PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959317

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959317

Automatic Vehicle Location Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

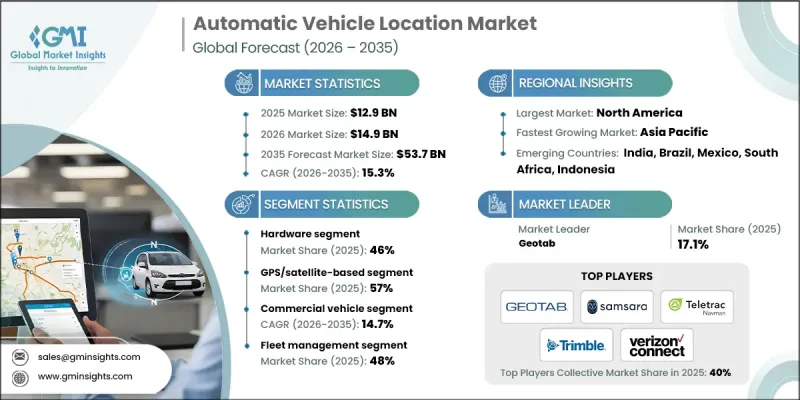

The Global Automatic Vehicle Location Market was valued at USD 12.9 billion in 2025 and is estimated to grow at a CAGR of 15.3% to reach USD 53.7 billion by 2035.

Demand for real-time visibility into vehicle movements continues to rise as organizations seek stronger control over logistics performance and operational costs. Companies across transportation, delivery, and service-based fleets are increasingly deploying AVL solutions to optimize routing, improve scheduling accuracy, and reduce fuel consumption. Continuous tracking capabilities allow operators to limit idle time, enhance driver accountability, and respond more efficiently to operational disruptions. As competition intensifies and delivery timelines tighten, AVL platforms are becoming essential tools for improving productivity and service reliability. The ability to generate actionable insights from location data is also helping organizations improve decision-making and align fleet performance with broader efficiency and sustainability goals. This shift toward data-driven fleet management is reinforcing the role of AVL systems as a core component of modern transportation infrastructure worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.9 Billion |

| Forecast Value | $53.7 Billion |

| CAGR | 15.3% |

Regulatory pressure from both public authorities and private-sector standards bodies continues to strengthen market adoption. Fleet operators are increasingly required to meet stricter requirements related to safety oversight, cargo visibility, and emissions tracking. Monitoring and reporting systems are now essential for compliance across public transportation fleets, commercial operators, and specialized vehicle segments. AVL platforms support adherence to these mandates by improving transparency, strengthening internal controls, and enabling accurate documentation. As regulations evolve, fleet operators rely on AVL systems to minimize compliance risks, avoid penalties, and maintain consistent safety standards across operations.

The commercial vehicles segment held 75% share and is expected to grow at a CAGR of 14.7% from 2026 to 2035. Operators of commercial fleets continue to lead adoption as they focus on route optimization, fuel efficiency, and regulatory alignment. Integration of AVL systems with telematics platforms, connected sensors, and predictive analytics supports proactive maintenance planning and real-time safety monitoring. Advanced diagnostics and intelligent analytics capabilities are increasingly embedded within fleet technology ecosystems, reinforcing long-term demand from logistics and utility operators.

U.S. Automatic Vehicle Location Market reached USD 3.86 billion in 2025. Strong adoption across the country is supported by the widespread use of advanced analytics to improve vehicle uptime and route efficiency. High penetration of connected vehicle technologies continues to accelerate deployment, while the rapid expansion of e-commerce delivery networks is increasing demand for precise, real-time tracking solutions that improve last-mile visibility and operational responsiveness.

Key companies operating in the Global Automatic Vehicle Location Market include Verizon Connect, Geotab, Samsara, Trimble, TomTom, Orbcomm, Teletrac Navman, MiX Telematics, Fleet Complete, and CalAmp. Companies in the automatic vehicle location market adopt focused strategies to strengthen their competitive position and expand market share. Continuous investment in software innovation enables providers to enhance analytics, reporting accuracy, and system scalability. Many players integrate artificial intelligence and machine learning to support predictive maintenance, driver behavior analysis, and route optimization. Strategic partnerships with vehicle manufacturers, logistics firms, and technology providers help accelerate deployment and broaden customer reach. Subscription-based service models improve recurring revenue stability. Companies also prioritize cybersecurity and data privacy to build customer trust.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 Vehicle

- 2.2.6 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for real-time fleet tracking & operational efficiency

