PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959309

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959309

Europe Adult Disposable Incontinence Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

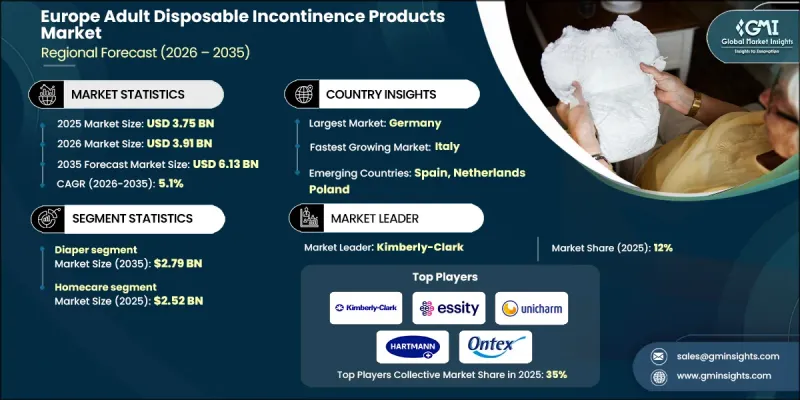

Europe Adult Disposable Incontinence Products Market was valued at USD 3.75 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 6.13 billion by 2035.

The steady growth trajectory is attributed to Europe's rapidly aging population, where individuals aged 65 and above account for over one-fifth of the total population. The increasing incidence of age-related conditions, mobility limitations, and chronic diseases such as diabetes, obesity, and neurological disorders has significantly increased long-term demand for disposable incontinence solutions. Additionally, improving reimbursement coverage in countries such as Germany, France, and the Nordic region is making these products more accessible across both home care and institutional environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.75 Billion |

| Forecast Value | $6.13 Billion |

| CAGR | 5.1% |

Growing social acceptance and declining stigma associated with adult incontinence have further strengthened product adoption across Europe. Consumers are increasingly prioritizing products that offer discretion, comfort, and skin protection, encouraging manufacturers to invest in innovations such as breathable back sheets, dermatologically tested materials, and advanced odor-control technologies. The strong expansion of e-commerce platforms and online pharmacies has also played a critical role in market development, offering privacy-driven purchasing, subscription-based deliveries, and wider product availability, particularly for elderly users and caregivers in remote locations.

By product type, the diapers segment represented USD 2.79 billion in 2025, supported by their extensive use across hospitals, nursing homes, assisted living facilities, and residential care settings. Diapers are preferred due to their superior absorbency, ease of use, and suitability for individuals with moderate to severe incontinence. Continuous improvements in thin-core technology, superabsorbent polymers, and ergonomic design have further enhanced user comfort and leakage protection.

In 2025, the offline channel accounted for the highest share of the market. Physical retail outlets benefit from strong brand visibility and well-established relationships between healthcare professionals and consumers, which significantly influence purchasing behavior. In-store promotions and product demonstrations allow buyers to better understand product functionality and benefits, helping build confidence and drive sales. Despite the rapid growth of digital retail, offline channels continue to lead due to the assurance, accessibility, and personalized assistance associated with brick-and-mortar stores. Trust remains a decisive factor in healthcare-related purchases, particularly among senior consumers, who prioritize reliability, ease of access, and face-to-face support over online convenience.

Germany Adult Disposable Incontinence Products Market reached USD 0.7 billion in 2025, supported by strong healthcare infrastructure, comprehensive reimbursement policies, and high awareness of incontinence management solutions. The country's well-established elderly care ecosystem, combined with high per-capita healthcare spending, continues to support robust product demand. United Kingdom, France, and Italy are expected to witness accelerated growth due to rising elderly populations, expanding home-care services, and increasing healthcare investments.

