Epoch Technology, Inc., Edgewave, and Jiangsu Lumispot Technology Co., Ltd. Companies operating in the Bulk Solid-State Laser Market are strengthening their competitive standing through continuous innovation, strategic partnerships, and vertical integration. Many players are investing heavily in research and development to improve beam quality, power scalability, and energy efficiency. Expanding production capabilities and enhancing crystal growth technologies help secure supply chain stability and cost control. Strategic collaborations with industrial OEMs, semiconductor manufacturers, medical device companies, and defense contractors support long-term contracts and customized system development.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Laser type trends

- 2.2.2 Pumping method trends

- 2.2.3 Wavelength trends

- 2.2.4 Power output trends

- 2.2.5 Operation type trends

- 2.2.6 Application trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High-power industrial material processing demand

- 3.2.1.2 Growth in semiconductor and microelectronics manufacturing

- 3.2.1.3 Rising adoption in medical and aesthetic applications

- 3.2.1.4 Expansion of defense and aerospace laser systems

- 3.2.1.5 Advancements in crystal growth and pump technologies

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High system cost and complex manufacturing

- 3.2.2.2 Thermal management and efficiency limitations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Laser Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Nd:YAG Lasers

- 5.3 Ytterbium-Doped Bulk Lasers (Yb:YAG, Yb:YLF, Other Yb-hosts)

- 5.4 Erbium-Doped Bulk Lasers (Er:YAG)

- 5.5 Holmium & Thulium-Doped Bulk Lasers (Ho:YAG, Tm:YAG)

- 5.6 Ti:Sapphire Lasers

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Pumping Method, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Lamp-Pumped Solid-State Lasers

- 6.3 Diode-Pumped Solid-State Lasers (DPSSL)

Chapter 7 Market Estimates and Forecast, By Wavelength, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 UV (<400 nm)

- 7.3 Visible (400-700 nm)

- 7.4 Near-IR (700-1400 nm)

- 7.5 Mid-IR (1400-3000 nm)

- 7.6 Far-IR (>3000 nm)

Chapter 8 Market Estimates and Forecast, By Power Output, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Low Power (<50 W)

- 8.3 Medium Power (50-500 W)

- 8.4 High Power (>500 W)

Chapter 9 Market Estimates and Forecast, By Operation Type, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Pulsed Operation

- 9.3 Nanosecond Pulsed

- 9.4 Ultrashort Pulsed

- 9.5 Continuous Wave Operation

- 9.6 Quasi Continuous Wave Operation

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 10.1 Key Trends

- 10.2 Industrial Manufacturing

- 10.3 Medical & Healthcare

- 10.4 Defense & Security

- 10.5 Research & Scientific

- 10.6 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Coherent Inc.

- 12.1.2 IPG Photonics

- 12.1.3 Northrop Grumman Corporation

- 12.1.4 Lumentum Operations LLC

- 12.1.5 Jenoptik Laser GmbH

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 CrystaLaser, LLC

- 12.2.1.2 Edgewave

- 12.2.1.3 Laserglow Technologies

- 12.2.2 Europe

- 12.2.2.1 ALPHALAS GmbH

- 12.2.2.2 LUMIBIRD

- 12.2.2.3 Quanta System SP

- 12.2.3 Asia Pacific

- 12.2.3.1 Hamamatsu Photonics K.K.

- 12.2.3.2 Daheng New Epoch Technology, Inc.

- 12.2.3.3 Jiangsu Lumispot Technology Co., Ltd.

- 12.2.1 North America

- 12.3 Niche / Disruptors

- 12.3.1 LASEROPTEK Co., Ltd.

- 12.3.2 CryLaS Crystal Laser Systems GmbH

- 12.3.3 Bright Solutions Srl

- 12.3.4 Light Conversion

- 12.3.5 TOPTICA Photonics