PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959319

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959319

Cloud Compliance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

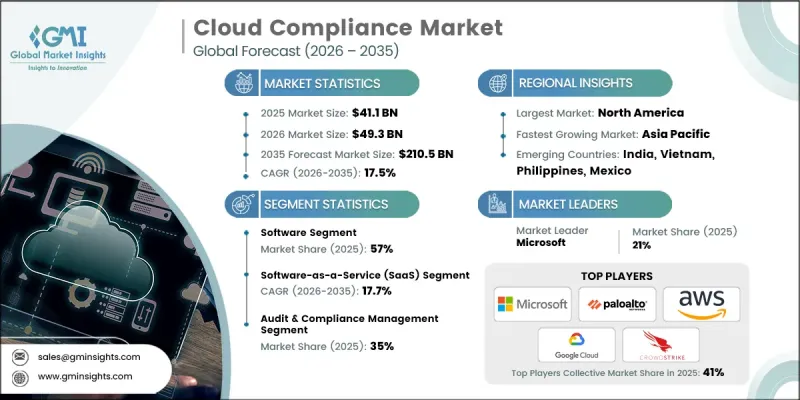

The Global Cloud Compliance Market was valued at USD 41.1 billion in 2025 and is estimated to grow at a CAGR of 17.5% to reach USD 210.5 billion by 2035.

Accelerated enterprise migration toward public, private, and hybrid cloud environments is significantly increasing compliance complexity across workloads, identities, configurations, and data assets. As organizations distribute applications across multiple cloud infrastructures, maintaining consistent governance and policy enforcement has become more challenging. The growing reliance on diverse cloud service providers alongside private infrastructure often results in fragmented visibility, creating a strong demand for centralized compliance orchestration and automated oversight platforms. Enterprises are prioritizing continuous monitoring frameworks to satisfy both internal governance standards and evolving regulatory requirements at scale. Industries such as financial services and telecommunications are increasingly deploying unified security and compliance architectures that consolidate posture management and application protection capabilities. Additionally, expanding data protection regulations and sector-specific mandates are intensifying compliance exposure, compelling businesses to invest in automated evidence collection and reporting systems. Real-time compliance tracking is gradually replacing traditional periodic audits, driving widespread adoption of SaaS-based compliance solutions that offer agility, scalability, and proactive risk mitigation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $41.1 Billion |

| Forecast Value | $210.5 Billion |

| CAGR | 17.5% |

The software segment accounted for 57% share in 2025 and is anticipated to grow at a CAGR of 16.6% from 2026 to 2035. Compliance platforms are evolving from standalone posture management tools into integrated ecosystems that unify identity governance, workload protection, configuration management, and data security controls. This transition is encouraging tool consolidation within enterprises seeking improved cross-cloud visibility and operational efficiency. Software providers are embedding compliance validation directly into development pipelines and infrastructure automation workflows to detect violations earlier in the deployment lifecycle. By incorporating compliance checks within DevOps and platform engineering processes, organizations can reduce remediation expenses, accelerate cloud rollouts, and strengthen accountability across technical teams. These advancements are reinforcing the dominance of software-driven compliance frameworks in complex multi-cloud environments.

The Software-as-a-Service segment held a 52% share in 2025 and is forecast to grow at a CAGR of 17.7% between 2026 and 2035. SaaS-based compliance solutions deliver continuous monitoring of data access controls, user behavior, and configuration integrity across externally hosted applications. As enterprises rapidly deploy cloud-native platforms, maintaining visibility and governance across third-party systems becomes increasingly critical. SaaS compliance tools provide centralized dashboards, automated reporting capabilities, and audit-ready documentation that help organizations safeguard sensitive data, enforce identity management standards, and maintain regulatory readiness. The flexibility and scalability of SaaS delivery models continue to drive adoption across enterprises of all sizes.

United States Cloud Compliance Market reached USD 14.1 billion in 2025. Across the country, enterprises are consolidating multiple security and compliance solutions into unified cloud-native protection platforms to streamline regulatory adherence and reduce operational complexity. This consolidation reduces redundant tooling, enhances audit preparedness, and enables continuous oversight of hybrid and multi-cloud workloads. Adoption of artificial intelligence-driven risk prioritization is expanding, allowing organizations to identify high-impact compliance gaps and automate coordinated remediation workflows across departments. AI-powered analytics are improving operational efficiency by minimizing false alerts and fostering closer collaboration between IT operations and security teams. These developments are positioning the United States as a leading hub for advanced cloud compliance innovation.