The competitive landscape of the Europe Adult Disposable Incontinence Products Market is characterized by the presence of established global players and strong regional manufacturers. Key players operating in the market include Essity AB, Kimberly-Clark Corporation, Procter & Gamble Company, Ontex Group, Abena A/S, Paul Hartmann AG, ConvaTec Group, and Domtar Corporation. These companies maintain their market positions through broad product portfolios, strong brand recognition, and extensive distribution networks across pharmacies, hospitals, supermarkets, and online platforms. Companies operating in the Europe Adult Disposable Incontinence Products Market are focusing on innovation, sustainability, and geographic expansion to strengthen their market foothold. Leading players are investing heavily in research and development to introduce high-absorbency, skin-friendly, and eco-friendly products that comply with Europe's stringent environmental regulations. Strategic partnerships with healthcare providers, nursing homes, and retail chains are helping manufacturers improve product accessibility and institutional penetration. Mergers and acquisitions are widely used to expand regional presence, particularly in Eastern Europe.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Product type

- 2.2.3 End use

- 2.2.4 Size

- 2.2.5 Absorbency level

- 2.2.6 Age group

- 2.2.7 Price range

- 2.2.8 Consumer group

- 2.2.9 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapidly aging population

- 3.2.1.2 Increasing healthcare expenditure & assistive technology uptake

- 3.2.1.3 Greater social acceptance & awareness

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Reimbursement variability across Europe

- 3.2.2.2 Persistent social stigma & underreporting

- 3.2.3 Opportunities

- 3.2.3.1 Integration of smart and sustainable materials

- 3.2.3.2 Expansion into home healthcare & E-commerce channels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By country

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By country

- 4.2.1.1 Germany

- 4.2.1.2 UK

- 4.2.1.3 France

- 4.2.1.4 Italy

- 4.2.1.5 Spain

- 4.2.1.6 Netherlands

- 4.2.1.7 Switzerland

- 4.2.1.8 Poland

- 4.2.1.9 Sweden

- 4.2.1.10 Russia

- 4.2.1 By country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Diaper

- 5.3 Pull-up underwear

- 5.4 Liners & guards

- 5.5 Under pads

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Home care

- 6.3 Nursing homes

- 6.4 Hospitals & ambulatory surgery centres

Chapter 7 Market Estimates and Forecast, By Size, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Small

- 7.3 Medium

- 7.4 Large

- 7.5 Extra large

Chapter 8 Market Estimates and Forecast, By Absorbency Level, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Light

- 8.3 Moderate

- 8.4 Heavy

- 8.5 Overnight

Chapter 9 Market Estimates and Forecast, By Age Group, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Early adulthood (20-39)

- 9.3 Middle adulthood (40-59)

- 9.4 Young old age (60-75)

- 9.5 Old age (75+)

Chapter 10 Market Estimates and Forecast, By Price Range, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Low (<25$)

- 10.3 Mid (25$-50$)

- 10.4 High (>50$)

Chapter 11 Market Estimates and Forecast, By Consumer Group, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Male

- 11.3 Female

Chapter 12 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 Offline

- 12.2.1 Specialty stores

- 12.2.2 Pharmaceutical stores

- 12.2.3 Others

- 12.3 Online

- 12.3.1 E-commerce websites

- 12.3.2 Company owned website

Chapter 13 Market Estimates and Forecast, By Country, 2022 - 2035 (USD Billion) (Thousand Units)

- 13.1 Key trends

- 13.2 Germany

- 13.3 UK

- 13.4 France

- 13.5 Italy

- 13.6 Spain

- 13.7 Netherlands

- 13.8 Switzerland

- 13.9 Poland

- 13.10 Sweden

- 13.11 Russia

Chapter 14 Company Profiles

- 14.1 ABENA

- 14.2 Advanced Absorbent Technologies

- 14.3 Attends / Attindas

- 14.4 Cardinal Health

- 14.5 Caroli

- 14.6 Drylock Technologies

- 14.7 Essity AB

- 14.8 First Quality Enterprises

- 14.9 Indas

- 14.10 Kimberly-Clark

- 14.11 KNH

- 14.12 Medline

- 14.13 Ontex BV

- 14.14 Paul Hartmann AG

- 14.15 Unicharm