PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959311

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959311

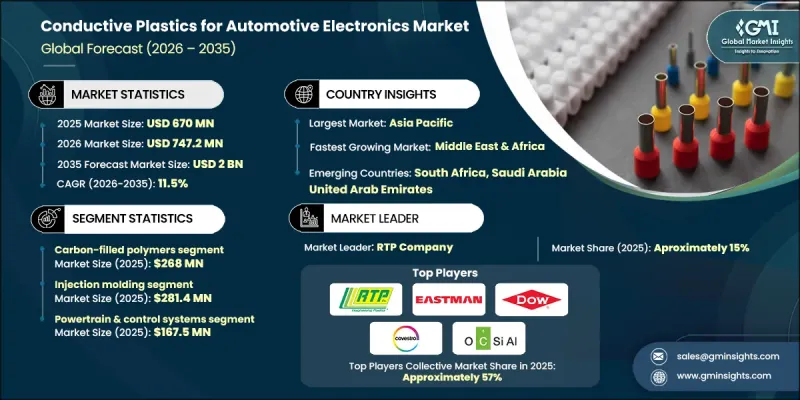

Conductive Plastics for Automotive Electronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Conductive Plastics for Automotive Electronics Market was valued at USD 670 million in 2025 and is estimated to grow at a CAGR of 11.5% to reach USD 2 billion by 2035.

Growth is driven by the automotive industry's increasing reliance on lightweight, high-performance materials to improve energy efficiency, reduce vehicle mass, and enable greater design flexibility. Conductive plastics are increasingly replacing conventional metals in electronic housings, connectors, and structural components, offering comparable performance with significantly lower weight. This transition aligns with OEM priorities around thermal efficiency, compact packaging, and seamless integration of complex electronic architectures. As vehicle platforms become more modular and electrified, demand for multifunctional materials that combine conductivity, durability, and manufacturability continues to rise. The rapid increase in onboard electronics, including advanced driver assistance, connectivity solutions, infotainment systems, and power electronics, has heightened the need for effective electromagnetic and radio-frequency interference shielding. Conductive plastics play a critical role in protecting sensitive components while enabling compact system designs, making them essential to modern automotive electronics development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $670 Million |

| Forecast Value | $2 Billion |

| CAGR | 11.5% |

The carbon-filled polymers segment reached USD 268 million in 2025. These materials are widely adopted due to their balanced electrical conductivity, cost efficiency, and low density, making them suitable for EMI and ESD shielding applications. Other conductive plastic types address different performance requirements, with higher conductivity materials supporting demanding electrical and thermal conditions, while flexible conductive polymers are gaining relevance in specialized applications that require corrosion resistance and tunable performance characteristics.

The powertrain and control systems segment accounted for USD 167.5 million in 2025 and is expected to grow at a CAGR of 12.1% during 2026-2035. Conductive plastics are increasingly used in sensors, control units, and electronic modules within these systems, where consistent electrical performance under thermal and mechanical stress is essential. Their adoption is also expanding across safety-related electronics and driver assistance systems, where stable signal transmission and effective shielding are critical for reliable operation.

North America Conductive Plastics for Automotive Electronics Market generated USD 120.9 million in 2025 and is expected to experience sustained growth over the forecast period. The region benefits from advanced automotive electronics adoption, mature manufacturing infrastructure, and strong investment in electric vehicle production. The United States represents the largest share of regional demand due to its well-established supply chain and focus on lightweight, high-performance materials that enhance electrical safety and shielding performance.

Key companies active in the Global Conductive Plastics for Automotive Electronics Market include Covestro AG, RTP Company, DOW, Eastman Chemical Company, Nanocyl SA, OCSiAl, Heraeus Materials Technology, SIMONA AG, and Agfa Gevaert NV. Companies in the conductive plastics for automotive electronics market are strengthening their market position through continuous material innovation and close collaboration with automotive OEMs. Manufacturers are investing in advanced polymer formulations that deliver improved conductivity, thermal stability, and weight reduction. Strategic partnerships with electronics and vehicle platform developers help align materials with next-generation design requirements. Firms are also expanding production capabilities and regional footprints to support growing EV and electronics demand. Emphasis on scalable manufacturing, cost optimization, and compliance with automotive standards enables wider adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Conductive Plastic Type

- 2.2.3 Manufacturing Process

- 2.2.4 End Use Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of lightweight materials in automotive electronics

- 3.2.1.2 Increasing demand for EMI/RFI shielding components

- 3.2.1.3 Technological advancements in conductive additives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited thermal conductivity

- 3.2.2.2 Complex and costly processing

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of EV & smart electronics applications

- 3.2.3.2 Advancements in high-performance conductive fillers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Conductive Plastic Type, 2022 - 2035 (USD million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Carbon-filled polymers

- 5.2.1 Carbon black

- 5.2.2 Carbon nanotubes (CNT)

- 5.2.3 Graphene/graphite

- 5.3 Metal-filled polymers

- 5.3.1 Silver-filled

- 5.3.2 Nickel-filled

- 5.3.3 Copper-filled

- 5.3.4 Hybrid metal fillers

- 5.4 Intrinsic conductive polymers

- 5.4.1 Polyaniline (PANI)

- 5.4.2 Polypyrrole (PPy)

- 5.4.3 Poly(3,4-ethylenedioxythiophene) (PEDOT)

- 5.5 Conductive polymer composites

- 5.5.1 Thermoplastic composites

- 5.5.2 Thermoset composites

Chapter 6 Market Estimates and Forecast, By Manufacturing Process, 2022 - 2035 (USD million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Injection molding

- 6.3 Extrusion (Profile, Film, Sheet, Cable)

- 6.4 Coating & surface treatment

- 6.5 Additive manufacturing (3D Printing)

- 6.6 Compounding & masterbatch production

Chapter 7 Market Estimates and Forecast, By End Use Application, 2022 - 2035 (USD million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Powertrain & control systems

- 7.2.1 Engine control modules (ECM)

- 7.2.2 Battery management systems (BMS) for EVs

- 7.3 Safety & ADAS

- 7.3.1 Airbag sensors

- 7.3.2 Lidar/radar housings

- 7.3.3 Camera mounts & shielding

- 7.4 Infotainment & telematics

- 7.4.1 Touch displays & bezels

- 7.4.2 Antenna covers

- 7.4.3 EMI/RFI Shields

- 7.5 Body electronics

- 7.5.1 Smart key housings

- 7.5.2 Sensor housings (Proximity, Rain, Light)

- 7.5.3 Connectivity modules

- 7.6 Charging & power distribution

- 7.6.1 Ev charging components

- 7.6.2 Power distribution units

- 7.6.3 Connector housings

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 RTP Company

- 9.2 Eastman Chemical Company

- 9.3 SIMONA AG

- 9.4 Nanocyl SA

- 9.5 OCSiAl

- 9.6 DOW

- 9.7 Covestro AG

- 9.8 Heraeus Materials Technology

- 9.9 Agfa-Gevaert NV