Major companies operating in the Global Cloud Compliance Market include Palo Alto Networks, Microsoft, Google Cloud, Amazon Web Services (AWS), Check Point Software, CrowdStrike, Fortinet, Trend Micro, Qualys, and Wiz. These providers compete by delivering integrated compliance, security, and risk management platforms designed to address evolving regulatory landscapes and multi-cloud operational demands. Companies in the Global Cloud Compliance Market are reinforcing their competitive standing through platform consolidation, AI-driven automation, and expanded multi-cloud interoperability. Vendors are investing in advanced analytics and machine learning models to deliver predictive compliance insights and automated remediation capabilities. Strategic partnerships with cloud providers and enterprise clients enable deeper integration across hybrid infrastructures. Many firms are enhancing developer-focused tools that embed compliance validation within CI/CD pipelines to promote proactive governance. In addition, providers are expanding global data center footprints and compliance certifications to meet regional regulatory standards.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment model

- 2.2.4 Application

- 2.2.5 Enterprise size

- 2.2.6 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Accelerated cloud migration

- 3.2.1.2 Multi-cloud and hybrid complexity

- 3.2.1.3 Rising data privacy and security obligations

- 3.2.1.4 Shift to continuous compliance automation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and integration costs

- 3.2.2.2 Shortage of skilled cloud compliance professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Compliance automation for SMBs

- 3.2.3.2 Managed cloud compliance services

- 3.2.3.3 Integration with DevSecOps and CI/CD pipelines

- 3.2.3.4 Public sector and government cloud adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Institute of Standards and Technology (NIST)

- 3.4.1.2 Federal Risk and Authorization Management Program (FedRAMP)

- 3.4.2 Europe

- 3.4.2.1 European Data Protection Board (EDPB)

- 3.4.2.2 ENISA (European Union Agency for Cybersecurity)

- 3.4.3 Asia Pacific

- 3.4.3.1 Singapore Personal Data Protection Commission (PDPC)

- 3.4.3.2 Japan Information-technology Promotion Agency (IPA)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Data Protection Authority (ANPD)

- 3.4.4.2 Mexico National Institute for Transparency, Access to Information and Personal Data Protection (INAI)

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Data Office / Ministry of Artificial Intelligence & Federal Authority for Identity and Citizenship

- 3.4.5.2 South Africa Information Regulator (SAIR)

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Investment & funding analysis

- 3.13 Risk & cybersecurity exposure analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

Chapter 6 Market Estimates & Forecast, By Deployment model, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Software-as-a-Service (SaaS)

- 6.3 Infrastructure-as-a-Service (IaaS)

- 6.4 Platform-as-a-Service (PaaS)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Audit & compliance management

- 7.3 Threat detection & remediation

- 7.4 Activity monitoring & analytics

- 7.5 Visibility & risk assessment

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Enterprise size, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Large enterprises

- 8.3 Small & medium enterprises (SMEs)

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 IT & telecommunications

- 9.4 Healthcare

- 9.5 Government & public sector

- 9.6 Retail & consumer goods

- 9.7 Manufacturing

- 9.8 Energy & utilities

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.4.8 Philippines

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 Amazon Web Services (AWS)

- 11.1.2 Check Point Software Technologies

- 11.1.3 CrowdStrike

- 11.1.4 Fortinet

- 11.1.5 Google Cloud (Alphabet Inc.)

- 11.1.6 IBM

- 11.1.7 Microsoft

- 11.1.8 Palo Alto Networks

- 11.1.9 Qualys

- 11.1.10 Trend Micro

- 11.2 Regional players

- 11.2.1 Aqua Security

- 11.2.2 Lacework (Fortinet)

- 11.2.3 Orca Security

- 11.2.4 Rapid7

- 11.2.5 SentinelOne

- 11.2.6 Snyk

- 11.2.7 Sysdig

- 11.2.8 Tenable

- 11.2.9 Wiz

- 11.2.10 Zscaler

- 11.3 Emerging players

- 11.3.1 Horangi Cyber Security

- 11.3.2 Scrut Automation

- 11.3.3 Secureframe

- 11.3.4 Vanta