- 3.2.1.2 Government regulations & compliance mandates

- 3.2.1.3 Technological advancements (IoT, Cloud, 5G & Analytics)

- 3.2.1.4 Growth of smart city & public transport initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial costs and integration complexity

- 3.2.2.2 Data privacy & security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with emerging technologies (AI, big data, machine learning)

- 3.2.3.2 Expansion into electric & connected vehicle management

- 3.2.3.3 Emerging markets & new sector adoption

- 3.2.3.4 Smart cities & intelligent mobility services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Department of Transportation (DOT) Standards

- 3.4.1.2 Occupational Safety and Health Administration (OSHA) Guidelines

- 3.4.1.3 U.S. Environmental Protection Agency (EPA)

- 3.4.2 Europe

- 3.4.2.1 EN ISO Tire Standards

- 3.4.2.2 European Union Customs and Safety Regulations

- 3.4.2.3 BS EN / CEN Standards

- 3.4.2.4 National Standards (UNE, DIN, etc.)

- 3.4.3 Asia Pacific

- 3.4.3.1 China GB (Guobiao) Standards

- 3.4.3.2 Japan JIS Requirements

- 3.4.3.3 Korea KS Certification

- 3.4.3.4 Indian BIS Standards

- 3.4.3.5 Thai Industrial Standards Institute (TISI)

- 3.4.4 Latin America

- 3.4.4.1 INMETRO (National Institute of Metrology)

- 3.4.4.2 INTI certification (Instituto Nacional de Tecnologia Industrial)

- 3.4.4.3 NOM standards (Norma Official Mexicana)

- 3.4.5 Middle East & Africa

- 3.4.5.1 ESMA / Emirates Conformity Assessment Scheme (ECAS)

- 3.4.5.2 GCC technical regulations

- 3.4.5.3 SABS certification

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 Pricing by product

- 3.8.2 Pricing by region

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Integration with connected vehicle ecosystem

- 3.13 Customization & modular solutions

- 3.14 Integration with autonomous vehicle management

- 3.15 Cybersecurity & data protection standards

- 3.16 AI and predictive analytics adoption

- 3.17 5G and edge computing integration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 OBD devices/Trackers

- 5.2.2 Standalone trackers

- 5.2.3 Sensors & electronic control units

- 5.3 Software

- 5.3.1 Fleet management & analytics

- 5.3.2 Performance management

- 5.3.3 Driver behavior monitoring

- 5.3.4 Vehicle diagnostics

- 5.3.5 Others (reporting, integration platforms)

- 5.4 Services

- 5.4.1 Installation & integration services

- 5.4.2 Maintenance & support services

- 5.4.3 Consulting & advisory services

- 5.4.4 Managed services & subscription plans

- 5.4.5 Training services

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 GPS/Satellite-based

- 6.3 GPRS/Cellular network

- 6.4 Dual mode

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV (Light commercial vehicle)

- 7.3.2 MCV (Medium commercial vehicle)

- 7.3.3 HCV (Heavy commercial vehicle)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Fleet management

- 8.3 Asset tracking

- 8.4 Vehicle tracking

- 8.5 Stolen vehicle recovery (SVR)

- 8.6 Public transit management

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Transportation & logistics

- 9.3 Construction & manufacturing

- 9.4 Government & defense

- 9.5 Aviation

- 9.6 Retail & e-commerce

- 9.7 Agriculture

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 CalAmp

- 11.1.2 Continental

- 11.1.3 Geotab

- 11.1.4 Motive (formerly KeepTruckin)

- 11.1.5 Motorola Solutions

- 11.1.6 Samsara

- 11.1.7 Teletrac Navman

- 11.1.8 Teltonika

- 11.1.9 Trimble

- 11.1.10 Verizon Connect

- 11.2 Regional players

- 11.2.1 Cartrack

- 11.2.2 Digital Matter

- 11.2.3 Fleetio

- 11.2.4 Masternaut

- 11.2.5 Meitrack

- 11.2.6 Michelin Connected Fleet

- 11.2.7 Micodus

- 11.2.8 MiX Telematics

- 11.2.9 Ruptela

- 11.2.10 Suntech

- 11.3 Emerging players

- 11.3.1 Bouncie

- 11.3.2 ClearPathGPS

- 11.3.3 iStartek

- 11.3.4 Linxup

- 11.3.5 Rhino Fleet Tracking

- 11.3.6 TKStar

- 11.3.7 TopFlyTech